Evaluating external historical performance

With release 1.9.55.122, backtrader can now be used to evaluate the

performance of an external set of orders. This can be used for example:

-

To evaluate a set of orders/trades which for which judgmental trading (i.e.: human discretional decision) was used

-

To evaluate orders created in another platform and verify the analyzers of that platform

-

And obviously in the other direction to evaluate the things returned by backtrader against well-known results from other platforms

Usage pattern

...

cerebro.adddata(mydata)

...

cerebro.add_order_history(orders, notify=True or False)

...

cerebro.run()

The obvious question here is how orders has to look like. Let’s quote the

docs:

-

orders: is an iterable (ex: list, tuple, iterator, generator) in which each element will be also an iterable (with length) with the following sub-elements (2 formats are possible)[datetime, size, price]or[datetime, size, price, data]Note: it must be sorted (or produce sorted elements) by

datetime ascendingwhere:

-

datetimeis a pythondate/datetimeinstance or a string with format YYYY-MM-DD[THH:MM:SS[.us]] where the elements in brackets are optional -

sizeis an integer (positive to buy, negative to sell) -

priceis a float/integer -

dataif present can take any of the following values-

None - The 1st data feed will be used as target

-

integer - The data with that index (insertion order in Cerebro) will be used

-

string - a data with that name, assigned for example with

cerebro.addata(data, name=value), will be the target

-

-

In the case of notify:

-

notify(default: True)If

Truethe 1st strategy inserted in the system will be notified of the artificial orders created following the information from each order inorders

Note

Notice how the example above is adding a data feed. Yes this is needed.

A practical example of how orders could look like

ORDER_HISTORY = (

('2005-02-01', 1, 2984.63),

('2005-03-04', -1, 3079.93),

...

('2006-12-18', 1, 4140.99),

)

An iterable with 3 elements, which could have been perfectly loaded from a CSV file.

An example

The sample below does two things:

-

Execute a simple SMA Crossover strategy

-

Add a history of orders which executes the same operations as the SMA CrossOver strategy

In this 2nd case an empty strategy is added to receive order and trade notifications over

notify_orderandnotify_trade

In both cases a set of analyzers (TimeReturn in Months and Years and

a TradeAnalyzer) are loaded … and they should return the same values.

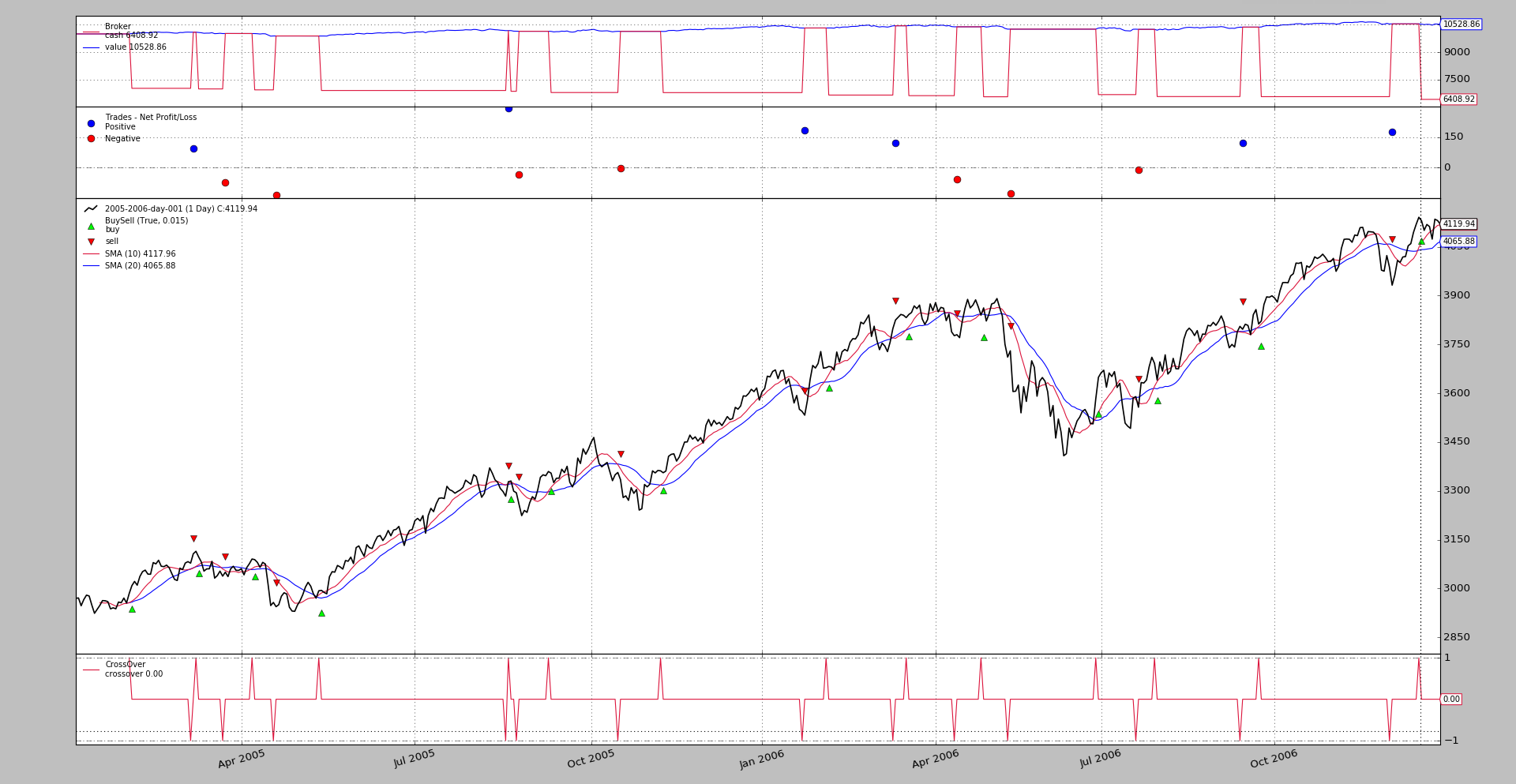

Run 1: SMA Crossover

$ ./order-history.py --plot --cerebro writer=True

Which produces a chart

And some textual output (capped for brevity):

Creating Signal Strategy

2005-02-01,1,2984.63

2005-03-04,-1,3079.93

...

2006-12-01,-1,3993.03

profit 177.9000000000001

2006-12-18,1,4140.99

===============================================================================

Cerebro:

...

- timereturn1:

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

- Params:

- timeframe: 8

- compression: None

- _doprenext: True

- data: None

- firstopen: True

- fund: None

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

- Analysis:

- 2005-12-31: 0.03580099999999975

- 2006-12-31: 0.01649448108275653

.......................................................................

- tradeanalyzer:

- Params: None

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

- Analysis:

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""

- total:

- total: 14

- open: 1

- closed: 13

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""

- streak:

^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^

- won:

- current: 2

- longest: 2

...

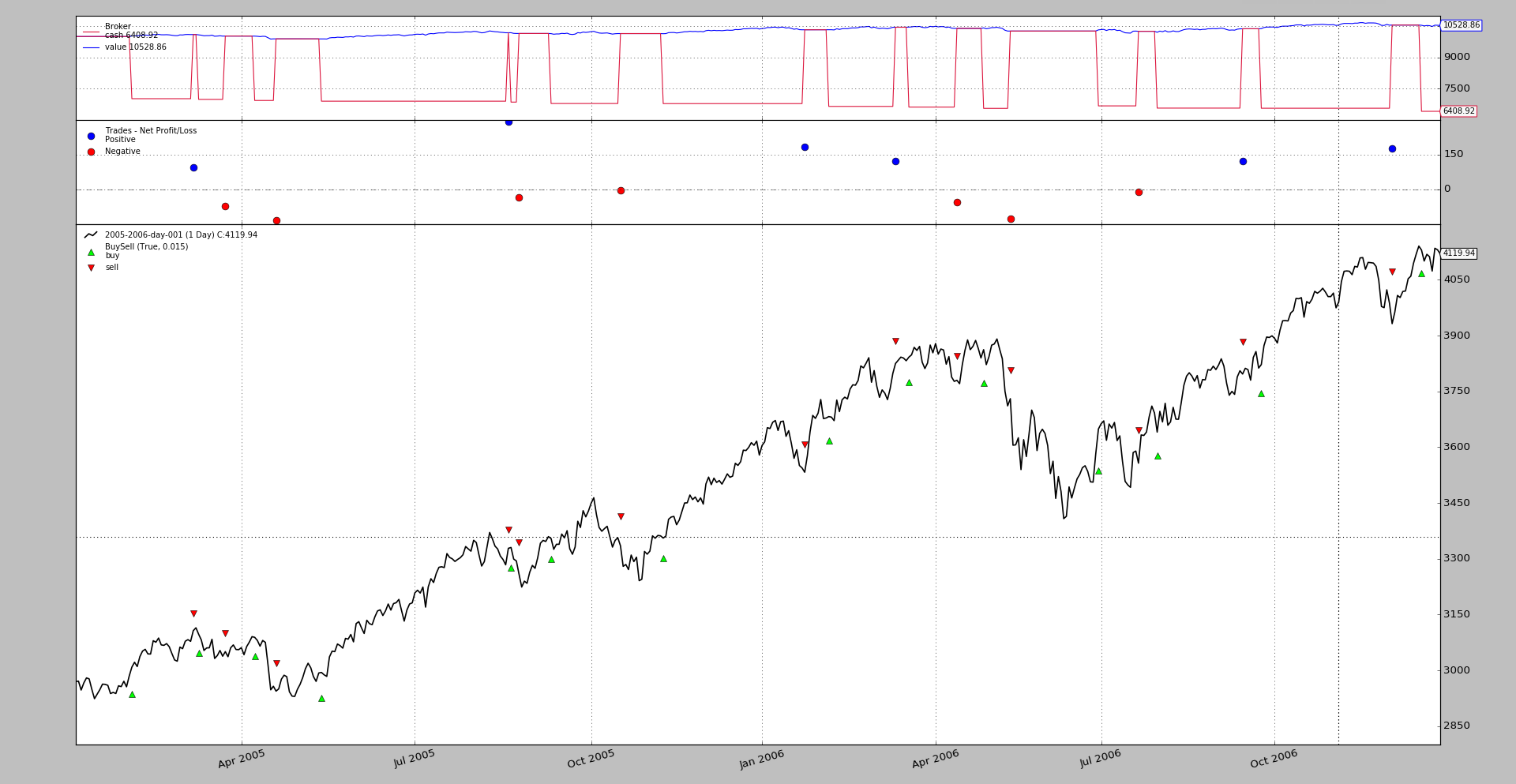

Run 2: Order history

$ ./order-history.py --plot --cerebro writer=True --order-history

Which produces a chart which seems to have no differences

And some textual output (capped again for brevity):

Creating Empty Strategy

2005-02-01,1,2984.63

2005-03-04,-1,3079.93

...

.......................................................................

- timereturn1:

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

- Params:

- timeframe: 8

- compression: None

- _doprenext: True

- data: None

- firstopen: True

- fund: None

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

- Analysis:

- 2005-12-31: 0.03580099999999975

- 2006-12-31: 0.01649448108275653

.......................................................................

- tradeanalyzer:

- Params: None

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

- Analysis:

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""

- total:

- total: 14

- open: 1

- closed: 13

"""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""""

- streak:

^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^

- won:

- current: 2

- longest: 2

...

And the values as expected match those of the reference.

Conclusion

Measuring the performance of judgmental trading can be measured for example. This is sometimes used in combination with algotrading, where the algo generates signals, but the human has the final decision on whether the signal has to translate into an actual trade.

Sample Usage

$ ./order-history.py --help

usage: order-history.py [-h] [--data0 DATA0] [--fromdate FROMDATE]

[--todate TODATE] [--order-history] [--cerebro kwargs]

[--broker kwargs] [--sizer kwargs] [--strat kwargs]

[--plot [kwargs]]

Order History Sample

optional arguments:

-h, --help show this help message and exit

--data0 DATA0 Data to read in (default:

../../datas/2005-2006-day-001.txt)

--fromdate FROMDATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default: )

--todate TODATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default: )

--order-history use order history (default: False)

--cerebro kwargs kwargs in key=value format (default: )

--broker kwargs kwargs in key=value format (default: )

--sizer kwargs kwargs in key=value format (default: )

--strat kwargs kwargs in key=value format (default: )

--plot [kwargs] kwargs in key=value format (default: )

Sample Code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import backtrader as bt

ORDER_HISTORY = (

('2005-02-01', 1, 2984.63),

('2005-03-04', -1, 3079.93),

('2005-03-08', 1, 3113.82),

('2005-03-22', -1, 3040.55),

('2005-04-08', 1, 3092.07),

('2005-04-20', -1, 2957.92),

('2005-05-13', 1, 2991.71),

('2005-08-19', -1, 3284.35),

('2005-08-22', 1, 3328.84),

('2005-08-25', -1, 3293.69),

('2005-09-12', 1, 3361.1),

('2005-10-18', -1, 3356.73),

('2005-11-09', 1, 3361.92),

('2006-01-24', -1, 3544.78),

('2006-02-06', 1, 3678.87),

('2006-03-13', -1, 3801.03),

('2006-03-20', 1, 3833.25),

('2006-04-13', -1, 3777.24),

('2006-05-02', 1, 3839.24),

('2006-05-16', -1, 3711.46),

('2006-06-30', 1, 3592.01),

('2006-07-21', -1, 3580.53),

('2006-08-01', 1, 3687.82),

('2006-09-14', -1, 3809.08),

('2006-09-25', 1, 3815.13),

('2006-12-01', -1, 3993.03),

('2006-12-18', 1, 4140.99),

)

class SmaCross(bt.SignalStrategy):

params = dict(sma1=10, sma2=20)

def notify_order(self, order):

if not order.alive():

print(','.join(str(x) for x in

(self.data.num2date(order.executed.dt).date(),

order.executed.size * 1 if order.isbuy() else -1,

order.executed.price)))

def notify_trade(self, trade):

if trade.isclosed:

print('profit {}'.format(trade.pnlcomm))

def __init__(self):

print('Creating Signal Strategy')

sma1 = bt.ind.SMA(period=self.params.sma1)

sma2 = bt.ind.SMA(period=self.params.sma2)

crossover = bt.ind.CrossOver(sma1, sma2)

self.signal_add(bt.SIGNAL_LONG, crossover)

class St(bt.Strategy):

params = dict(

)

def notify_order(self, order):

if not order.alive():

print(','.join(str(x) for x in

(self.data.num2date(order.executed.dt).date(),

order.executed.size * 1 if order.isbuy() else -1,

order.executed.price)))

def notify_trade(self, trade):

if trade.isclosed:

print('profit {}'.format(trade.pnlcomm))

def __init__(self):

print('Creating Empty Strategy')

pass

def next(self):

pass

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

# Data feed kwargs

kwargs = dict()

# Parse from/to-date

dtfmt, tmfmt = '%Y-%m-%d', 'T%H:%M:%S'

for a, d in ((getattr(args, x), x) for x in ['fromdate', 'todate']):

if a:

strpfmt = dtfmt + tmfmt * ('T' in a)

kwargs[d] = datetime.datetime.strptime(a, strpfmt)

data0 = bt.feeds.BacktraderCSVData(dataname=args.data0, **kwargs)

cerebro.adddata(data0)

# Broker

cerebro.broker = bt.brokers.BackBroker(**eval('dict(' + args.broker + ')'))

# Sizer

cerebro.addsizer(bt.sizers.FixedSize, **eval('dict(' + args.sizer + ')'))

# Strategy

if not args.order_history:

cerebro.addstrategy(SmaCross, **eval('dict(' + args.strat + ')'))

else:

cerebro.addstrategy(St, **eval('dict(' + args.strat + ')'))

cerebro.add_order_history(ORDER_HISTORY, notify=True)

cerebro.addanalyzer(bt.analyzers.TimeReturn, timeframe=bt.TimeFrame.Months)

cerebro.addanalyzer(bt.analyzers.TimeReturn, timeframe=bt.TimeFrame.Years)

cerebro.addanalyzer(bt.analyzers.TradeAnalyzer)

# Execute

cerebro.run(**eval('dict(' + args.cerebro + ')'))

if args.plot: # Plot if requested to

cerebro.plot(**eval('dict(' + args.plot + ')'))

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description=(

'Order History Sample'

)

)

parser.add_argument('--data0', default='../../datas/2005-2006-day-001.txt',

required=False, help='Data to read in')

# Defaults for dates

parser.add_argument('--fromdate', required=False, default='',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--todate', required=False, default='',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--order-history', required=False, action='store_true',

help='use order history')

parser.add_argument('--cerebro', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--broker', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--sizer', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--strat', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--plot', required=False, default='',

nargs='?', const='{}',

metavar='kwargs', help='kwargs in key=value format')

return parser.parse_args(pargs)

if __name__ == '__main__':

runstrat()