Mixing Timeframes in Indicators

Release 1.3.0.92 brings up the possibility to have data (from either data feeds and/or indicators) from different timeframes mixed.

To the release: https://github.com/mementum/backtrader/releases/tag/1.3.0.92

Background: Indicators are smart dumb objects.

-

They are smart because they can make complex calculations.

-

They are dumb because they operate with no knowledge of what sources are providing the data for the calculations

As such:

- If the data sources providing the values have different timeframes,

different lengths inside the

Cerebroengine, the indicator will break.

Example of a calculation, in which data0 has a timeframe of days and

data1 has a timeframe of months:

pivotpoint = btind.PivotPoint(self.data1)

sellsignal = self.data0.close < pivotpoint.s1

Here a sell signal is sought when the close is below the s1 line (1st

support)

Note

PivotPoint works in a larger timeframe by definition

This will in the past with the following error:

return self.array[self.idx + ago]

IndexError: array index out of range

And for a good reason: self.data.close provides values from the very 1st

instant, but PivotPoint (and hence the s1 line) will only deliver

values once a full month has gone by, which is roughly equivalent to 22

values of self.data0.close. During this 22 closes there isn’t yet a value

for s1 and the attempt to fetch it from the underlying array fails.

Lines objects support the () operator (__call__ special method in

Python) for deliver a delayed version of itself:

close1 = self.data.close(-1)

In this example the object close1 (when accessed via [0]) contains

always the previous values (-1) delivered by close. The syntax has been

reused to accomodate adapting timeframes. Let’s rewrite the above

pivotpoint snippet:

pivotpoint = btind.PivotPoint(self.data1)

sellsignal = self.data0.close < pivotpoint.s1()

See how the () is executed with no arguments (in the background a None

is being supplied). The following is happening:

pivotpoint.s1() is returning an internal LinesCoupler object which

follows the rigthm of the larger scope. This coupler fills itself with the

latest delivered value from the real s1 (starting with a default value of

NaN)

But something extra is needed to make the magic work. Cerebro has to be

created with:

cerebro = bt.Cerebro(runonce=False)

or executed with:

cerebro.run(runonce=False)

In this mode the indicators and late-evaluated automatic lines objects are executed step by step rather than in tight loops. This makes the entire operation slower, but it makes it possible

The sample script at the bottom which was breaking above, now runs:

$ ./mixing-timeframes.py

With output:

0021,0021,0001,2005-01-31,2984.75,2935.96,0.00

0022,0022,0001,2005-02-01,3008.85,2935.96,0.00

...

0073,0073,0003,2005-04-15,3013.89,3010.76,0.00

0074,0074,0003,2005-04-18,2947.79,3010.76,1.00

...

At trading 74 the 1st instance of close < s1 takes palce.

The script also provides insight into the additional possiblity: couple all lines of an indicator. Before we had:

self.sellsignal = self.data0.close < pp.s1()

Being the alternative:

pp1 = pp()

self.sellsignal = self.data0.close < pp1.s1

Now the entire PivotPoint indicator has been coupled and any of its lines

can be accessed (namely p, r1, r2, s1, s2). The script has

only interest in s1 and the access is direct.:

$ ./mixing-timeframes.py --multi

The output:

0021,0021,0001,2005-01-31,2984.75,2935.96,0.00

0022,0022,0001,2005-02-01,3008.85,2935.96,0.00

...

0073,0073,0003,2005-04-15,3013.89,3010.76,0.00

0074,0074,0003,2005-04-18,2947.79,3010.76,1.00

...

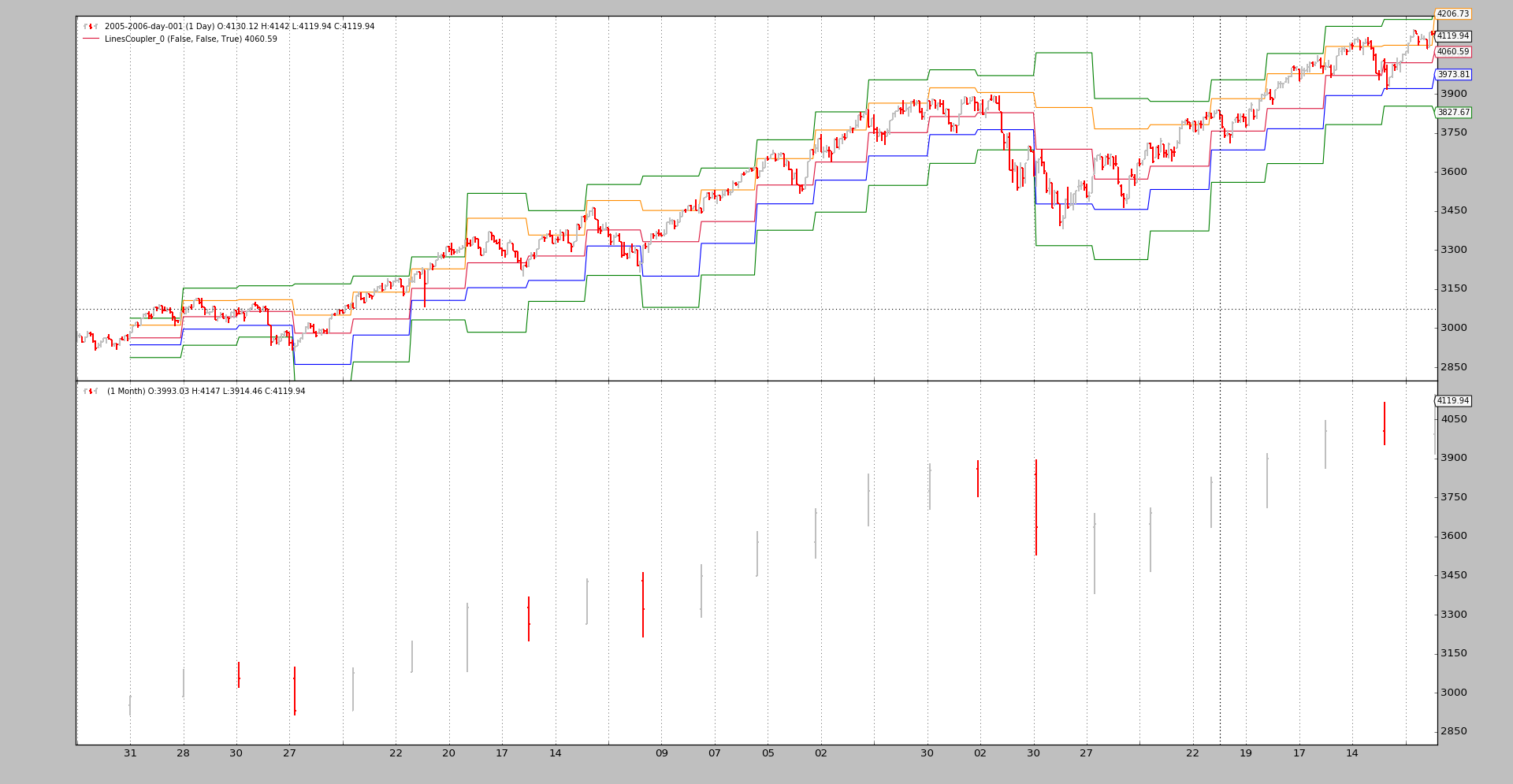

No surprises here. The same as before. The “coupled” object can even be plotted:

$ ./mixing-timeframes.py --multi --plot

Full coupling syntax

For lines objects with multiple lines (for example Indicators like

PivotPoint):

-

obj(clockref=None, line=-1)clockrefIfclockrefisNone, the surrounding object (in the examples aStrategy) will be the reference to adapt larger timeframes (for example:Months) to smaller/faster timeframes (for example:Days)

Another reference can be used if wished

line- If the default `-1` is given, all *lines* are coupled. - If another integer (for example, `0` or `1`) a single line will be coupled and fetched by index (from `obj.lines[x]`) - If a string is passed, the line will be fetched by name. In the sample the following could have been done: ``` coupled_s1 = pp(line='s1') ```

For lines objects with a single line (for example line s1 from the

indicator PivotPoint):

obj(clockref=None)(see above forclockref)

Conclusion

Integrated in the regular () syntax, datas from different timeframes can be

mixed in indicators, taking always into account that cerebro needs to be

instantiated or created with runonce=False.

Script Code and Usage

Available as sample in the sources of backtrader. Usage:

$ ./mixing-timeframes.py --help

usage: mixing-timeframes.py [-h] [--data DATA] [--multi] [--plot]

Sample for pivot point and cross plotting

optional arguments:

-h, --help show this help message and exit

--data DATA Data to be read in (default: ../../datas/2005-2006-day-001.txt)

--multi Couple all lines of the indicator (default: False)

--plot Plot the result (default: False)

The code:

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

import backtrader.utils.flushfile

class St(bt.Strategy):

params = dict(multi=True)

def __init__(self):

self.pp = pp = btind.PivotPoint(self.data1)

pp.plotinfo.plot = False # deactivate plotting

if self.p.multi:

pp1 = pp() # couple the entire indicators

self.sellsignal = self.data0.close < pp1.s1

else:

self.sellsignal = self.data0.close < pp.s1()

def next(self):

txt = ','.join(

['%04d' % len(self),

'%04d' % len(self.data0),

'%04d' % len(self.data1),

self.data.datetime.date(0).isoformat(),

'%.2f' % self.data0.close[0],

'%.2f' % self.pp.s1[0],

'%.2f' % self.sellsignal[0]])

print(txt)

def runstrat():

args = parse_args()

cerebro = bt.Cerebro()

data = btfeeds.BacktraderCSVData(dataname=args.data)

cerebro.adddata(data)

cerebro.resampledata(data, timeframe=bt.TimeFrame.Months)

cerebro.addstrategy(St, multi=args.multi)

cerebro.run(stdstats=False, runonce=False)

if args.plot:

cerebro.plot(style='bar')

def parse_args():

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description='Sample for pivot point and cross plotting')

parser.add_argument('--data', required=False,

default='../../datas/2005-2006-day-001.txt',

help='Data to be read in')

parser.add_argument('--multi', required=False, action='store_true',

help='Couple all lines of the indicator')

parser.add_argument('--plot', required=False, action='store_true',

help=('Plot the result'))

return parser.parse_args()

if __name__ == '__main__':

runstrat()