Volume Filling

Up until now the default volume filling strategy in backtrader has been rather simple and straightforward:

- Ignore volume

Note

Jul 15, 2016

Corrected a bug in the implementation and updated the sample to

close the position and repeat after a break.

The last test run below (and the corresponding chart) are from the update sample

This is based on 2 premises:

-

Trade in markets liquid enough to fully absorb buy/sell orders in one go

-

Real volume matching requires a real wolrd

A quick example is a

Fill or Killorder. Even down to the tick resolution and with enough volume for a fill, the backtrader broker cannot know how many extra actors happen to be in the market to discriminate if such an order would be or would not be matched to stick to theFillpart or if the order should beKill

But with release 1.5.2.93 it is possible to specify a filler for the

broker to take Volume into account when executing an order. Additionally 3

initial fillers have made it into the release:

-

FixedSize: uses a fixed matching size (for example: 1000 units) each day, provided the current bar has at least 1000 units -

FixedBarPerc: uses a percentage of the total bar volume to try to match the order -

BarPointPerc: does a uniform distribution of the bar volume across the price range high-low and uses a percentage of the volume that would correspond to a single price point

Creating a filler

A filler in the backtrader ecosystem can be any callable which matches the following signature:

callable(order, price, ago)

Where:

-

orderis the order which is going to be executedThis object gives access to the

dataobject which is the target of the operation, creation sizes/prices, execution prices/sizes/remaining sizes and other details -

priceat which the order is going to be executed -

agois the index to thedatain the order in which to look for the volume and price elementsIn almost all cases this will be

0(current point in time) but in a corner case to coverCloseorders this may be-1To for example access the bar volume do:

barvolume = order.data.volume[ago]

The callable can be a function or for example an instance of a class

supporting the __call__ method, like in:

class MyFiller(object):

def __call__(self, order, price, ago):

pass

Adding a Filler to the broker

The most straightforward method is to use the set_filler:

import backtrader as bt

cerebro = Cerebro()

cerebro.broker.set_filler(bt.broker.filler.FixedSize())

The second choice is to completely replace the broker, although this is

probably only meant for subclasses of BrokerBack which have rewritten

portions of the functionality:

import backtrader as bt

cerebro = Cerebro()

filler = bt.broker.filler.FixedSize()

newbroker = bt.broker.BrokerBack(filler=filler)

cerebro.broker = newbroker

The sample

The backtrader sources contain a sample named volumefilling which allows

to test some of the integrated fillers (initially all)

The sample uses a default data sample in the sources named:

datas/2006-volume-day-001.txt.

For example a run with no filler:

$ ./volumefilling.py --stakeperc 20.0

Output:

Len,Datetime,Open,High,Low,Close,Volume,OpenInterest

0001,2006-01-02,3602.00,3624.00,3596.00,3617.00,164794.00,1511674.00

++ STAKE VOLUME: 32958.0

-- NOTIFY ORDER BEGIN

Ref: 1

...

Alive: False

-- NOTIFY ORDER END

-- ORDER REMSIZE: 0.0

++ ORDER COMPLETED at data.len: 2

0002,2006-01-03,3623.00,3665.00,3614.00,3665.00,554426.00,1501792.00

...

Much of the input has been skipped because it is rather verbose, but the summary is:

-

Upon seeing the 1st bar

20%(–stakeperc 20.0) will be used to issue a buy order -

As seen in the output and with the default behaviour of backtrader the order has been completely matched in a single shot. No look at the volume has been performed

Note

The broker has an insane amount of cash allocated in the sample to make sure it can withstand many test situations

Another run with the FixedSize volume filler and a maximum of 1000

units per bar:

$ ./volumefilling.py --stakeperc 20.0 --filler FixedSize --filler-args size=1000

Ouutput:

Len,Datetime,Open,High,Low,Close,Volume,OpenInterest

0001,2006-01-02,3602.00,3624.00,3596.00,3617.00,164794.00,1511674.00

++ STAKE VOLUME: 32958.0

-- NOTIFY ORDER BEGIN

...

-- NOTIFY ORDER END

-- ORDER REMSIZE: 0.0

++ ORDER COMPLETED at data.len: 34

0034,2006-02-16,3755.00,3774.00,3738.00,3773.00,502043.00,1662302.00

...

Now:

-

The chosen volume remains the same at

32958 -

Execution is completed at bar

34which seems reasonable because from bar 2 to 34 … 33 bars have been seen. With\1000` units matched per bar 33 bars are obviously needed to complete the execution

This is not a great achievement, so let’s go for FixedBarPerc:

$ ./volumefilling.py --stakeperc 20.0 --filler FixedBarPerc --filler-args perc=0.75

Output:

...

-- NOTIFY ORDER END

-- ORDER REMSIZE: 0.0

++ ORDER COMPLETED at data.len: 11

0011,2006-01-16,3635.00,3664.00,3632.00,3660.00,273296.00,1592611.00

...

This time:

-

Skipping the start, still

32958units for the order -

The execution uses 0.75% of the bar volume to match the request.

-

It takes from bar 2 to 11 (10 bars) to complete.

This is more interesting, but let’s see what happens now with a more dynamic

volume allocation with BarPointPerc:

$ ./volumefilling.py --stakeperc 20.0 --filler BarPointPerc --filler-args minmov=1.0,perc=10.0

Output:

...

-- NOTIFY ORDER END

-- ORDER REMSIZE: 0.0

++ ORDER COMPLETED at data.len: 22

0022,2006-01-31,3697.00,3718.00,3681.00,3704.00,749740.00,1642003.00

...

What happens is:

-

Same initial allocation (skipped) to the order of

32958as size -

It takes from 2 to 22 to fully execute (21 bars)

-

The filler has used a

minmovof1.0(minimum price movement of the asset) to uniformly distribute the volume amongst the high-low range -

A

10%of the volumed assigned to a given price point is used for order matching

For anyone interested in how the order is being matched partially at each bar, examining the full output of a run may be worth the time.

Note

Run with corrected bug in 1.5.3.93 and updated sample to close

the operation after a break

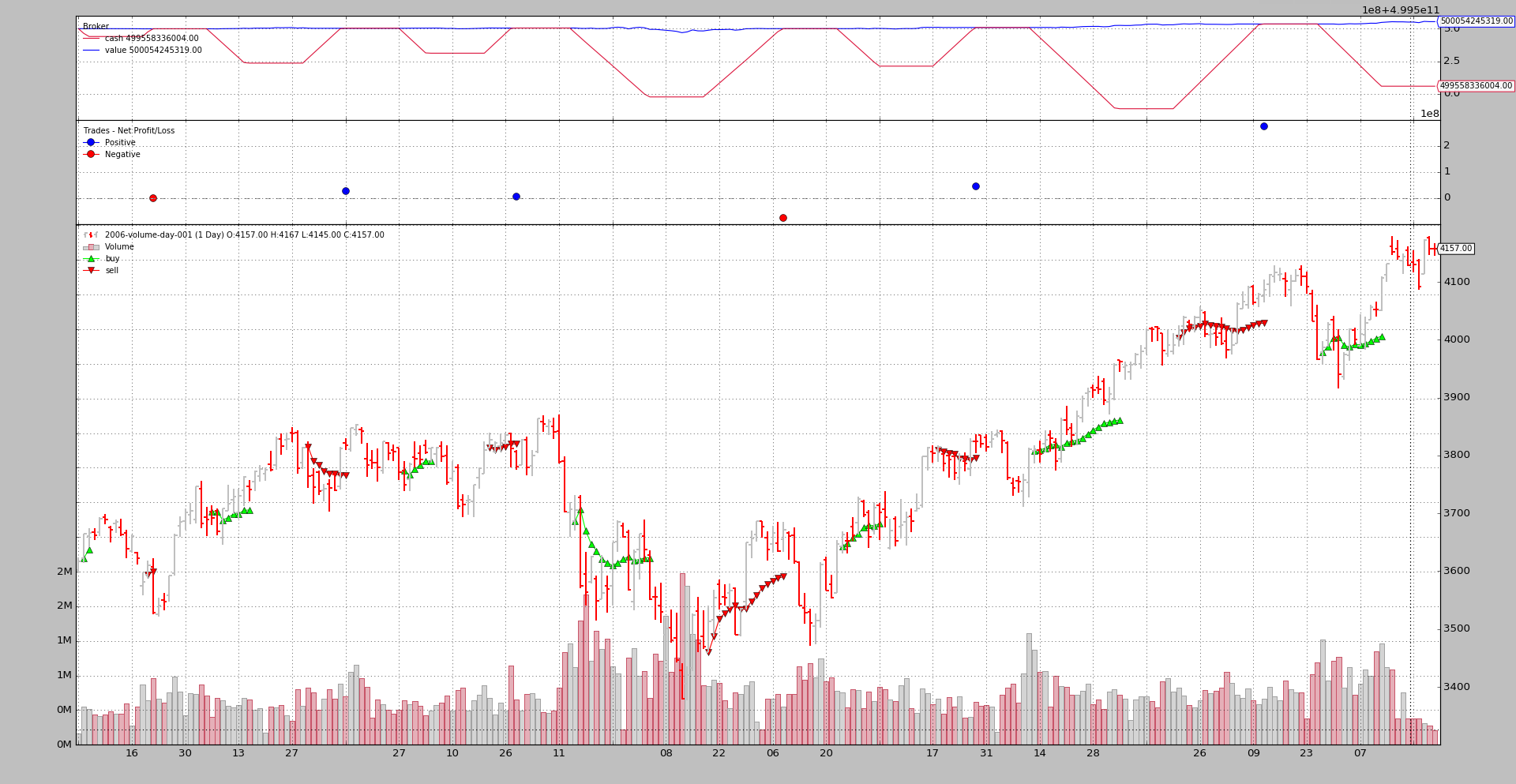

The cash is increased to an even insaner amount to avoid margin calls and plotting is enabled:

$ ./volumefilling.py --filler FixedSize --filler-args size=10000 --stakeperc 10.0 --plot --cash 500e9

Rather than looking at the output which is extremely verbose, let’s look at the chart which already tells the story.

Usage of the sample:

usage: volumefilling.py [-h] [--data DATA] [--cash CASH]

[--filler {FixedSize,FixedBarPerc,BarPointPerc}]

[--filler-args FILLER_ARGS] [--stakeperc STAKEPERC]

[--opbreak OPBREAK] [--fromdate FROMDATE]

[--todate TODATE] [--plot]

Volume Filling Sample

optional arguments:

-h, --help show this help message and exit

--data DATA Data to be read in (default: ../../datas/2006-volume-

day-001.txt)

--cash CASH Starting cash (default: 500000000.0)

--filler {FixedSize,FixedBarPerc,BarPointPerc}

Apply a volume filler for the execution (default:

None)

--filler-args FILLER_ARGS

kwargs for the filler with format:

arg1=val1,arg2=val2... (default: None)

--stakeperc STAKEPERC

Percentage of 1st bar to use for stake (default: 10.0)

--opbreak OPBREAK Bars to wait for new op after completing another

(default: 10)

--fromdate FROMDATE, -f FROMDATE

Starting date in YYYY-MM-DD format (default: None)

--todate TODATE, -t TODATE

Ending date in YYYY-MM-DD format (default: None)

--plot Plot the result (default: False)

The code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import os.path

import time

import sys

import backtrader as bt

class St(bt.Strategy):

params = (

('stakeperc', 10.0),

('opbreak', 10),

)

def notify_order(self, order):

print('-- NOTIFY ORDER BEGIN')

print(order)

print('-- NOTIFY ORDER END')

print('-- ORDER REMSIZE:', order.executed.remsize)

if order.status == order.Completed:

print('++ ORDER COMPLETED at data.len:', len(order.data))

self.doop = -self.p.opbreak

def __init__(self):

pass

def start(self):

self.callcounter = 0

txtfields = list()

txtfields.append('Len')

txtfields.append('Datetime')

txtfields.append('Open')

txtfields.append('High')

txtfields.append('Low')

txtfields.append('Close')

txtfields.append('Volume')

txtfields.append('OpenInterest')

print(','.join(txtfields))

self.doop = 0

def next(self):

txtfields = list()

txtfields.append('%04d' % len(self))

txtfields.append(self.data0.datetime.date(0).isoformat())

txtfields.append('%.2f' % self.data0.open[0])

txtfields.append('%.2f' % self.data0.high[0])

txtfields.append('%.2f' % self.data0.low[0])

txtfields.append('%.2f' % self.data0.close[0])

txtfields.append('%.2f' % self.data0.volume[0])

txtfields.append('%.2f' % self.data0.openinterest[0])

print(','.join(txtfields))

# Single order

if self.doop == 0:

if not self.position.size:

stakevol = (self.data0.volume[0] * self.p.stakeperc) // 100

print('++ STAKE VOLUME:', stakevol)

self.buy(size=stakevol)

else:

self.close()

self.doop += 1

FILLERS = {

'FixedSize': bt.broker.filler.FixedSize,

'FixedBarPerc': bt.broker.filler.FixedBarPerc,

'BarPointPerc': bt.broker.filler.BarPointPerc,

}

def runstrat():

args = parse_args()

datakwargs = dict()

if args.fromdate:

fromdate = datetime.datetime.strptime(args.fromdate, '%Y-%m-%d')

datakwargs['fromdate'] = fromdate

if args.todate:

fromdate = datetime.datetime.strptime(args.todate, '%Y-%m-%d')

datakwargs['todate'] = todate

data = bt.feeds.BacktraderCSVData(dataname=args.data, **datakwargs)

cerebro = bt.Cerebro()

cerebro.adddata(data)

cerebro.broker.set_cash(args.cash)

if args.filler is not None:

fillerkwargs = dict()

if args.filler_args is not None:

fillerkwargs = eval('dict(' + args.filler_args + ')')

filler = FILLERS[args.filler](**fillerkwargs)

cerebro.broker.set_filler(filler)

cerebro.addstrategy(St, stakeperc=args.stakeperc, opbreak=args.opbreak)

cerebro.run()

if args.plot:

cerebro.plot(style='bar')

def parse_args():

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description='Volume Filling Sample')

parser.add_argument('--data', required=False,

default='../../datas/2006-volume-day-001.txt',

help='Data to be read in')

parser.add_argument('--cash', required=False, action='store',

default=500e6, type=float,

help=('Starting cash'))

parser.add_argument('--filler', required=False, action='store',

default=None, choices=FILLERS.keys(),

help=('Apply a volume filler for the execution'))

parser.add_argument('--filler-args', required=False, action='store',

default=None,

help=('kwargs for the filler with format:\n'

'\n'

'arg1=val1,arg2=val2...'))

parser.add_argument('--stakeperc', required=False, action='store',

type=float, default=10.0,

help=('Percentage of 1st bar to use for stake'))

parser.add_argument('--opbreak', required=False, action='store',

type=int, default=10,

help=('Bars to wait for new op after completing '

'another'))

parser.add_argument('--fromdate', '-f', required=False, default=None,

help='Starting date in YYYY-MM-DD format')

parser.add_argument('--todate', '-t', required=False, default=None,

help='Ending date in YYYY-MM-DD format')

parser.add_argument('--plot', required=False, action='store_true',

help=('Plot the result'))

return parser.parse_args()

if __name__ == '__main__':

runstrat()