Cheat On Open

Release 1.9.44.116 adds support for Cheat-On-Open. This seems to be a

demanded feature for people who go all-in, having made a calculation after

the close of a bar, but expecting to be matched against the open price.

Such a use case fails when the opening price gaps (up or down, depending on

whether buy or sell is in effect) and the cash is not enough for an

all-in operation. This forces the broker to reject the operation.

And although people can try to look into the future with a positive [1]

index approach, this requires preloading data which is not always available.

The pattern:

cerebro = bt.Cerebro(cheat_on_open=True)

This:

-

Activates an extra cycle in the system which calls the methods in the strategy

next_open,nextstart_openandprenext_openThe decision to have an additional family of methods has been made to make a clear separation between the regular methods which operate on the basis that the prices being examined are no longer available and the future is unknown and the operation in cheating mode.

This also avoids having 2 calls to the regular

nextmethod.

The following holds true when inside a xxx_open method:

-

The indicators have not been recalculated and hold the values that were last seen during the previous cycle in the equivalent

xxxregular methods -

The broker has not yet evaluated the pending orders for the new cycle and new orders can be introduced which will be evaluated if possible.

Notice that:

-

Cerebroalso has abroker_coo(default:True) parameter which tells cerebro that ifcheat-on-openhas been activated, it shall try to activate it also in the broker if possible.The simulation broker has a parameter named:

cooand a method to set it namedset_coo

Trying cheat-on-open

The sample below has a strategy with 2 different behaviors:

-

If cheat-on-open is True, it will only operate from

next_open -

If cheat-on-open is False, it will only operate from

next

In both cases the matching price must be the same

-

If not cheating, the order is issued at the end of the previous day and will be matched with the next incoming price which is the

openprice -

If cheating, the order is issued on the same day it is executed. Because the order is issued before the broker has evaluated orders, it will also be matched with the next incoming price, the

openprice.This second scenario, allows calculation of exact stakes for all-in strategies, because one can directly access the current

openprice.

In both cases

- The current

openandcloseprices will be printed fromnext.

Regular execution:

$ ./cheat-on-open.py --cerebro cheat_on_open=False

...

2005-04-07 next, open 3073.4 close 3090.72

2005-04-08 next, open 3092.07 close 3088.92

Strat Len 68 2005-04-08 Send Buy, fromopen False, close 3088.92

2005-04-11 Buy Executed at price 3088.47

2005-04-11 next, open 3088.47 close 3080.6

2005-04-12 next, open 3080.42 close 3065.18

...

The order:

-

Is issued on 2005-04-08 after the close

-

It is executed on 2005-04-11 with the

openprice of3088.47

Cheating execution:

$ ./cheat-on-open.py --cerebro cheat_on_open=True

...

2005-04-07 next, open 3073.4 close 3090.72

2005-04-08 next, open 3092.07 close 3088.92

2005-04-11 Send Buy, fromopen True, close 3080.6

2005-04-11 Buy Executed at price 3088.47

2005-04-11 next, open 3088.47 close 3080.6

2005-04-12 next, open 3080.42 close 3065.18

...

The order:

-

Is issued on 2005-04-11 before the open

-

It is executed on 2005-04-11 with the

openprice of3088.47

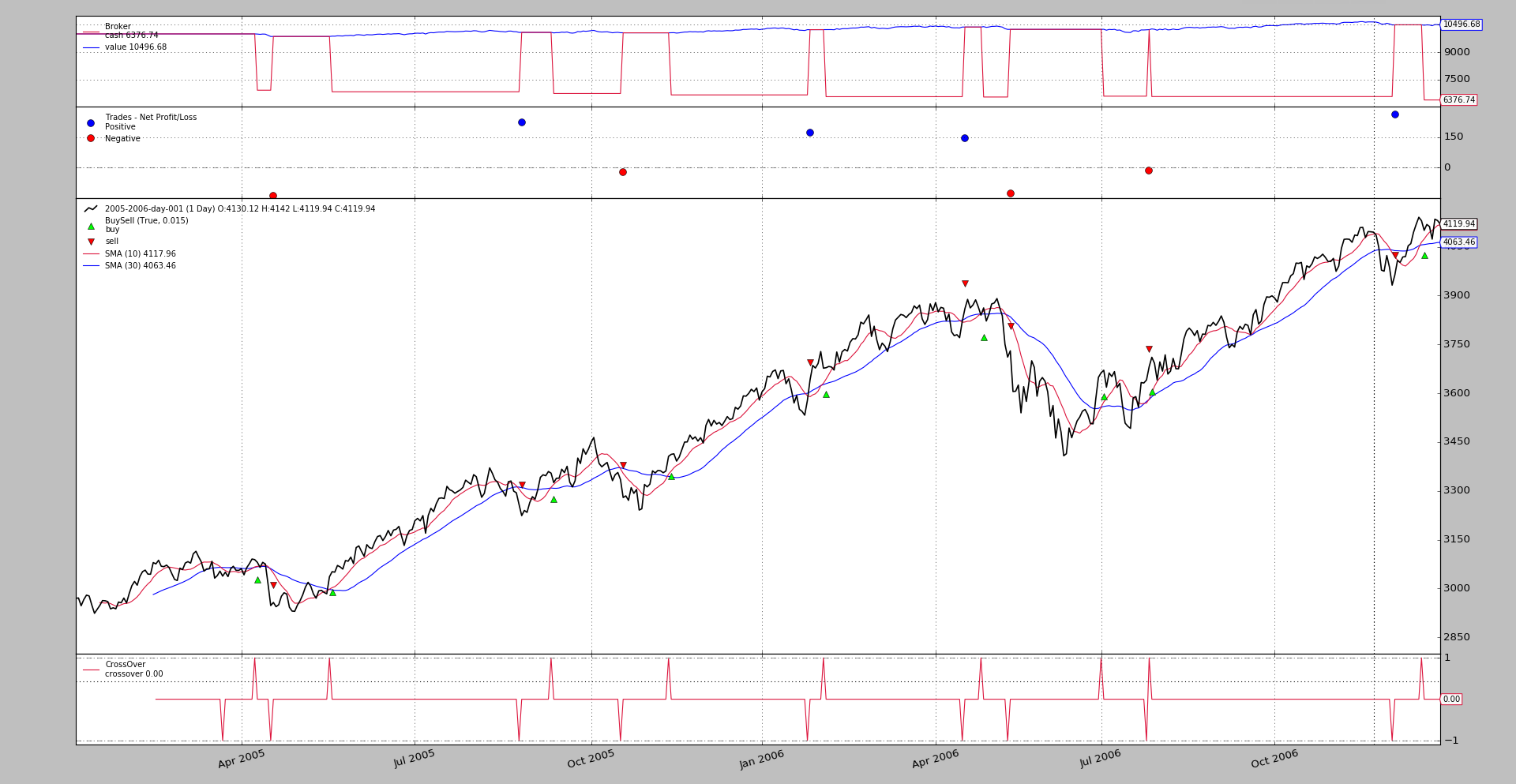

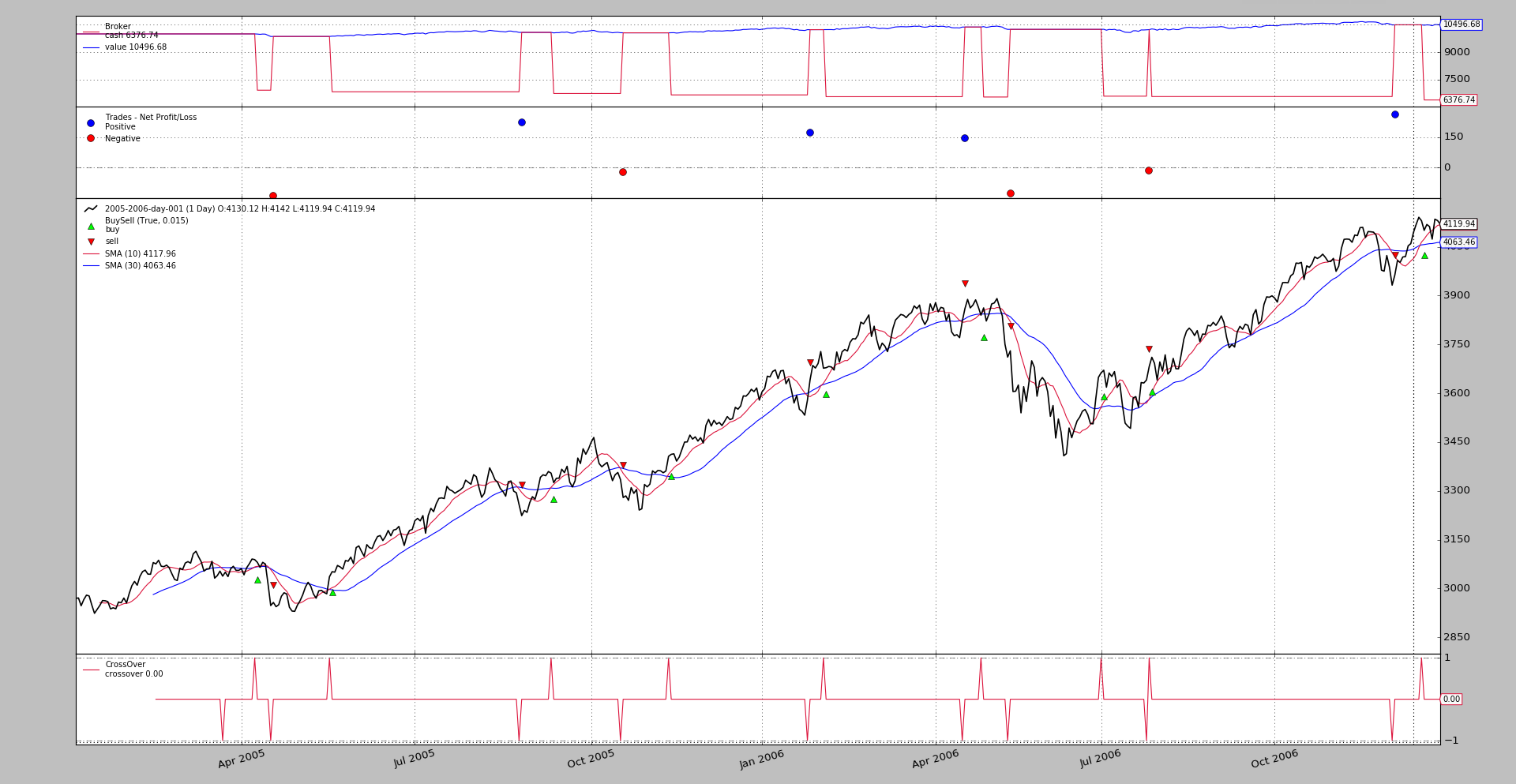

And the overall result as seen on the chart is also the same.

Conclusion

Cheating on the open allows issuing orders before the open which can for example allow the exact calculation of stakes for all-in scenarios.

Sample usage

$ ./cheat-on-open.py --help

usage: cheat-on-open.py [-h] [--data0 DATA0] [--fromdate FROMDATE]

[--todate TODATE] [--cerebro kwargs] [--broker kwargs]

[--sizer kwargs] [--strat kwargs] [--plot [kwargs]]

Cheat-On-Open Sample

optional arguments:

-h, --help show this help message and exit

--data0 DATA0 Data to read in (default:

../../datas/2005-2006-day-001.txt)

--fromdate FROMDATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default: )

--todate TODATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default: )

--cerebro kwargs kwargs in key=value format (default: )

--broker kwargs kwargs in key=value format (default: )

--sizer kwargs kwargs in key=value format (default: )

--strat kwargs kwargs in key=value format (default: )

--plot [kwargs] kwargs in key=value format (default: )

Sample source

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import backtrader as bt

class St(bt.Strategy):

params = dict(

periods=[10, 30],

matype=bt.ind.SMA,

)

def __init__(self):

self.cheating = self.cerebro.p.cheat_on_open

mas = [self.p.matype(period=x) for x in self.p.periods]

self.signal = bt.ind.CrossOver(*mas)

self.order = None

def notify_order(self, order):

if order.status != order.Completed:

return

self.order = None

print('{} {} Executed at price {}'.format(

bt.num2date(order.executed.dt).date(),

'Buy' * order.isbuy() or 'Sell', order.executed.price)

)

def operate(self, fromopen):

if self.order is not None:

return

if self.position:

if self.signal < 0:

self.order = self.close()

elif self.signal > 0:

print('{} Send Buy, fromopen {}, close {}'.format(

self.data.datetime.date(),

fromopen, self.data.close[0])

)

self.order = self.buy()

def next(self):

print('{} next, open {} close {}'.format(

self.data.datetime.date(),

self.data.open[0], self.data.close[0])

)

if self.cheating:

return

self.operate(fromopen=False)

def next_open(self):

if not self.cheating:

return

self.operate(fromopen=True)

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

# Data feed kwargs

kwargs = dict()

# Parse from/to-date

dtfmt, tmfmt = '%Y-%m-%d', 'T%H:%M:%S'

for a, d in ((getattr(args, x), x) for x in ['fromdate', 'todate']):

if a:

strpfmt = dtfmt + tmfmt * ('T' in a)

kwargs[d] = datetime.datetime.strptime(a, strpfmt)

# Data feed

data0 = bt.feeds.BacktraderCSVData(dataname=args.data0, **kwargs)

cerebro.adddata(data0)

# Broker

cerebro.broker = bt.brokers.BackBroker(**eval('dict(' + args.broker + ')'))

# Sizer

cerebro.addsizer(bt.sizers.FixedSize, **eval('dict(' + args.sizer + ')'))

# Strategy

cerebro.addstrategy(St, **eval('dict(' + args.strat + ')'))

# Execute

cerebro.run(**eval('dict(' + args.cerebro + ')'))

if args.plot: # Plot if requested to

cerebro.plot(**eval('dict(' + args.plot + ')'))

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description=(

'Cheat-On-Open Sample'

)

)

parser.add_argument('--data0', default='../../datas/2005-2006-day-001.txt',

required=False, help='Data to read in')

# Defaults for dates

parser.add_argument('--fromdate', required=False, default='',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--todate', required=False, default='',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--cerebro', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--broker', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--sizer', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--strat', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--plot', required=False, default='',

nargs='?', const='{}',

metavar='kwargs', help='kwargs in key=value format')

return parser.parse_args(pargs)

if __name__ == '__main__':

runstrat()