Bracket Orders

Release 1.9.37.116 adds bracket orders giving a very broad spectrum of

orders which are supported by the backtesting broker (Market, Limit,

Close, Stop, StopLimit, StopTrail, StopTrailLimit, OCO)

Note

This is implemented for backtesting and for the Interactivers Brokers store

A bracket order isn’s a single order but it is actually made up of 3

orders. Let’s consider the long side

-

A main side

buyorder, usually set to be aLimitorStopLimitorder -

A low side

sellorder, usually set to be aStoporder to limit losses -

A high side

sellorder, usually set to be aLimitorder to take profit

With corresponding sell and 2 x buy orders for the short side.

The low/high side orders do actually create a bracket around the main side order.

To put some logic into it, the following rules apply:

-

The 3 orders are submitted together to avoid having any of them triggered independently

-

The low/high side orders are marked as children of the main side

-

The children are not active until the main side is executed

-

The cancellation of the main side cancels both the low and high side

-

The execution of the main side activates both the low and high side

-

Upon being active

- The execution or cancellation of any of low/high side orders automatically cancels the other

Usage Pattern

There are two possibilities to create the bracket set of orders

-

Single issuing of the 3 orders

-

Manual issuing of the 3 orders

Single Issuing of a Bracket

backtrader offers two new methods in the Strategy to control bracket

orders.

buy_bracketandsell_bracket

Note

Signature and info below or in the Strategy reference section.

With a single statement a complete set of 3 orders. An example:

brackets = self.buy_bracket(limitprice=14.00, price=13.50, stopprice=13.00)

Notice how stopprice and limitprice wrap the main price

This should be enough. The actual target data would be data0 and the

size would be automatically determined by the default sizer. Of course both

and many other parameters can be specified to have a fine control of the

execution.

The return value is:

- A

listcontaining the 3 orders in this order:[main, stop, limit]

Because when issuing a sell_bracket order, the low and high sides would be

turned aound, the parameters are named following convention stop and limit

-

stopis meant to stop the losses (low side in a long operation, and high side in a short operation) -

limitis meant to take the profit (high side in a long operation and low side in a short operation)

Manual Issuing of a Bracket

This involves the generation of the 3 orders and playing around with the

transmit and parent arguments. The rules:

-

The main side order must be created 1st and have

transmit=False -

The low/high side orders must have

parent=main_side_order -

The 1st low/high side order to be created must have

transmit=False -

The last order to be created (either the low or high side) sets

transmit=True

A practical example doing what the single command from above did:

mainside = self.buy(price=13.50, exectype=bt.Order.Limit, transmit=False)

lowside = self.sell(price=13.00, size=mainside.size, exectype=bt.Order.Stop,

transmit=False, parent=mainside)

highside = self.sell(price=14.00, size=mainside.size, exectype=bt.Order.Limit,

transmit=True, parent=mainside)

Where there is a lot more to do:

-

Keep track of the

mainsideorder to indicate it is the parent of the others -

Control

transmitto make sure only the last order triggers the joint transmission -

Specify the execution types

-

Specify the

sizefor the low and high sideBecause the

sizeMUST be the same. If the parameter were not specified manually and the end user had introduced a sizer, the sizer could actually indicate a different value for the orders. That’s why it has to be manually added to the calls after it has been set for themainsideorder.

A sample of it

Running the sample from below produces this output (capped for brevity)

$ ./bracket.py --plot

2005-01-28: Oref 1 / Buy at 2941.11055

2005-01-28: Oref 2 / Sell Stop at 2881.99275

2005-01-28: Oref 3 / Sell Limit at 3000.22835

2005-01-31: Order ref: 1 / Type Buy / Status Submitted

2005-01-31: Order ref: 2 / Type Sell / Status Submitted

2005-01-31: Order ref: 3 / Type Sell / Status Submitted

2005-01-31: Order ref: 1 / Type Buy / Status Accepted

2005-01-31: Order ref: 2 / Type Sell / Status Accepted

2005-01-31: Order ref: 3 / Type Sell / Status Accepted

2005-02-01: Order ref: 1 / Type Buy / Status Expired

2005-02-01: Order ref: 2 / Type Sell / Status Canceled

2005-02-01: Order ref: 3 / Type Sell / Status Canceled

...

2005-08-11: Oref 16 / Buy at 3337.3892

2005-08-11: Oref 17 / Sell Stop at 3270.306

2005-08-11: Oref 18 / Sell Limit at 3404.4724

2005-08-12: Order ref: 16 / Type Buy / Status Submitted

2005-08-12: Order ref: 17 / Type Sell / Status Submitted

2005-08-12: Order ref: 18 / Type Sell / Status Submitted

2005-08-12: Order ref: 16 / Type Buy / Status Accepted

2005-08-12: Order ref: 17 / Type Sell / Status Accepted

2005-08-12: Order ref: 18 / Type Sell / Status Accepted

2005-08-12: Order ref: 16 / Type Buy / Status Completed

2005-08-18: Order ref: 17 / Type Sell / Status Completed

2005-08-18: Order ref: 18 / Type Sell / Status Canceled

...

2005-09-26: Oref 22 / Buy at 3383.92535

2005-09-26: Oref 23 / Sell Stop at 3315.90675

2005-09-26: Oref 24 / Sell Limit at 3451.94395

2005-09-27: Order ref: 22 / Type Buy / Status Submitted

2005-09-27: Order ref: 23 / Type Sell / Status Submitted

2005-09-27: Order ref: 24 / Type Sell / Status Submitted

2005-09-27: Order ref: 22 / Type Buy / Status Accepted

2005-09-27: Order ref: 23 / Type Sell / Status Accepted

2005-09-27: Order ref: 24 / Type Sell / Status Accepted

2005-09-27: Order ref: 22 / Type Buy / Status Completed

2005-10-04: Order ref: 24 / Type Sell / Status Completed

2005-10-04: Order ref: 23 / Type Sell / Status Canceled

...

Where 3 different outcomes are shown:

-

In the 1st case the main side order expired and this automatically cancelled the other two

-

In the 2nd case the main side order was completed and the low (stop in the buy case) was executed limiting losses

-

In the 3rd case the main side order was completed and the high side (limit) was executed

This can be noticed because the Completed ids are

22and24and the high side order is being issued last, which means the non-executed low side order has id 23.

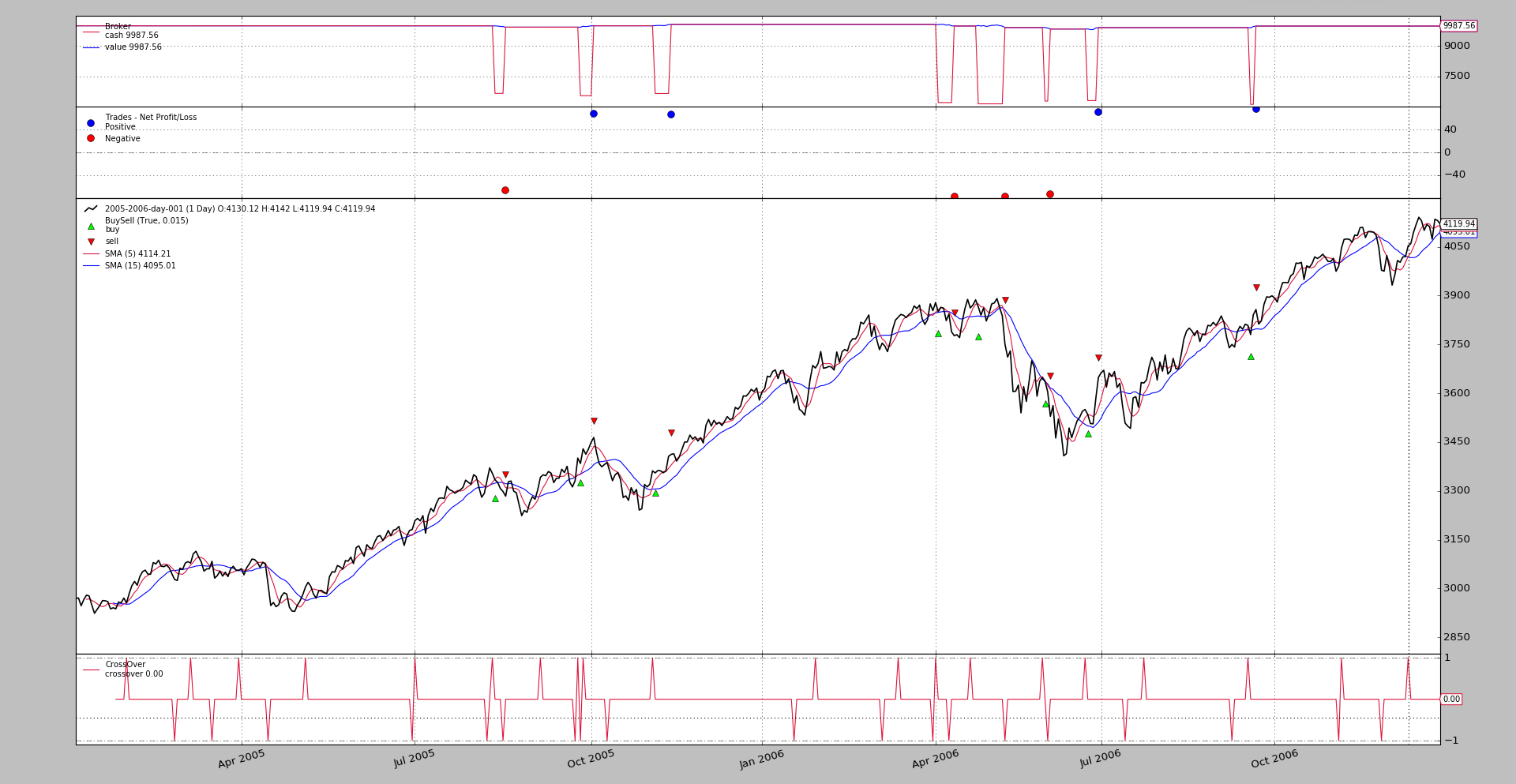

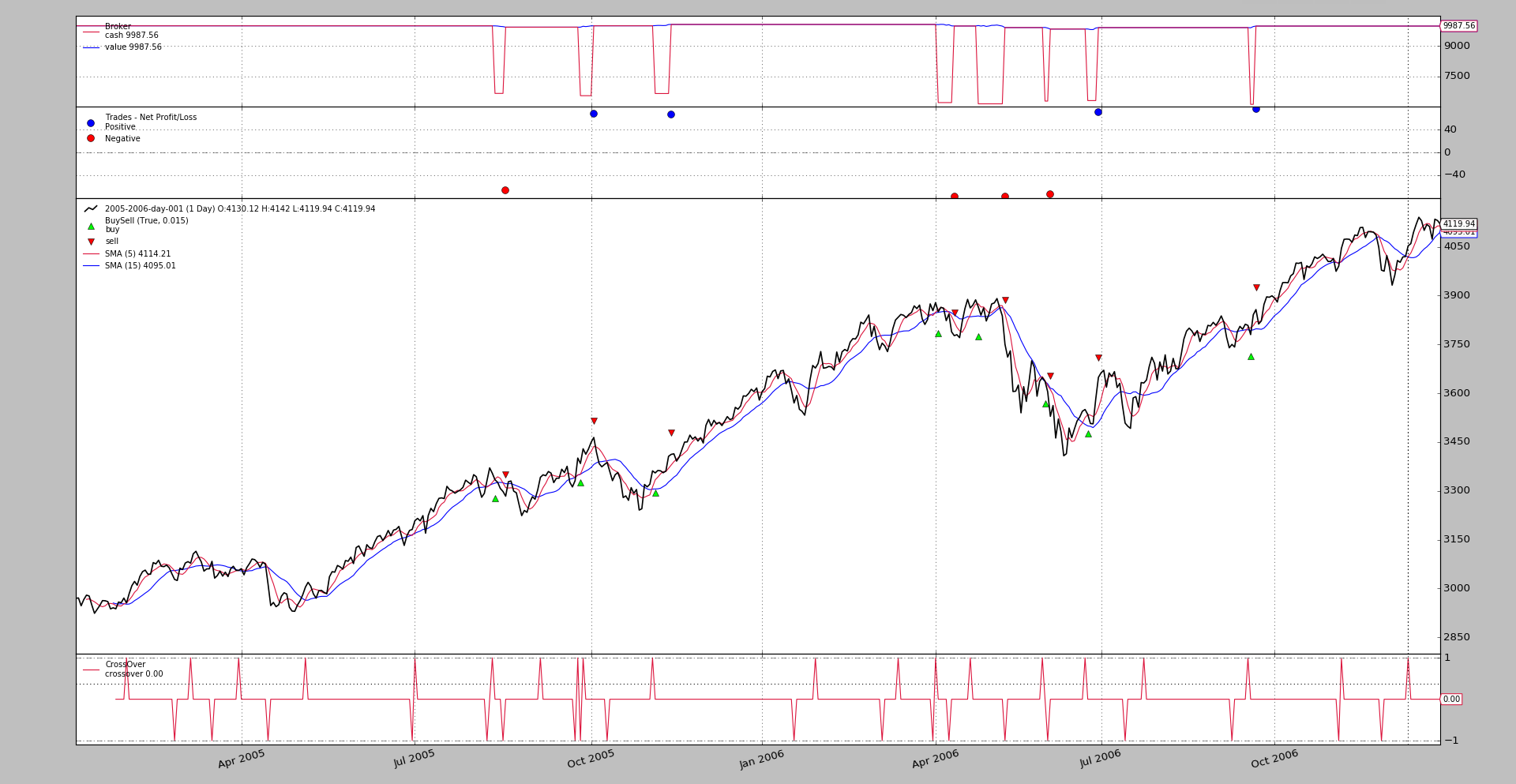

Visually

It can be immediately seen that the losing trades align around the same value and winning trades too, which is the purpose of the backeting. Controlling both sides.

The sample as run issues the 3 orders manually, but it can be told to use

buy_bracket. Let’s see the output:

$ ./bracket.py --strat usebracket=True

With the same result

Some reference

See the new buy_bracket and sell_bracket methods

def buy_bracket(self, data=None, size=None, price=None, plimit=None,

exectype=bt.Order.Limit, valid=None, tradeid=0,

trailamount=None, trailpercent=None, oargs={},

stopprice=None, stopexec=bt.Order.Stop, stopargs={},

limitprice=None, limitexec=bt.Order.Limit, limitargs={},

**kwargs):

'''

Create a bracket order group (low side - buy order - high side). The

default behavior is as follows:

- Issue a **buy** order with execution ``Limit`

- Issue a *low side* bracket **sell** order with execution ``Stop``

- Issue a *high side* bracket **sell** order with execution

``Limit``.

See below for the different parameters

- ``data`` (default: ``None``)

For which data the order has to be created. If ``None`` then the

first data in the system, ``self.datas[0] or self.data0`` (aka

``self.data``) will be used

- ``size`` (default: ``None``)

Size to use (positive) of units of data to use for the order.

If ``None`` the ``sizer`` instance retrieved via ``getsizer`` will

be used to determine the size.

**Note**: The same size is applied to all 3 orders of the bracket

- ``price`` (default: ``None``)

Price to use (live brokers may place restrictions on the actual

format if it does not comply to minimum tick size requirements)

``None`` is valid for ``Market`` and ``Close`` orders (the market

determines the price)

For ``Limit``, ``Stop`` and ``StopLimit`` orders this value

determines the trigger point (in the case of ``Limit`` the trigger

is obviously at which price the order should be matched)

- ``plimit`` (default: ``None``)

Only applicable to ``StopLimit`` orders. This is the price at which

to set the implicit *Limit* order, once the *Stop* has been

triggered (for which ``price`` has been used)

- ``trailamount`` (default: ``None``)

If the order type is StopTrail or StopTrailLimit, this is an

absolute amount which determines the distance to the price (below

for a Sell order and above for a buy order) to keep the trailing

stop

- ``trailpercent`` (default: ``None``)

If the order type is StopTrail or StopTrailLimit, this is a

percentage amount which determines the distance to the price (below

for a Sell order and above for a buy order) to keep the trailing

stop (if ``trailamount`` is also specified it will be used)

- ``exectype`` (default: ``bt.Order.Limit``)

Possible values: (see the documentation for the method ``buy``

- ``valid`` (default: ``None``)

Possible values: (see the documentation for the method ``buy``

- ``tradeid`` (default: ``0``)

Possible values: (see the documentation for the method ``buy``

- ``oargs`` (default: ``{}``)

Specific keyword arguments (in a ``dict``) to pass to the main side

order. Arguments from the default ``**kwargs`` will be applied on

top of this.

- ``**kwargs``: additional broker implementations may support extra

parameters. ``backtrader`` will pass the *kwargs* down to the

created order objects

Possible values: (see the documentation for the method ``buy``

**Note**: this ``kwargs`` will be applied to the 3 orders of a

bracket. See below for specific keyword arguments for the low and

high side orders

- ``stopprice`` (default: ``None``)

Specific price for the *low side* stop order

- ``stopexec`` (default: ``bt.Order.Stop``)

Specific execution type for the *low side* order

- ``stopargs`` (default: ``{}``)

Specific keyword arguments (in a ``dict``) to pass to the low side

order. Arguments from the default ``**kwargs`` will be applied on

top of this.

- ``limitprice`` (default: ``None``)

Specific price for the *high side* stop order

- ``stopexec`` (default: ``bt.Order.Limit``)

Specific execution type for the *high side* order

- ``limitargs`` (default: ``{}``)

Specific keyword arguments (in a ``dict``) to pass to the high side

order. Arguments from the default ``**kwargs`` will be applied on

top of this.

Returns:

- A list containing the 3 bracket orders [order, stop side, limit

side]

'''

def sell_bracket(self, data=None,

size=None, price=None, plimit=None,

exectype=bt.Order.Limit, valid=None, tradeid=0,

trailamount=None, trailpercent=None,

oargs={},

stopprice=None, stopexec=bt.Order.Stop, stopargs={},

limitprice=None, limitexec=bt.Order.Limit, limitargs={},

**kwargs):

'''

Create a bracket order group (low side - buy order - high side). The

default behavior is as follows:

- Issue a **sell** order with execution ``Limit`

- Issue a *high side* bracket **buy** order with execution ``Stop``

- Issue a *low side* bracket **buy** order with execution ``Limit``.

See ``bracket_buy`` for the meaning of the parameters

Returns:

- A list containing the 3 bracket orders [order, stop side, limit

side]

'''

Sample usage

$ ./bracket.py --help

usage: bracket.py [-h] [--data0 DATA0] [--fromdate FROMDATE] [--todate TODATE]

[--cerebro kwargs] [--broker kwargs] [--sizer kwargs]

[--strat kwargs] [--plot [kwargs]]

Sample Skeleton

optional arguments:

-h, --help show this help message and exit

--data0 DATA0 Data to read in (default:

../../datas/2005-2006-day-001.txt)

--fromdate FROMDATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default: )

--todate TODATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default: )

--cerebro kwargs kwargs in key=value format (default: )

--broker kwargs kwargs in key=value format (default: )

--sizer kwargs kwargs in key=value format (default: )

--strat kwargs kwargs in key=value format (default: )

--plot [kwargs] kwargs in key=value format (default: )

Sample Code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import backtrader as bt

class St(bt.Strategy):

params = dict(

ma=bt.ind.SMA,

p1=5,

p2=15,

limit=0.005,

limdays=3,

limdays2=1000,

hold=10,

usebracket=False, # use order_target_size

switchp1p2=False, # switch prices of order1 and order2

)

def notify_order(self, order):

print('{}: Order ref: {} / Type {} / Status {}'.format(

self.data.datetime.date(0),

order.ref, 'Buy' * order.isbuy() or 'Sell',

order.getstatusname()))

if order.status == order.Completed:

self.holdstart = len(self)

if not order.alive() and order.ref in self.orefs:

self.orefs.remove(order.ref)

def __init__(self):

ma1, ma2 = self.p.ma(period=self.p.p1), self.p.ma(period=self.p.p2)

self.cross = bt.ind.CrossOver(ma1, ma2)

self.orefs = list()

if self.p.usebracket:

print('-' * 5, 'Using buy_bracket')

def next(self):

if self.orefs:

return # pending orders do nothing

if not self.position:

if self.cross > 0.0: # crossing up

close = self.data.close[0]

p1 = close * (1.0 - self.p.limit)

p2 = p1 - 0.02 * close

p3 = p1 + 0.02 * close

valid1 = datetime.timedelta(self.p.limdays)

valid2 = valid3 = datetime.timedelta(self.p.limdays2)

if self.p.switchp1p2:

p1, p2 = p2, p1

valid1, valid2 = valid2, valid1

if not self.p.usebracket:

o1 = self.buy(exectype=bt.Order.Limit,

price=p1,

valid=valid1,

transmit=False)

print('{}: Oref {} / Buy at {}'.format(

self.datetime.date(), o1.ref, p1))

o2 = self.sell(exectype=bt.Order.Stop,

price=p2,

valid=valid2,

parent=o1,

transmit=False)

print('{}: Oref {} / Sell Stop at {}'.format(

self.datetime.date(), o2.ref, p2))

o3 = self.sell(exectype=bt.Order.Limit,

price=p3,

valid=valid3,

parent=o1,

transmit=True)

print('{}: Oref {} / Sell Limit at {}'.format(

self.datetime.date(), o3.ref, p3))

self.orefs = [o1.ref, o2.ref, o3.ref]

else:

os = self.buy_bracket(

price=p1, valid=valid1,

stopprice=p2, stopargs=dict(valid=valid2),

limitprice=p3, limitargs=dict(valid=valid3),)

self.orefs = [o.ref for o in os]

else: # in the market

if (len(self) - self.holdstart) >= self.p.hold:

pass # do nothing in this case

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

# Data feed kwargs

kwargs = dict()

# Parse from/to-date

dtfmt, tmfmt = '%Y-%m-%d', 'T%H:%M:%S'

for a, d in ((getattr(args, x), x) for x in ['fromdate', 'todate']):

if a:

strpfmt = dtfmt + tmfmt * ('T' in a)

kwargs[d] = datetime.datetime.strptime(a, strpfmt)

# Data feed

data0 = bt.feeds.BacktraderCSVData(dataname=args.data0, **kwargs)

cerebro.adddata(data0)

# Broker

cerebro.broker = bt.brokers.BackBroker(**eval('dict(' + args.broker + ')'))

# Sizer

cerebro.addsizer(bt.sizers.FixedSize, **eval('dict(' + args.sizer + ')'))

# Strategy

cerebro.addstrategy(St, **eval('dict(' + args.strat + ')'))

# Execute

cerebro.run(**eval('dict(' + args.cerebro + ')'))

if args.plot: # Plot if requested to

cerebro.plot(**eval('dict(' + args.plot + ')'))

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description=(

'Sample Skeleton'

)

)

parser.add_argument('--data0', default='../../datas/2005-2006-day-001.txt',

required=False, help='Data to read in')

# Defaults for dates

parser.add_argument('--fromdate', required=False, default='',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--todate', required=False, default='',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--cerebro', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--broker', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--sizer', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--strat', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--plot', required=False, default='',

nargs='?', const='{}',

metavar='kwargs', help='kwargs in key=value format')

return parser.parse_args(pargs)

if __name__ == '__main__':

runstrat()