Futures and Spot Compensation

Release 1.9.32.116 adds support for an interesting use case presented in

the Community

-

Start a trade with a future, which includes physical delivery

-

Have an indicator tell you something

-

If needed be, close the position by operating on the spot price, effectively canceling the physical delivery, be it for receiving the goods or for having to deliver them (and hopefully making a profit)

The future expires on the same day the operation on the spot price takes place

That means:

-

The platform is fed with data points from two different assets

-

The platform has to somehow understand the assets are related and that operations on the spot price will close positions open on the future

In reality, the future is not closed, only the physical delivery is compensated

Using that compensation concept, backtrader adds a way to let the user

communicate to the platform that things on one data feed will have compensating

effects on another. The usage pattern

import backtrader as bt

cerebro = bt.Cerebro()

data0 = bt.feeds.MyFavouriteDataFeed(dataname='futurename')

cerebro.adddata(data0)

data1 = bt.feeds.MyFavouriteDataFeed(dataname='spotname')

data1.compensate(data0) # let the system know ops on data1 affect data0

cerebro.adddata(data1)

...

cerebro.run()

Putting it all together

An example is always worth a thousand posts, so let’s put all the pieces together for it.

-

Use one of the standard sample feeds from the

backtradersources. This will be the future -

Simulate a similar but distinct price, by reusing the same feed and adding a filter which will randomly move the price some points above/below, to create a spread. As simple as:

# The filter which changes the close price def close_changer(data, *args, **kwargs): data.close[0] += 50.0 * random.randint(-1, 1) return False # length of stream is unchanged -

Plotting on the same axis will mix the default included

BuyObservermarkers and therefore the standard observers will be disabled and manually readded to plot with different per-data markers -

Positions will be entered randomly and exited 10 days later

This doesn’t match future expiration periods, but this is just putting the functionality in place and not checking a trading calendar

!!! note

A simulation including execution on the spot price on the day of

future expiration would require activating `cheat-on-close` to

make sure the orders are executed when the future expires. This is

not needed in this sample, because the expiration is being chosen

at random.

-

Notice that the strategy

-

buyoperations are executed ondata0 -

selloperations are executed ondata1

class St(bt.Strategy): def __init__(self): bt.obs.BuySell(self.data0, barplot=True) # done here for BuySellArrows(self.data1, barplot=True) # different markers per data def next(self): if not self.position: if random.randint(0, 1): self.buy(data=self.data0) self.entered = len(self) else: # in the market if (len(self) - self.entered) >= 10: self.sell(data=self.data1) -

The execution:

$ ./future-spot.py --no-comp

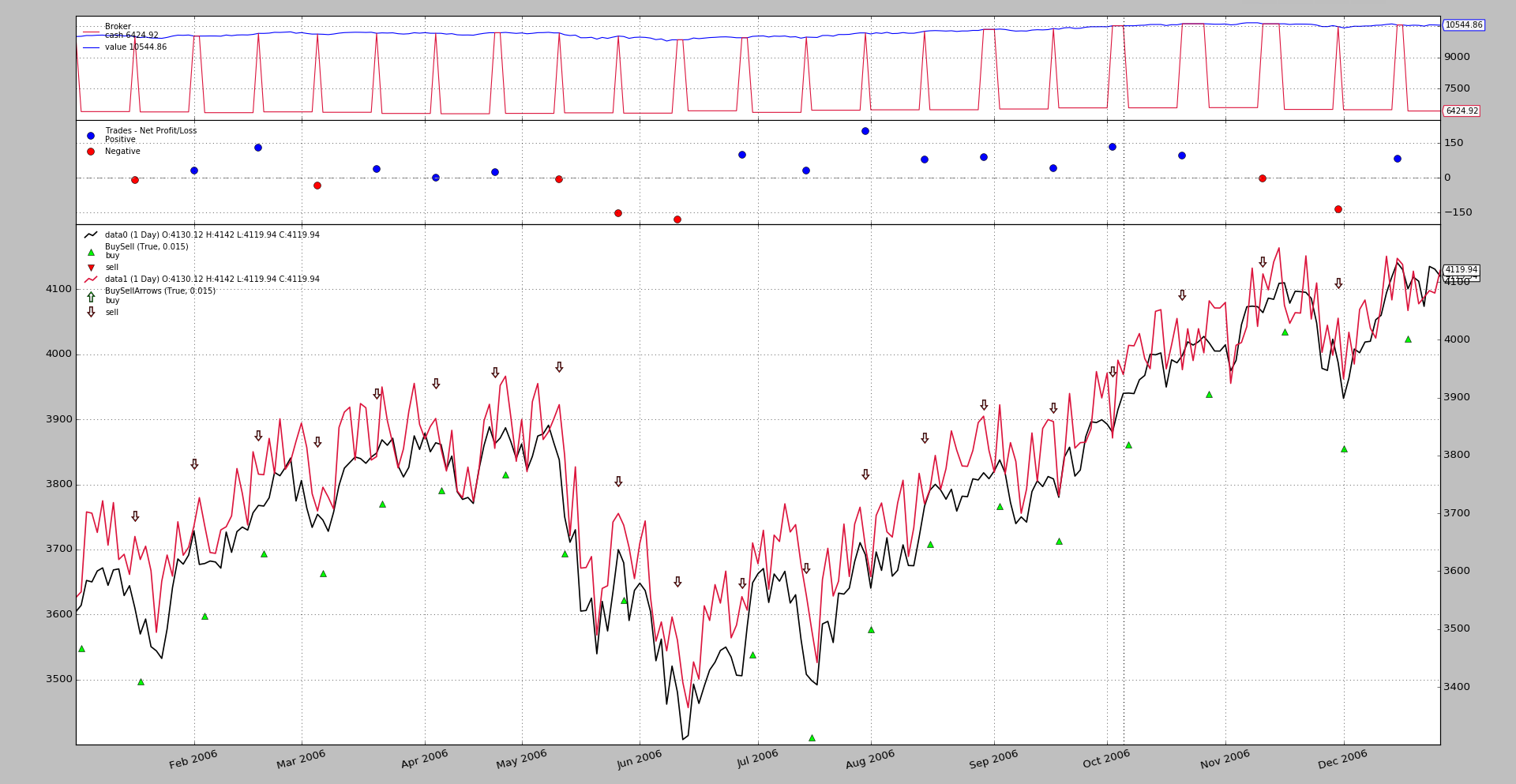

With this graphical output.

And it works:

-

buyoperations are signaled with a green triangle pointing upwards and the legend tells us they belong todata0as expected -

selloperations are signaled with an arrow pointing downwards and the legend tells us they belong todata1as expected -

Trades are being closed, even if they are being open with

data0and being closed withdata1, achieving the desired effect (which in real life is avoiding the physical delivery of the goods acquired by means of the future)

One could only imagine what would happen if the same logic is applied without the compensation taking place. Let’s do it:

$ ./future-spot.py --no-comp

And the output

It should be quite obvious that this fails miserably:

-

The logic expects positions on

data0to be closed by the operations ondata1and to only open positions ondata0when not in the market -

But compensation has been deactivated and the intial operation on

data0(green triangle) is never closed, so no other operation can never be initiated and short positions ondata1start accumulating.

Sample Usage

$ ./future-spot.py --help

usage: future-spot.py [-h] [--no-comp]

Compensation example

optional arguments:

-h, --help show this help message and exit

--no-comp

Sample Code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import random

import backtrader as bt

# The filter which changes the close price

def close_changer(data, *args, **kwargs):

data.close[0] += 50.0 * random.randint(-1, 1)

return False # length of stream is unchanged

# override the standard markers

class BuySellArrows(bt.observers.BuySell):

plotlines = dict(buy=dict(marker='$\u21E7$', markersize=12.0),

sell=dict(marker='$\u21E9$', markersize=12.0))

class St(bt.Strategy):

def __init__(self):

bt.obs.BuySell(self.data0, barplot=True) # done here for

BuySellArrows(self.data1, barplot=True) # different markers per data

def next(self):

if not self.position:

if random.randint(0, 1):

self.buy(data=self.data0)

self.entered = len(self)

else: # in the market

if (len(self) - self.entered) >= 10:

self.sell(data=self.data1)

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

dataname = '../../datas/2006-day-001.txt' # data feed

data0 = bt.feeds.BacktraderCSVData(dataname=dataname, name='data0')

cerebro.adddata(data0)

data1 = bt.feeds.BacktraderCSVData(dataname=dataname, name='data1')

data1.addfilter(close_changer)

if not args.no_comp:

data1.compensate(data0)

data1.plotinfo.plotmaster = data0

cerebro.adddata(data1)

cerebro.addstrategy(St) # sample strategy

cerebro.addobserver(bt.obs.Broker) # removed below with stdstats=False

cerebro.addobserver(bt.obs.Trades) # removed below with stdstats=False

cerebro.broker.set_coc(True)

cerebro.run(stdstats=False) # execute

cerebro.plot(volume=False) # and plot

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description=('Compensation example'))

parser.add_argument('--no-comp', required=False, action='store_true')

return parser.parse_args(pargs)

if __name__ == '__main__':

runstrat()