Synchronizing different markets

The more the usage the more the mix of ideas and unexpected scenarios that backtrader has to face. And with each new one, a challenge to see if the platform can live up to the expectations set forth when development started, flexibility and ease of use were the targets and Python was chosen as the cornerstone.

Ticket #76 raises the

question as to whether synchronizing markets with different trading calendars can

be done. Direct attempts to do so fail and the issue creator wonders why

backtrader is not looking at the date.

Before any answer is delivered some thought has to be put into:

- Behavior of indicators for the days which do not align

The answer to the latter is:

- The platform is as much as possible

dateandtimeagnostic and will not look at the contents of the fields to evaluate those concepts

Taken into account the fact that stock market prices are datetime series

the above can hold up true up to certain limits. In the case of multiple datas

the following design considerations apply:

-

The 1st data added to

cerebrois thedatamaster -

All other datas have to be time aligned/synchronized with it never being able to overtake (in

datetimeterms) thedatamaster

Putting together the 3 bullet points from above delivers the mix experienced by the issue creator. The scenario:

-

Calendar Year:

2012 -

Data 0:

^GSPC(or S&P 500 for friends) -

Data 1:

^GDAXI(or Dax Index for friends)

Running a custom script to see how the data is synchronized by backtrader:

$ ./weekdaysaligner.py --online --data1 '^GSPC' --data0 '^GDAXI'

And the output:

0001, True, data0, 2012-01-03T23:59:59, 2012-01-03T23:59:59, data1

0002, True, data0, 2012-01-04T23:59:59, 2012-01-04T23:59:59, data1

0003, True, data0, 2012-01-05T23:59:59, 2012-01-05T23:59:59, data1

0004, True, data0, 2012-01-06T23:59:59, 2012-01-06T23:59:59, data1

0005, True, data0, 2012-01-09T23:59:59, 2012-01-09T23:59:59, data1

0006, True, data0, 2012-01-10T23:59:59, 2012-01-10T23:59:59, data1

0007, True, data0, 2012-01-11T23:59:59, 2012-01-11T23:59:59, data1

0008, True, data0, 2012-01-12T23:59:59, 2012-01-12T23:59:59, data1

0009, True, data0, 2012-01-13T23:59:59, 2012-01-13T23:59:59, data1

0010, False, data0, 2012-01-17T23:59:59, 2012-01-16T23:59:59, data1

0011, False, data0, 2012-01-18T23:59:59, 2012-01-17T23:59:59, data1

...

As soon as 2012-01-16 the trading calendars diverge. The data0 is the

datamaster (^GSPC) and even if data1 (^GDAXI) would have a bar

to deliver on 2012-01-16, this wasn’t a trading day for the S&P 500.

The best that backtrader can do with the aforementioned design restrictions

when the next trading day for the ^GSPC comes in, the 2012-01-17 is

deliver the next not yet processed date for ^GDAXI which is the

2012-01-16.

And the synchronization problem accumulates with each diverging day. At the end

of 2012 it looks like follows:

...

0249, False, data0, 2012-12-28T23:59:59, 2012-12-19T23:59:59, data1

0250, False, data0, 2012-12-31T23:59:59, 2012-12-20T23:59:59, data1

The reason should be obvious: the Europeans trade more days than the Americans.

In the Ticket #76 https://github.com/mementum/backtrader/issues/76 the

poster shows what zipline does. Let’s look at the 2012-01-13 -

2012-01-17 conundrum:

0009 : True : 2012-01-13 : close 1289.09 - 2012-01-13 : close 6143.08

0010 : False : 2012-01-13 : close 1289.09 - 2012-01-16 : close 6220.01

0011 : True : 2012-01-17 : close 1293.67 - 2012-01-17 : close 6332.93

Blistering barnacles! The data for 2012-01-13 has been simply

duplicated without apparently asking the user for permission. Imho, this

shouldn’t be because the end user of the platform cannot undo this spontaneous

addition.

Note

Except for a brief look at zipline, the author doesn’t know if

this is the standard behavior, configured by the script developer and

if it can be undone

Once we have seen that the others let’s try again with backtrader using

the accumulated wisdom: the Europeans trade more often than the

Americans. Let’s reverse the roles of ^GSPC and ^GDAXI and see the

outcome:

$ ./weekdaysaligner.py --online --data1 '^GSPC' --data0 '^GDAXI'

The output (skipping to 2012-01-13 directly):

...

0009, True, data0, 2012-01-13T23:59:59, 2012-01-13T23:59:59, data1

0010, False, data0, 2012-01-16T23:59:59, 2012-01-13T23:59:59, data1

0011, True, data0, 2012-01-17T23:59:59, 2012-01-17T23:59:59, data1

...

Blistering barnacles again! backtrader has also duplicated the

2012-01-13 value for data1 (in this case ^GSPC) as a match for

data0 (now ^GDAXI) delivery of 2012-01-16.

And even better:

- Synchronization is reachieved with the next date:

2012-01-17

The same re-synchronization is seen again soon:

...

0034, True, data0, 2012-02-17T23:59:59, 2012-02-17T23:59:59, data1

0035, False, data0, 2012-02-20T23:59:59, 2012-02-17T23:59:59, data1

0036, True, data0, 2012-02-21T23:59:59, 2012-02-21T23:59:59, data1

...

Followed by not such an easy re-sync:

...

0068, True, data0, 2012-04-05T23:59:59, 2012-04-05T23:59:59, data1

0069, False, data0, 2012-04-10T23:59:59, 2012-04-09T23:59:59, data1

...

0129, False, data0, 2012-07-04T23:59:59, 2012-07-03T23:59:59, data1

0130, True, data0, 2012-07-05T23:59:59, 2012-07-05T23:59:59, data1

...

Such episodes keep repeating until the last bar for ^GDAXI is delivered:

...

0256, True, data0, 2012-12-31T23:59:59, 2012-12-31T23:59:59, data1

...

The reason for this synchronization issues is that backtrader does NOT

duplicate the data.

-

Once the

datamasterhas delivered a new bar the otherdatasare asked to deliver -

If no bar can be delivered for the current

datetimeof thedatamaster(because it, for example, would be overtaken) the next best data is, so to say, re-deliveredAnd this is a bar with an already seen

date

Proper Synchronization

But not all hope is lost. backtrader can deliver. Let’s use

filters. This piece of technology in backtrader allows manipulating the

data before it hits the deepest parts of the platform and for example

indicators are calculated.

Note

delivering is a perception matter and therefore what

backtrader delivers may not be what the recipient is expecting as

the delivery

The actual code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import datetime

class WeekDaysFiller(object):

'''Bar Filler to add missing calendar days to trading days'''

# kickstart value for date comparisons

lastdt = datetime.datetime.max.toordinal()

def __init__(self, data, fillclose=False):

self.fillclose = fillclose

self.voidbar = [float('Nan')] * data.size() # init a void bar

def __call__(self, data):

'''Empty bars (NaN) or with last close price are added for weekdays with no

data

Params:

- data: the data source to filter/process

Returns:

- True (always): bars are removed (even if put back on the stack)

'''

dt = data.datetime.dt() # current date in int format

lastdt = self.lastdt + 1 # move the last seen data once forward

while lastdt < dt: # loop over gap bars

if datetime.date.fromordinal(lastdt).isoweekday() < 6: # Mon-Fri

# Fill in date and add new bar to the stack

if self.fillclose:

self.voidbar = [self.lastclose] * data.size()

self.voidbar[-1] = float(lastdt) + data.sessionend

data._add2stack(self.voidbar[:])

lastdt += 1 # move lastdt forward

self.lastdt = dt # keep a record of the last seen date

self.lastclose = data.close[0]

data._save2stack(erase=True) # dt bar to the stack and out of stream

return True # bars are on the stack (new and original)

The test script is already fitted with the capability to use it:

$ ./weekdaysaligner.py --online --data0 '^GSPC' --data1 '^GDAXI' --filler

With --filler the WeekDaysFiller is added to both data0 and

data1. And the output:

0001, True, data0, 2012-01-03T23:59:59, 2012-01-03T23:59:59, data1

...

0009, True, data0, 2012-01-13T23:59:59, 2012-01-13T23:59:59, data1

0010, True, data0, 2012-01-16T23:59:59, 2012-01-16T23:59:59, data1

0011, True, data0, 2012-01-17T23:59:59, 2012-01-17T23:59:59, data1

...

The 1st conundrum at 2012-01-13 - 2012-01-17 is gone. And the entire

set is synchronized:

...

0256, True, data0, 2012-12-25T23:59:59, 2012-12-25T23:59:59, data1

0257, True, data0, 2012-12-26T23:59:59, 2012-12-26T23:59:59, data1

0258, True, data0, 2012-12-27T23:59:59, 2012-12-27T23:59:59, data1

0259, True, data0, 2012-12-28T23:59:59, 2012-12-28T23:59:59, data1

0260, True, data0, 2012-12-31T23:59:59, 2012-12-31T23:59:59, data1

Something worth noticing:

-

With

^GSPCasdata0we had250lines (the index traded250days in2012) -

With

^GDAXIwedata0had256lines (the index traded256days in2012) -

And with the

WeekDaysFillerin place the length of both datas has been extended to260Adding

52*2(weekends and days in a weekend), we would end up with364. The remaining day until the regular365days in a year was for sure a Saturday or a Sunday.

The filter is filling with NaN values for the days in which no trading

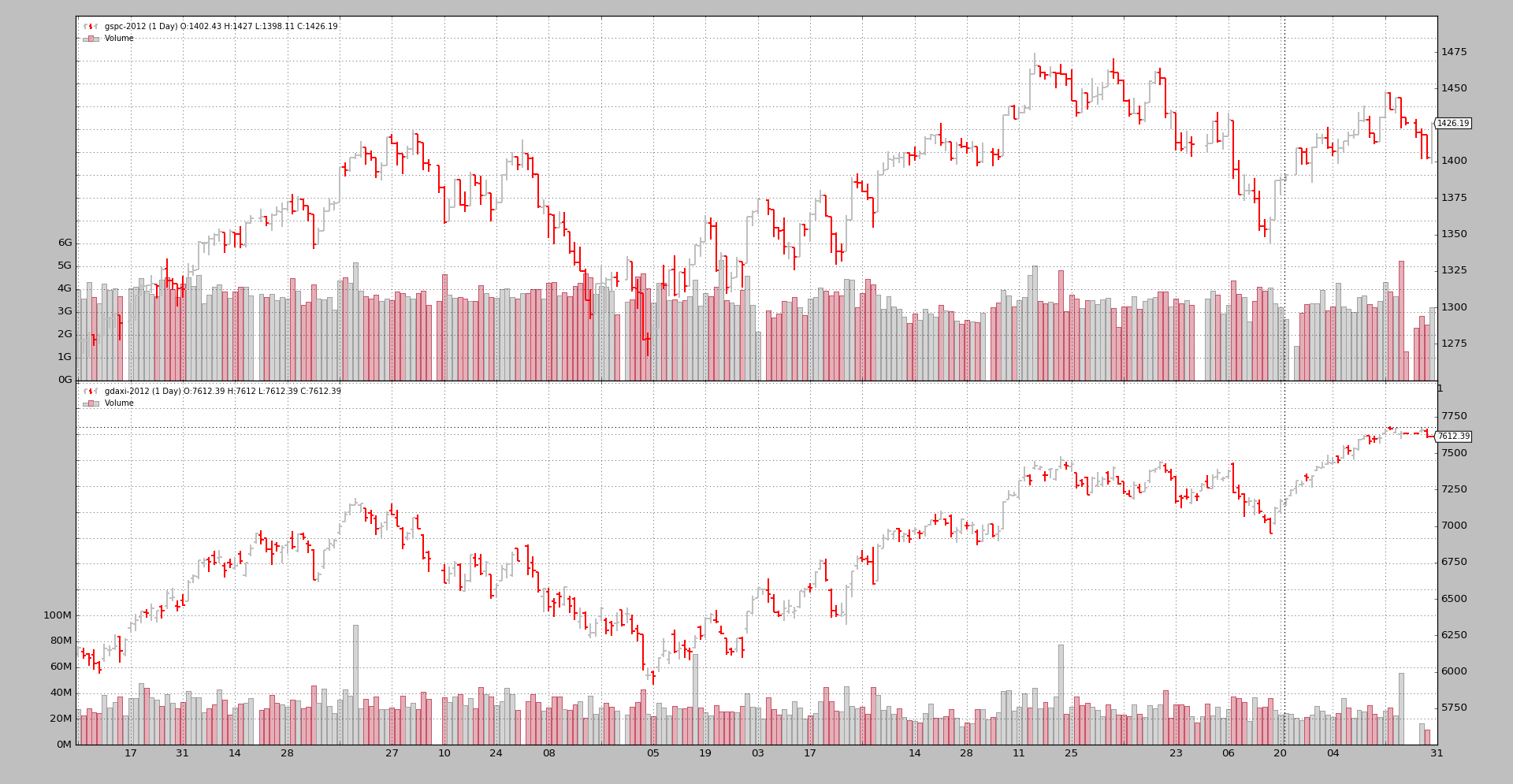

took place for the given data. Let’s plot it:

$ ./weekdaysaligner.py --online --data0 '^GSPC' --data1 '^GDAXI' --filler --plot

Filled days are quite obvious:

-

The gap in between bars is there

-

The gap is even more obvious for the volume plot

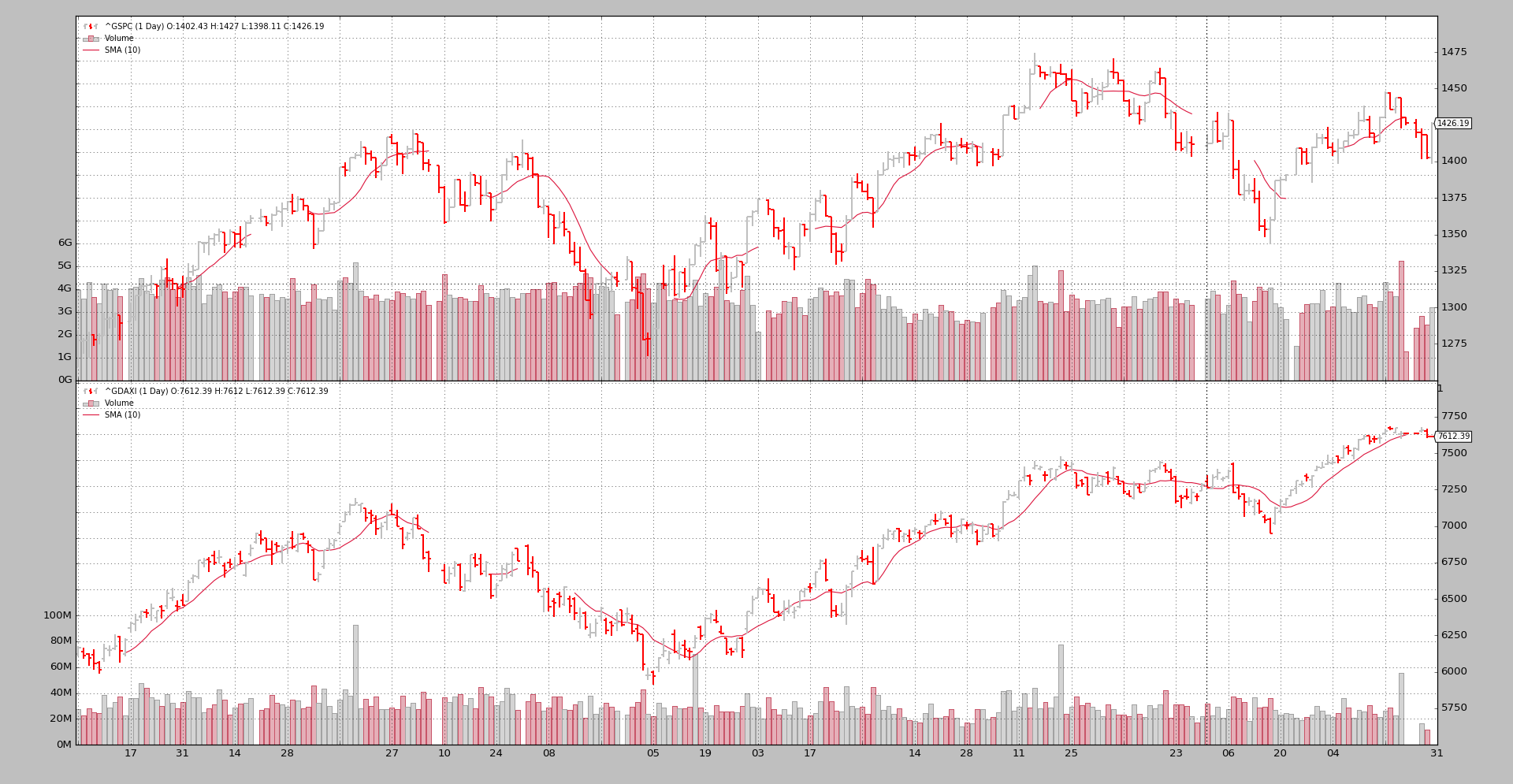

A 2nd plot will try to answer the question at the top: what happens with

indicators?. Remember that the new bars have been given a value of NaN

(that’s why they are not displayed):

$ ./weekdaysaligner.py --online --data0 '^GSPC' --data1 '^GDAXI' --filler --plot --sma 10

Re-blistering barnacles! The Simple Moving Average has broken the space time

continuum and jumps some bars with no solution of continuity. This is of course

the effect of filling up with Not a Number aka NaN: mathematic

operations no longer make sense.

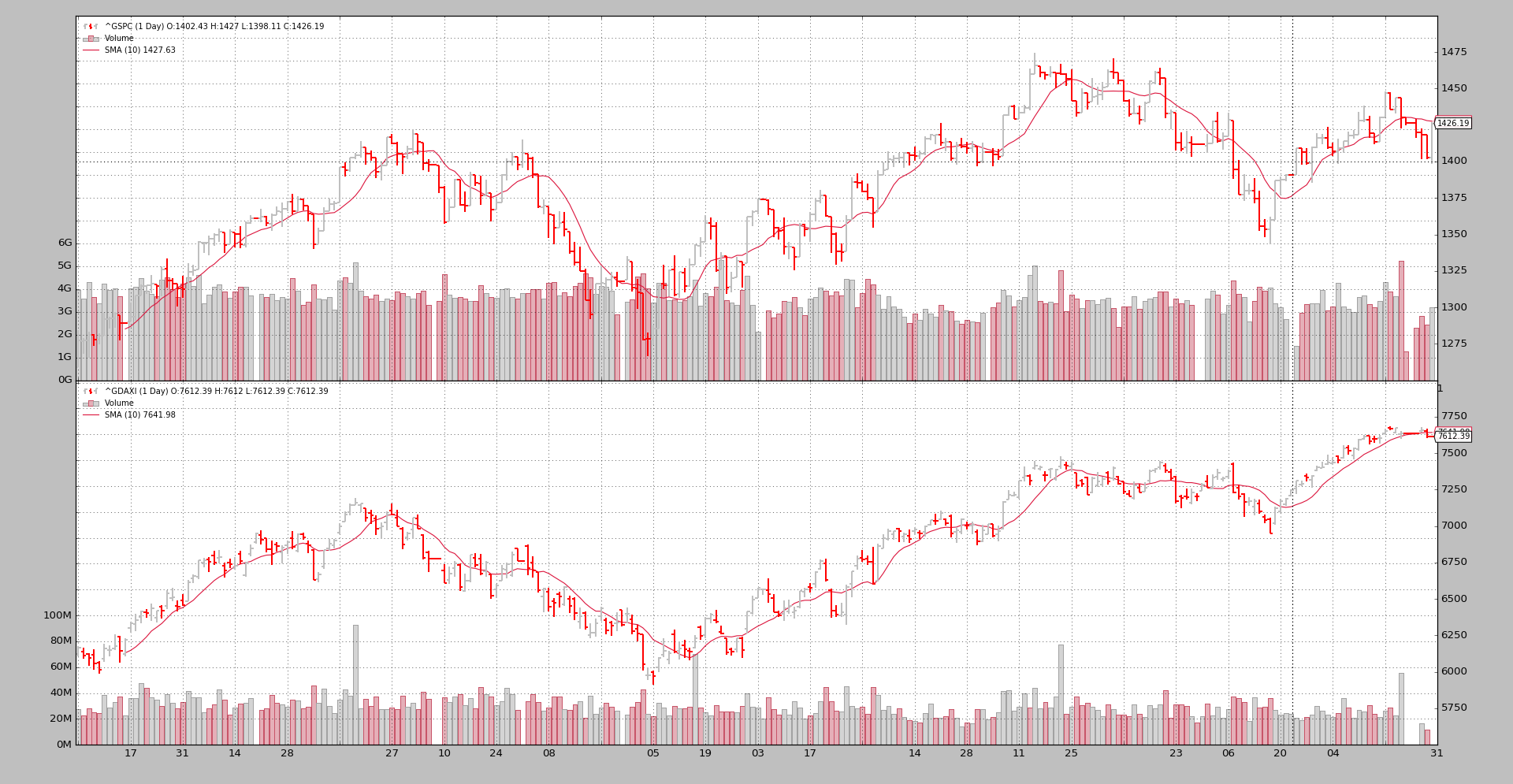

If instead of NaN the last seen closing price is used:

$ ./weekdaysaligner.py --online --data0 '^GSPC' --data1 '^GDAXI' --filler --plot --sma 10 --fillclose

The plot looks a lot nicer with a regular SMA for the entire 260 days

Conclusion

Synchronizing two instruments with different trading calendars is a matter of

making decisions and compromises. backtrader needs time aligned data to

work with multiple datas and different trading calendars don’t help.

The use of the WeekDaysFiller described here can alleviate the situation

but it is by no means a universal panacea, because with which values to fill is

a matter of long and prolonged consideration.

Script Code and Usage

Available as sample in the sources of backtrader:

$ ./weekdaysaligner.py --help

usage: weekdaysaligner.py [-h] [--online] --data0 DATA0 [--data1 DATA1]

[--sma SMA] [--fillclose] [--filler] [--filler0]

[--filler1] [--fromdate FROMDATE] [--todate TODATE]

[--plot]

Sample for aligning with trade

optional arguments:

-h, --help show this help message and exit

--online Fetch data online from Yahoo (default: False)

--data0 DATA0 Data 0 to be read in (default: None)

--data1 DATA1 Data 1 to be read in (default: None)

--sma SMA Add a sma to the datas (default: 0)

--fillclose Fill with Close price instead of NaN (default: False)

--filler Add Filler to Datas 0 and 1 (default: False)

--filler0 Add Filler to Data 0 (default: False)

--filler1 Add Filler to Data 1 (default: False)

--fromdate FROMDATE, -f FROMDATE

Starting date in YYYY-MM-DD format (default:

2012-01-01)

--todate TODATE, -t TODATE

Ending date in YYYY-MM-DD format (default: 2012-12-31)

--plot Do plot (default: False)

The code:

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

import backtrader.utils.flushfile

# from wkdaysfiller import WeekDaysFiller

from weekdaysfiller import WeekDaysFiller

class St(bt.Strategy):

params = (('sma', 0),)

def __init__(self):

if self.p.sma:

btind.SMA(self.data0, period=self.p.sma)

btind.SMA(self.data1, period=self.p.sma)

def next(self):

dtequal = (self.data0.datetime.datetime() ==

self.data1.datetime.datetime())

txt = ''

txt += '%04d, %5s' % (len(self), str(dtequal))

txt += ', data0, %s' % self.data0.datetime.datetime().isoformat()

txt += ', %s, data1' % self.data1.datetime.datetime().isoformat()

print(txt)

def runstrat():

args = parse_args()

fromdate = datetime.datetime.strptime(args.fromdate, '%Y-%m-%d')

todate = datetime.datetime.strptime(args.todate, '%Y-%m-%d')

cerebro = bt.Cerebro(stdstats=False)

DataFeed = btfeeds.YahooFinanceCSVData

if args.online:

DataFeed = btfeeds.YahooFinanceData

data0 = DataFeed(dataname=args.data0, fromdate=fromdate, todate=todate)

if args.data1:

data1 = DataFeed(dataname=args.data1, fromdate=fromdate, todate=todate)

else:

data1 = data0.clone()

if args.filler or args.filler0:

data0.addfilter(WeekDaysFiller, fillclose=args.fillclose)

if args.filler or args.filler1:

data1.addfilter(WeekDaysFiller, fillclose=args.fillclose)

cerebro.adddata(data0)

cerebro.adddata(data1)

cerebro.addstrategy(St, sma=args.sma)

cerebro.run(runonce=True, preload=True)

if args.plot:

cerebro.plot(style='bar')

def parse_args():

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description='Sample for aligning with trade ')

parser.add_argument('--online', required=False, action='store_true',

help='Fetch data online from Yahoo')

parser.add_argument('--data0', required=True, help='Data 0 to be read in')

parser.add_argument('--data1', required=False, help='Data 1 to be read in')

parser.add_argument('--sma', required=False, default=0, type=int,

help='Add a sma to the datas')

parser.add_argument('--fillclose', required=False, action='store_true',

help='Fill with Close price instead of NaN')

parser.add_argument('--filler', required=False, action='store_true',

help='Add Filler to Datas 0 and 1')

parser.add_argument('--filler0', required=False, action='store_true',

help='Add Filler to Data 0')

parser.add_argument('--filler1', required=False, action='store_true',

help='Add Filler to Data 1')

parser.add_argument('--fromdate', '-f', default='2012-01-01',

help='Starting date in YYYY-MM-DD format')

parser.add_argument('--todate', '-t', default='2012-12-31',

help='Ending date in YYYY-MM-DD format')

parser.add_argument('--plot', required=False, action='store_true',

help='Do plot')

return parser.parse_args()

if __name__ == '__main__':

runstrat()