Absolute Strengh Histogram

Stockcharts and Investopedia have literature on this indicator.

With the formula being:

StochRSI = (RSI - min(RSI, period)) / (max(RSI, period) - min(RSI, period))

In theory the period to calculate the RSI is the same that will later be

applied to find out the minimum and maximum values of the RSI. That means

that if the chosen period is 14 (de-facto standard) for the RSI, the total

look-back period for the indicator will be 28

Note

The actual look-back period will be a bit longer, because a 14-period

RSI has a longer effective look-back period of 15, as the comparison

of the closing prices of the 1st two periods is needed to kick-start the

calculations

In any case, backtrader does calculate all the needed look-back and warm-up periods automatically.

Considering that the following are built-in indicators in backtrader:

RSILowest(akaMaxN)Highest(akaMinN)

developing the StochRSI according to the formula seen above is

straightforward.

class StochRSI(bt.Indicator):

lines = ('stochrsi',)

params = dict(

period=14, # to apply to RSI

pperiod=None, # if passed apply to HighestN/LowestN, else "period"

)

def __init__(self):

rsi = bt.ind.RSI(self.data, period=self.p.period)

pperiod = self.p.pperiod or self.p.period

maxrsi = bt.ind.Highest(rsi, period=pperiod)

minrsi = bt.ind.Lowest(rsi, period=pperiod)

self.l.stochrsi = (rsi - minrsi) / (maxrsi - minrsi)

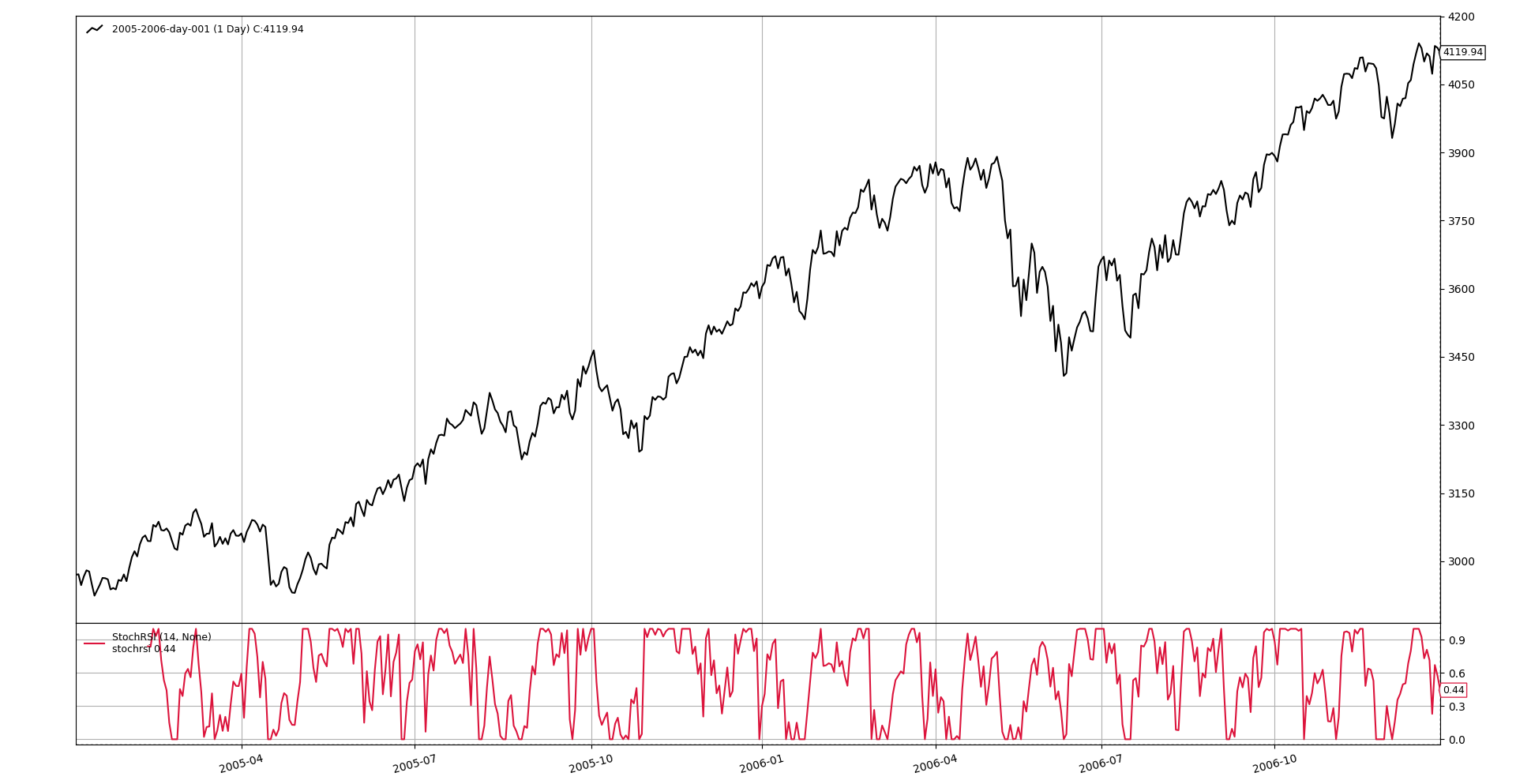

And here a view of how the indicator works