Automating backtrader BackTesting

So far all backtrader examples and working samples have started from scratch creating a main Python module which loads datas, strategies, observers and prepares cash and commission schemes.

One of the goals of algorithmic trading is the automation of trading and given that bactrader is a backtesting platform intented to check trading algorithms (hence is an algotrading platform), automating the use of backtrader was an obvious goal.

Note

Aug 22, 2015

Analyzer support in bt-run.py included

The development version of backtrader now contains the bt-run.py script

which automates most tasks and will be installed along backtrader as part of

a regular package.

bt-run.py allows the end user to:

-

Say which datas have to be loaded

-

Set the format to load the datas

-

Specify the date range for the datas

-

Disable standard observers

-

Load one or more observers (example: DrawDown) from the built-in ones or from a python module

-

Set the cash and commission scheme parameters for the broker (commission, margin, mult)

-

Enable plotting, controlling the amount of charts and style to present the data

And finally:

-

Load a strategy (a built-in one or from a Python module)

-

Pass parameters to the loaded strategy

See below for the Usage* of the script.

Applying a User Defined Strategy

Let’s consider the following strategy which:

-

Simply loads a SimpleMovingAverage (default period 15)

-

Prints outs

-

Is in a fily with the name mymod.py

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import backtrader as bt

import backtrader.indicators as btind

class MyTest(bt.Strategy):

params = (('period', 15),)

def log(self, txt, dt=None):

''' Logging function fot this strategy'''

dt = dt or self.data.datetime[0]

if isinstance(dt, float):

dt = bt.num2date(dt)

print('%s, %s' % (dt.isoformat(), txt))

def __init__(self):

sma = btind.SMA(period=self.p.period)

def next(self):

ltxt = '%d, %.2f, %.2f, %.2f, %.2f, %.2f, %.2f'

self.log(ltxt %

(len(self),

self.data.open[0], self.data.high[0],

self.data.low[0], self.data.close[0],

self.data.volume[0], self.data.openinterest[0]))

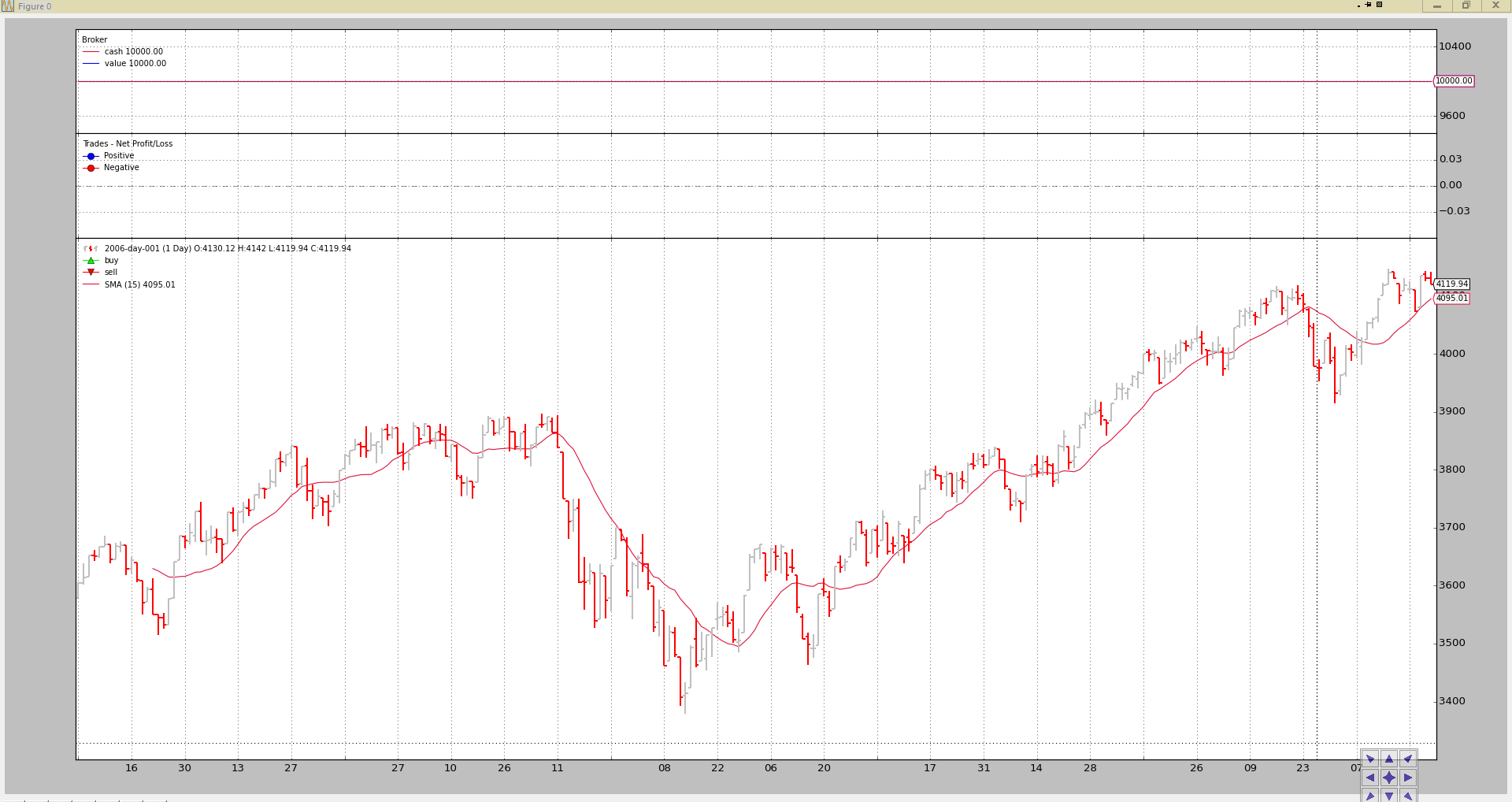

Executing the strategy with the usual testing sample is easy: easy:

./bt-run.py --csvformat btcsv \

--data ../samples/data/sample/2006-day-001.txt \

--strategy ./mymod.py

The chart output

The console output:

2006-01-20T23:59:59+00:00, 15, 3593.16, 3612.37, 3550.80, 3550.80, 0.00, 0.00

2006-01-23T23:59:59+00:00, 16, 3550.24, 3550.24, 3515.07, 3544.31, 0.00, 0.00

2006-01-24T23:59:59+00:00, 17, 3544.78, 3553.16, 3526.37, 3532.68, 0.00, 0.00

2006-01-25T23:59:59+00:00, 18, 3532.72, 3578.00, 3532.72, 3578.00, 0.00, 0.00

...

...

2006-12-22T23:59:59+00:00, 252, 4109.86, 4109.86, 4072.62, 4073.50, 0.00, 0.00

2006-12-27T23:59:59+00:00, 253, 4079.70, 4134.86, 4079.70, 4134.86, 0.00, 0.00

2006-12-28T23:59:59+00:00, 254, 4137.44, 4142.06, 4125.14, 4130.66, 0.00, 0.00

2006-12-29T23:59:59+00:00, 255, 4130.12, 4142.01, 4119.94, 4119.94, 0.00, 0.00

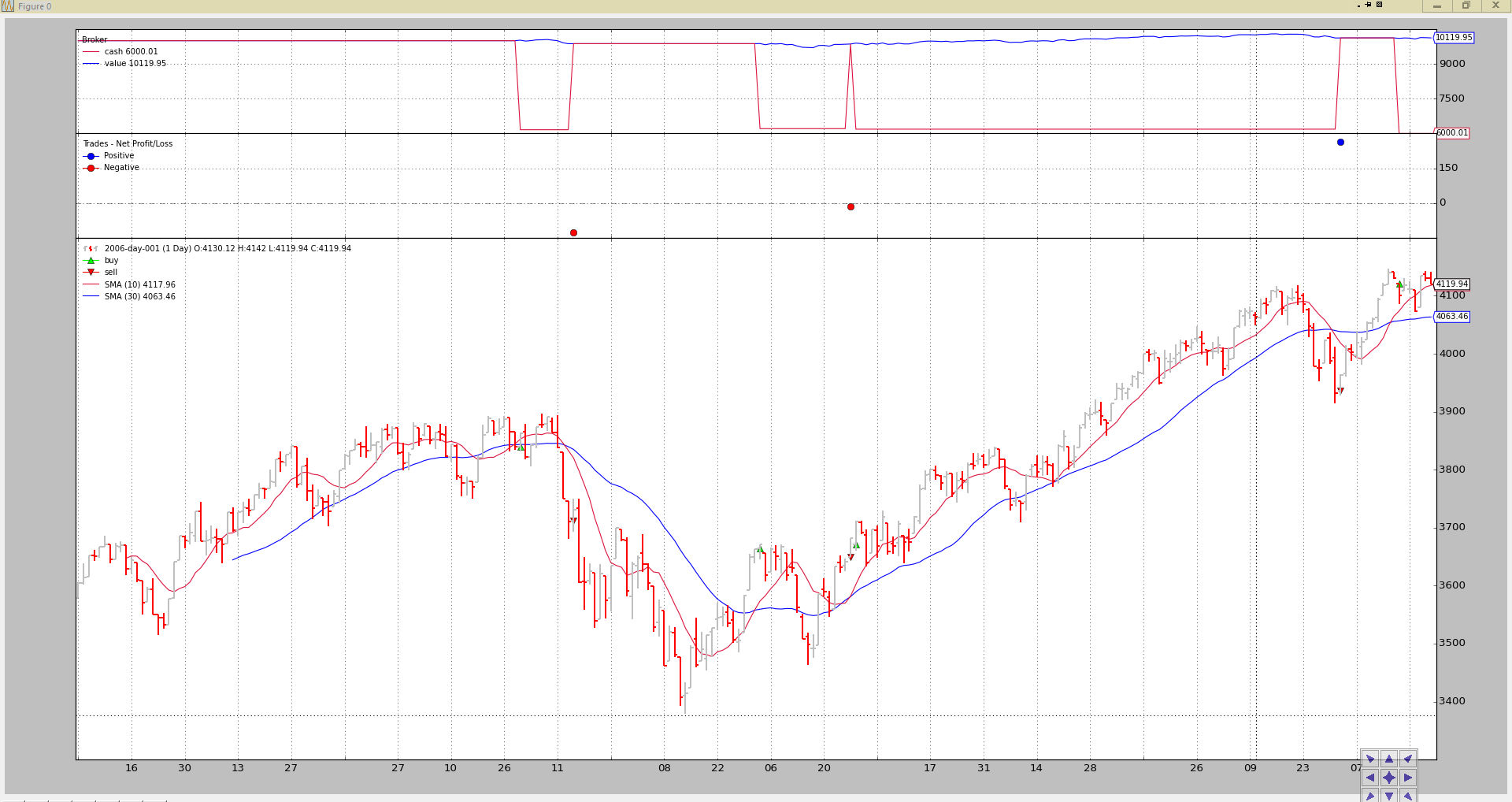

Same strategy but:

- Setting the parameter

periodto 50

The command line:

./bt-run.py --csvformat btcsv \

--data ../samples/data/sample/2006-day-001.txt \

--strategy ./mymod.py \

period 50

The chart output.

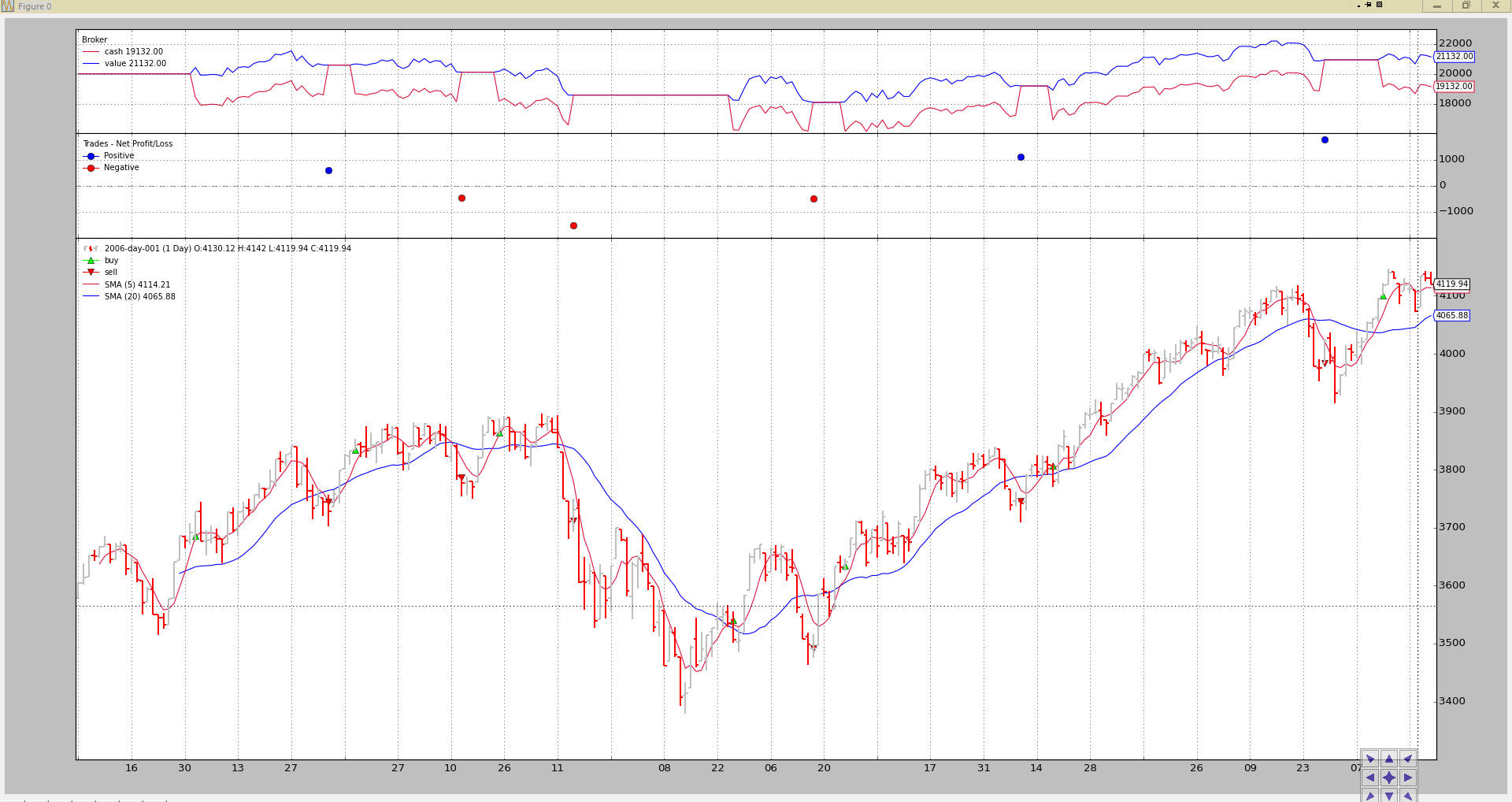

Using a built-in Strategy

backtrader will slowly be including sample (textbook) strategies. Along with

the bt-run.py script a standard Simple Moving Average CrossOver strategy

is included. The name:

-

SMA_CrossOver -

Parameters

-

fast (default 10) period of the fast moving average

-

slow (default 30) period of the slow moving average

-

The strategy buys if the fast moving average crosses up the fast and sells (only if it has bought before) upon the fast moving average crossing down the slow moving average.

The code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import backtrader as bt

import backtrader.indicators as btind

class SMA_CrossOver(bt.Strategy):

params = (('fast', 10), ('slow', 30))

def __init__(self):

sma_fast = btind.SMA(period=self.p.fast)

sma_slow = btind.SMA(period=self.p.slow)

self.buysig = btind.CrossOver(sma_fast, sma_slow)

def next(self):

if self.position.size:

if self.buysig < 0:

self.sell()

elif self.buysig > 0:

self.buy()

Standard execution:

./bt-run.py --csvformat btcsv \

--data ../samples/data/sample/2006-day-001.txt \

--strategy :SMA_CrossOver

Notice the ‘:’. The standard notation (see below) to load a strategy is:

- module:stragegy

With the following rules:

-

If module is there and strategy is specified, then that strategy will be used

-

If module is there but no strategy is specified, the 1st strategy found in the module will be returned

-

If no module is specified, “strategy” is assumed to refer to a strategy in the

backtraderpackage

The latter being our case.

The output.

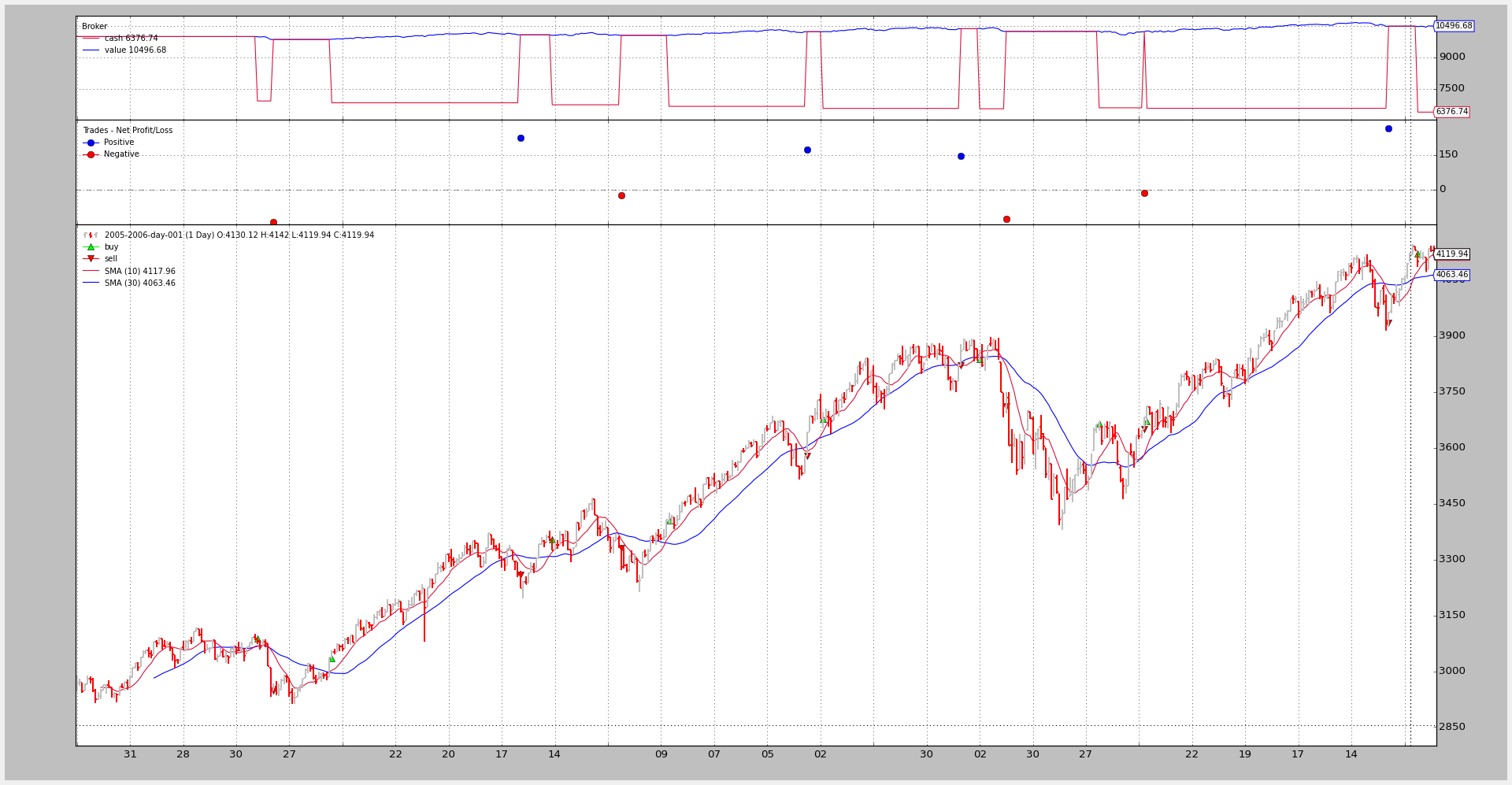

One last example adding commission schemes, cash and changing the parameters:

./bt-run.py --csvformat btcsv \

--data ../samples/data/sample/2006-day-001.txt \

--cash 20000 \

--commission 2.0 \

--mult 10 \

--margin 2000 \

--strategy :SMA_CrossOver \

fast 5 slow 20

The output.

We have backtested the strategy:

-

Changing the moving average periods

-

Setting a new starting cash

-

Putting a commission scheme in place for a futures-like instrument

See the continuous variations in cash with each bar, as cash is adjusted for the futures-like instrument daily changes

Adding Analyzers

Note

Added Analyzer example

bt-run.py also supports adding Analyzers with the same syntax used for

the strategies to choose between internal/external analyzers.

Example with a SharpeRatio analysis for the years 2005-2006:

./bt-run.py --csvformat btcsv \

--data ../samples/data/sample/2005-2006-day-001.txt \

--strategy :SMA_CrossOver \

--analyzer :SharpeRatio

The output:

====================

== Analyzers

====================

## sharperatio

-- sharperatio : 11.6473326097

Good strategy!!! (Pure luck for the example actually which also bears no commissions)

The chart (which simply shows the Analyzer is not in the plot, because Analyzers cannot be plotted, they aren’t lines objects)

Usage of the script

Directly from the script:

$ ./bt-run.py --help

usage: bt-run.py [-h] --data DATA

[--csvformat {yahoocsv_unreversed,vchart,sierracsv,yahoocsv,vchartcsv,btcsv}]

[--fromdate FROMDATE] [--todate TODATE] --strategy STRATEGY

[--nostdstats] [--observer OBSERVERS] [--analyzer ANALYZERS]

[--cash CASH] [--commission COMMISSION] [--margin MARGIN]

[--mult MULT] [--noplot] [--plotstyle {bar,line,candle}]

[--plotfigs PLOTFIGS]

...

Backtrader Run Script

positional arguments:

args args to pass to the loaded strategy

optional arguments:

-h, --help show this help message and exit

Data options:

--data DATA, -d DATA Data files to be added to the system

--csvformat {yahoocsv_unreversed,vchart,sierracsv,yahoocsv,vchartcsv,btcsv}, -c {yahoocsv_unreversed,vchart,sierracsv,yahoocsv,vchartcsv,btcsv}

CSV Format

--fromdate FROMDATE, -f FROMDATE

Starting date in YYYY-MM-DD[THH:MM:SS] format

--todate TODATE, -t TODATE

Ending date in YYYY-MM-DD[THH:MM:SS] format

Strategy options:

--strategy STRATEGY, -st STRATEGY

Module and strategy to load with format

module_path:strategy_name. module_path:strategy_name

will load strategy_name from the given module_path

module_path will load the module and return the first

available strategy in the module :strategy_name will

load the given strategy from the set of built-in

strategies

Observers and statistics:

--nostdstats Disable the standard statistics observers

--observer OBSERVERS, -ob OBSERVERS

This option can be specified multiple times Module and

observer to load with format

module_path:observer_name. module_path:observer_name

will load observer_name from the given module_path

module_path will load the module and return all

available observers in the module :observer_name will

load the given strategy from the set of built-in

strategies

Analyzers:

--analyzer ANALYZERS, -an ANALYZERS

This option can be specified multiple times Module and

analyzer to load with format

module_path:analzyer_name. module_path:analyzer_name

will load observer_name from the given module_path

module_path will load the module and return all

available analyzers in the module :anaylzer_name will

load the given strategy from the set of built-in

strategies

Cash and Commission Scheme Args:

--cash CASH, -cash CASH

Cash to set to the broker

--commission COMMISSION, -comm COMMISSION

Commission value to set

--margin MARGIN, -marg MARGIN

Margin type to set

--mult MULT, -mul MULT

Multiplier to use

Plotting options:

--noplot, -np Do not plot the read data

--plotstyle {bar,line,candle}, -ps {bar,line,candle}

Plot style for the input data

--plotfigs PLOTFIGS, -pn PLOTFIGS

Plot using n figures

And the code:

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import inspect

import itertools

import random

import string

import sys

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btinds

import backtrader.observers as btobs

import backtrader.strategies as btstrats

import backtrader.analyzers as btanalyzers

DATAFORMATS = dict(

btcsv=btfeeds.BacktraderCSVData,

vchartcsv=btfeeds.VChartCSVData,

vchart=btfeeds.VChartData,

sierracsv=btfeeds.SierraChartCSVData,

yahoocsv=btfeeds.YahooFinanceCSVData,

yahoocsv_unreversed=btfeeds.YahooFinanceCSVData

)

def runstrat():

args = parse_args()

stdstats = not args.nostdstats

cerebro = bt.Cerebro(stdstats=stdstats)

for data in getdatas(args):

cerebro.adddata(data)

# Prepare a dictionary of extra args passed to push them to the strategy

# pack them in pairs

packedargs = itertools.izip_longest(*[iter(args.args)] * 2, fillvalue='')

# prepare a string for evaluation, eval and store the result

evalargs = 'dict('

for key, value in packedargs:

evalargs += key + '=' + value + ','

evalargs += ')'

stratkwargs = eval(evalargs)

# Get the strategy and add it with any arguments

strat = getstrategy(args)

cerebro.addstrategy(strat, **stratkwargs)

obs = getobservers(args)

for ob in obs:

cerebro.addobserver(ob)

ans = getanalyzers(args)

for an in ans:

cerebro.addanalyzer(an)

setbroker(args, cerebro)

runsts = cerebro.run()

runst = runsts[0] # single strategy and no optimization

if runst.analyzers:

print('====================')

print('== Analyzers')

print('====================')

for name, analyzer in runst.analyzers.getitems():

print('## ', name)

analysis = analyzer.get_analysis()

for key, val in analysis.items():

print('-- ', key, ':', val)

if not args.noplot:

cerebro.plot(numfigs=args.plotfigs, style=args.plotstyle)

def setbroker(args, cerebro):

broker = cerebro.getbroker()

if args.cash is not None:

broker.setcash(args.cash)

commkwargs = dict()

if args.commission is not None:

commkwargs['commission'] = args.commission

if args.margin is not None:

commkwargs['margin'] = args.margin

if args.mult is not None:

commkwargs['mult'] = args.mult

if commkwargs:

broker.setcommission(**commkwargs)

def getdatas(args):

# Get the data feed class from the global dictionary

dfcls = DATAFORMATS[args.csvformat]

# Prepare some args

dfkwargs = dict()

if args.csvformat == 'yahoo_unreversed':

dfkwargs['reverse'] = True

fmtstr = '%Y-%m-%d'

if args.fromdate:

dtsplit = args.fromdate.split('T')

if len(dtsplit) > 1:

fmtstr += 'T%H:%M:%S'

fromdate = datetime.datetime.strptime(args.fromdate, fmtstr)

dfkwargs['fromdate'] = fromdate

fmtstr = '%Y-%m-%d'

if args.todate:

dtsplit = args.todate.split('T')

if len(dtsplit) > 1:

fmtstr += 'T%H:%M:%S'

todate = datetime.datetime.strptime(args.todate, fmtstr)

dfkwargs['todate'] = todate

datas = list()

for dname in args.data:

dfkwargs['dataname'] = dname

data = dfcls(**dfkwargs)

datas.append(data)

return datas

def getmodclasses(mod, clstype, clsname=None):

clsmembers = inspect.getmembers(mod, inspect.isclass)

clslist = list()

for name, cls in clsmembers:

if not issubclass(cls, clstype):

continue

if clsname:

if clsname == name:

clslist.append(cls)

break

else:

clslist.append(cls)

return clslist

def loadmodule(modpath, modname=''):

# generate a random name for the module

if not modname:

chars = string.ascii_uppercase + string.digits

modname = ''.join(random.choice(chars) for _ in range(10))

version = (sys.version_info[0], sys.version_info[1])

if version < (3, 3):

mod, e = loadmodule2(modpath, modname)

else:

mod, e = loadmodule3(modpath, modname)

return mod, e

def loadmodule2(modpath, modname):

import imp

try:

mod = imp.load_source(modname, modpath)

except Exception, e:

return (None, e)

return (mod, None)

def loadmodule3(modpath, modname):

import importlib.machinery

try:

loader = importlib.machinery.SourceFileLoader(modname, modpath)

mod = loader.load_module()

except Exception, e:

return (None, e)

return (mod, None)

def getstrategy(args):

sttokens = args.strategy.split(':')

if len(sttokens) == 1:

modpath = sttokens[0]

stname = None

else:

modpath, stname = sttokens

if modpath:

mod, e = loadmodule(modpath)

if not mod:

print('')

print('Failed to load module %s:' % modpath, e)

sys.exit(1)

else:

mod = btstrats

strats = getmodclasses(mod=mod, clstype=bt.Strategy, clsname=stname)

if not strats:

print('No strategy %s / module %s' % (str(stname), modpath))

sys.exit(1)

return strats[0]

def getanalyzers(args):

analyzers = list()

for anspec in args.analyzers or []:

tokens = anspec.split(':')

if len(tokens) == 1:

modpath = tokens[0]

name = None

else:

modpath, name = tokens

if modpath:

mod, e = loadmodule(modpath)

if not mod:

print('')

print('Failed to load module %s:' % modpath, e)

sys.exit(1)

else:

mod = btanalyzers

loaded = getmodclasses(mod=mod, clstype=bt.Analyzer, clsname=name)

if not loaded:

print('No analyzer %s / module %s' % ((str(name), modpath)))

sys.exit(1)

analyzers.extend(loaded)

return analyzers

def getobservers(args):

observers = list()

for obspec in args.observers or []:

tokens = obspec.split(':')

if len(tokens) == 1:

modpath = tokens[0]

name = None

else:

modpath, name = tokens

if modpath:

mod, e = loadmodule(modpath)

if not mod:

print('')

print('Failed to load module %s:' % modpath, e)

sys.exit(1)

else:

mod = btobs

loaded = getmodclasses(mod=mod, clstype=bt.Observer, clsname=name)

if not loaded:

print('No observer %s / module %s' % ((str(name), modpath)))

sys.exit(1)

observers.extend(loaded)

return observers

def parse_args():

parser = argparse.ArgumentParser(

description='Backtrader Run Script')

group = parser.add_argument_group(title='Data options')

# Data options

group.add_argument('--data', '-d', action='append', required=True,

help='Data files to be added to the system')

datakeys = list(DATAFORMATS.keys())

group.add_argument('--csvformat', '-c', required=False,

default='btcsv', choices=datakeys,

help='CSV Format')

group.add_argument('--fromdate', '-f', required=False, default=None,

help='Starting date in YYYY-MM-DD[THH:MM:SS] format')

group.add_argument('--todate', '-t', required=False, default=None,

help='Ending date in YYYY-MM-DD[THH:MM:SS] format')

# Module where to read the strategy from

group = parser.add_argument_group(title='Strategy options')

group.add_argument('--strategy', '-st', required=True,

help=('Module and strategy to load with format '

'module_path:strategy_name.\n'

'\n'

'module_path:strategy_name will load '

'strategy_name from the given module_path\n'

'\n'

'module_path will load the module and return '

'the first available strategy in the module\n'

'\n'

':strategy_name will load the given strategy '

'from the set of built-in strategies'))

# Observers

group = parser.add_argument_group(title='Observers and statistics')

group.add_argument('--nostdstats', action='store_true',

help='Disable the standard statistics observers')

group.add_argument('--observer', '-ob', dest='observers',

action='append', required=False,

help=('This option can be specified multiple times\n'

'\n'

'Module and observer to load with format '

'module_path:observer_name.\n'

'\n'

'module_path:observer_name will load '

'observer_name from the given module_path\n'

'\n'

'module_path will load the module and return '

'all available observers in the module\n'

'\n'

':observer_name will load the given strategy '

'from the set of built-in strategies'))

# Anaylzers

group = parser.add_argument_group(title='Analyzers')

group.add_argument('--analyzer', '-an', dest='analyzers',

action='append', required=False,

help=('This option can be specified multiple times\n'

'\n'

'Module and analyzer to load with format '

'module_path:analzyer_name.\n'

'\n'

'module_path:analyzer_name will load '

'observer_name from the given module_path\n'

'\n'

'module_path will load the module and return '

'all available analyzers in the module\n'

'\n'

':anaylzer_name will load the given strategy '

'from the set of built-in strategies'))

# Broker/Commissions

group = parser.add_argument_group(title='Cash and Commission Scheme Args')

group.add_argument('--cash', '-cash', required=False, type=float,

help='Cash to set to the broker')

group.add_argument('--commission', '-comm', required=False, type=float,

help='Commission value to set')

group.add_argument('--margin', '-marg', required=False, type=float,

help='Margin type to set')

group.add_argument('--mult', '-mul', required=False, type=float,

help='Multiplier to use')

# Plot options

group = parser.add_argument_group(title='Plotting options')

group.add_argument('--noplot', '-np', action='store_true', required=False,

help='Do not plot the read data')

group.add_argument('--plotstyle', '-ps', required=False, default='bar',

choices=['bar', 'line', 'candle'],

help='Plot style for the input data')

group.add_argument('--plotfigs', '-pn', required=False, default=1,

type=int, help='Plot using n figures')

# Extra arguments

parser.add_argument('args', nargs=argparse.REMAINDER,

help='args to pass to the loaded strategy')

return parser.parse_args()

if __name__ == '__main__':

runstrat()