Commissions: Stocks vs Futures

Agnosticity

Before going forward let’s remember that backtrader tries to remain agnostic

as to what the data represents. Different commission schemes can be applied to

the same data set.

Let’s see how it can be done.

Using the broker shortcuts

This keeps the end user away from CommissionInfo objects because a

commission scheme can be created/set with a single function call. Within the

regular cerebro creation/set-up process, just add a call to

setcommission over the broker member attribute. The following call sets

a usual commission scheme for Eurostoxx50 futures when working with

Interactive Brokers:

cerebro.broker.setcommission(commission=2.0, margin=2000.0, mult=10.0)

Since most users will usually just test a single instrument, that’s all that’s

down to it. If you have given a name to your data feed, because several

instruments are being considered simultaneously on a chart, this call can be

slightly extended to look as follows:

cerebro.broker.setcommission(commission=2.0, margin=2000.0, mult=10.0, name='Eurostoxxx50')

In this case this on-the-fly commission scheme will only applied to instruments

whose name matches Eurostoxx50.

The meaning of the setcommission parameters

-

commission(default:0.0)Monetary units in absolute or percentage terms each action costs.

In the above example it is 2.0 euros per contract for a

buyand again 2.0 euros per contract for asell.The important issue here is when to use absolute or percentage values.

-

If

marginevaluates toFalse(it is False, 0 or None for example) then it will be considered thatcommissionexpresses a percentage of thepricetimessizeoperatin value -

If

marginis something else, it is considered the operations are happenning on afutureslike intstrument andcommissionis a fixed price persizecontracts

-

-

margin(default:None)Margin money needed when operating with

futureslike instruments. As expressed above-

If a no

marginis set, thecommissionwill be understood to be indicated in percentage and applied toprice * sizecomponents of abuyorselloperation -

If a

marginis set, thecommissionwill be understood to be a fixed value which is multiplied by thesizecomponent ofbuyorselloperation

-

-

mult(default: 1.0)For

futurelike instruments this determines the multiplicator to apply to profit and loss calculations.This is what makes futures attractive and risky at the same time.

-

name(default: None)Limit the application of the commission scheme to instruments matching

nameThis can be set during the creation of a data feed.

If left unset, the scheme will apply to any data present in the system.

Two examples now: stocks vs futures

The futures example from above:

cerebro.broker.setcommission(commission=2.0, margin=2000.0, mult=10.0)

A example for stocks:

cerebro.broker.setcommission(commission=0.005) # 0.5% of the operation value

Note

The 2nd syntax doesn’t set margin and mult and backtrader attempts a

smart approach by considering the commission to be % based.

To fully specify commission schemes, a subclass of CommissionInfo needs

to be created

Creating permanent Commission schemes

A more permanent commission scheme can be created by working directly with

CommissionInfo classes. The user could choose to have this definition

somewhere:

import backtrader as bt

commEurostoxx50 = bt.CommissionInfo(commission=2.0, margin=2000.0, mult=10.0)

To later apply it in another Python module with addcommissioninfo:

from mycomm import commEurostoxx50

...

cerebro.broker.addcommissioninfo(commEuroStoxx50, name='Eurostoxxx50')

CommissionInfo is an object which uses a params declaration just like

other objects in the backtrader environment. As such the above can be also

expressed as:

import backtrader as bt

class CommEurostoxx50(bt.CommissionInfo):

params = dict(commission=2.0, margin=2000.0, mult=10.0)

And later:

from mycomm import CommEurostoxx50

...

cerebro.broker.addcommissioninfoCommEuroStoxx50(), name='Eurostoxxx50')

Now a “real” comparison with a SMA Crossover

Using a SimpleMovingAverage crossover as the entry/exit signal the same data set

is going to be tested with a futures like commission scheme and then with a

stocks like one.

Note

Futures positions could also not only be given the enter/exit behavior but a reversal behavior on each occassion. But this example is about comparing the commission schemes.

The code (see at the bottom for the full strategy) is the same and the scheme can be chosen before the strategy is defined.

futures_like = True

if futures_like:

commission, margin, mult = 2.0, 2000.0, 10.0

else:

commission, margin, mult = 0.005, None, 1

Just set futures_like to false to run with the stocks like scheme.

Some logging code has been added to evaluate the impact of the differrent commission schemes. Let’s concentrate on just the 2 first operations.

For futures:

2006-03-09, BUY CREATE, 3757.59

2006-03-10, BUY EXECUTED, Price: 3754.13, Cost: 2000.00, Comm 2.00

2006-04-11, SELL CREATE, 3788.81

2006-04-12, SELL EXECUTED, Price: 3786.93, Cost: 2000.00, Comm 2.00

2006-04-12, OPERATION PROFIT, GROSS 328.00, NET 324.00

2006-04-20, BUY CREATE, 3860.00

2006-04-21, BUY EXECUTED, Price: 3863.57, Cost: 2000.00, Comm 2.00

2006-04-28, SELL CREATE, 3839.90

2006-05-02, SELL EXECUTED, Price: 3839.24, Cost: 2000.00, Comm 2.00

2006-05-02, OPERATION PROFIT, GROSS -243.30, NET -247.30

For stocks:

2006-03-09, BUY CREATE, 3757.59

2006-03-10, BUY EXECUTED, Price: 3754.13, Cost: 3754.13, Comm 18.77

2006-04-11, SELL CREATE, 3788.81

2006-04-12, SELL EXECUTED, Price: 3786.93, Cost: 3786.93, Comm 18.93

2006-04-12, OPERATION PROFIT, GROSS 32.80, NET -4.91

2006-04-20, BUY CREATE, 3860.00

2006-04-21, BUY EXECUTED, Price: 3863.57, Cost: 3863.57, Comm 19.32

2006-04-28, SELL CREATE, 3839.90

2006-05-02, SELL EXECUTED, Price: 3839.24, Cost: 3839.24, Comm 19.20

2006-05-02, OPERATION PROFIT, GROSS -24.33, NET -62.84

The 1st operation has the following prices:

-

BUY (Execution) -> 3754.13 / SELL (Execution) -> 3786.93

-

Futures Profit & Loss (with commission): 324.0

-

Stocks Profit & Loss (with commission): -4.91

-

Hey!! Commission has fully eaten up any profit on the stocks operation

but has only meant a small dent to the futures one.

The 2nd operation:

-

BUY (Execution) ->

3863.57/ SELL (Execution) ->3389.24-

Futures Profit & Loss (with commission):

-247.30 -

Stocks Profit & Loss (with commission):

-62.84

-

The bite has been sensibly larger for this negative operation with futures

But:

-

Futures accumulated net profit & loss:

324.00 + (-247.30) = 76.70 -

Stocks accumulated net profit & loss:

(-4.91) + (-62.84) = -67.75

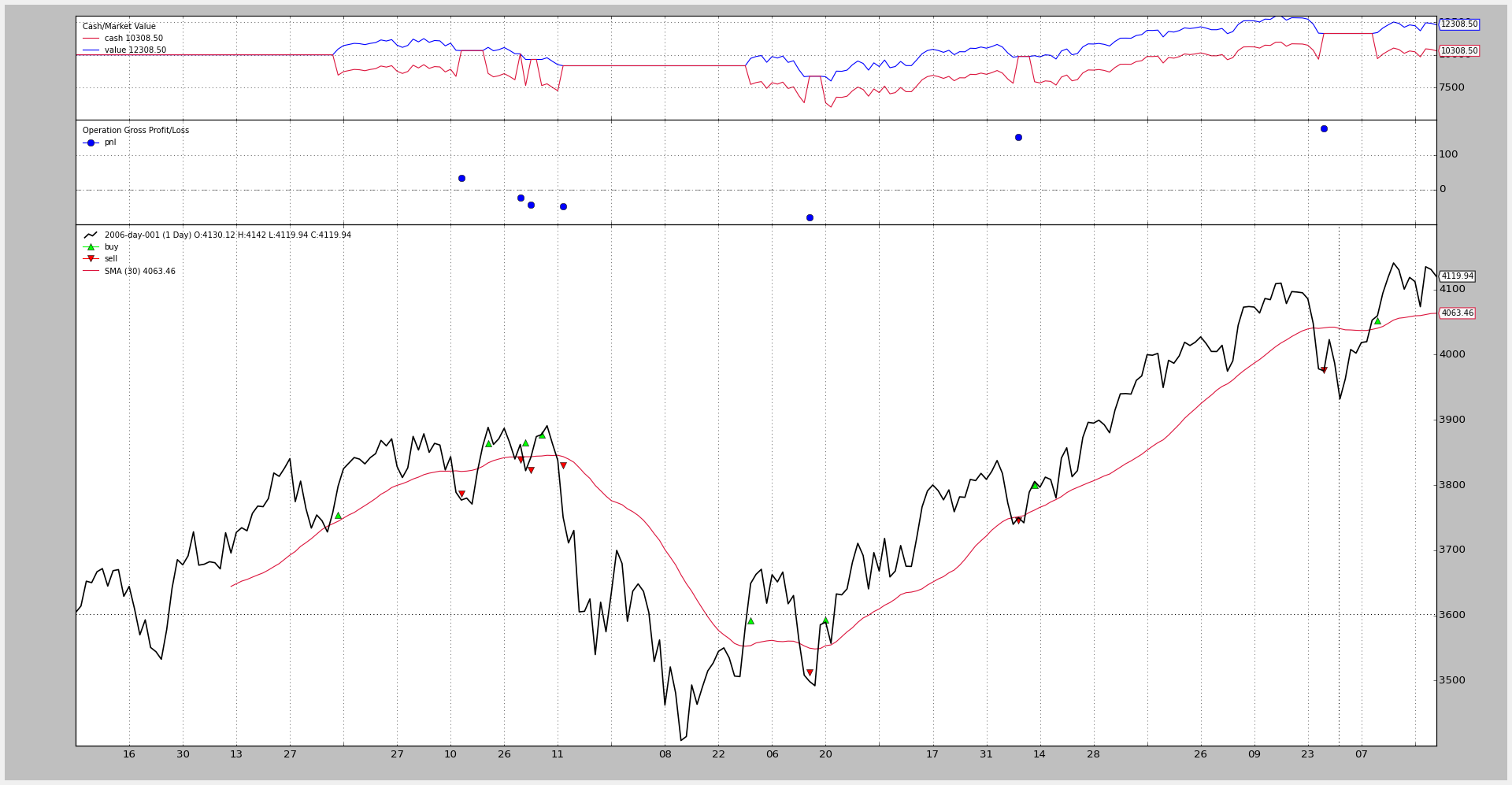

The accumulated effect can be seen on the charts below, where it can also be seen that at the end of the full year, futures have produced a larger profit, but have also suffered a larger drawdown (were deeper underwater)

But the important thing: whether futures or stocks … it can be

backtested.

Commissions for futures

Commissions for stocks

The code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

futures_like = True

if futures_like:

commission, margin, mult = 2.0, 2000.0, 10.0

else:

commission, margin, mult = 0.005, None, 1

class SMACrossOver(bt.Strategy):

def log(self, txt, dt=None):

''' Logging function fot this strategy'''

dt = dt or self.datas[0].datetime.date(0)

print('%s, %s' % (dt.isoformat(), txt))

def notify(self, order):

if order.status in [order.Submitted, order.Accepted]:

# Buy/Sell order submitted/accepted to/by broker - Nothing to do

return

# Check if an order has been completed

# Attention: broker could reject order if not enougth cash

if order.status in [order.Completed, order.Canceled, order.Margin]:

if order.isbuy():

self.log(

'BUY EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

self.buyprice = order.executed.price

self.buycomm = order.executed.comm

self.opsize = order.executed.size

else: # Sell

self.log('SELL EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

gross_pnl = (order.executed.price - self.buyprice) * \

self.opsize

if margin:

gross_pnl *= mult

net_pnl = gross_pnl - self.buycomm - order.executed.comm

self.log('OPERATION PROFIT, GROSS %.2f, NET %.2f' %

(gross_pnl, net_pnl))

def __init__(self):

sma = btind.SMA(self.data)

# > 0 crossing up / < 0 crossing down

self.buysell_sig = btind.CrossOver(self.data, sma)

def next(self):

if self.buysell_sig > 0:

self.log('BUY CREATE, %.2f' % self.data.close[0])

self.buy() # keep order ref to avoid 2nd orders

elif self.position and self.buysell_sig < 0:

self.log('SELL CREATE, %.2f' % self.data.close[0])

self.sell()

if __name__ == '__main__':

# Create a cerebro entity

cerebro = bt.Cerebro()

# Add a strategy

cerebro.addstrategy(SMACrossOver)

# Create a Data Feed

datapath = ('../../datas/2006-day-001.txt')

data = bt.feeds.BacktraderCSVData(dataname=datapath)

# Add the Data Feed to Cerebro

cerebro.adddata(data)

# set commission scheme -- CHANGE HERE TO PLAY

cerebro.broker.setcommission(

commission=commission, margin=margin, mult=mult)

# Run over everything

cerebro.run()

# Plot the result

cerebro.plot()

Reference

class backtrader.CommInfoBase()

Base Class for the Commission Schemes.

Params:

-

commission(def:0.0): base commission value in percentage or monetary units -

mult(def1.0): multiplier applied to the asset for value/profit -

margin(def:None): amount of monetary units needed to open/hold an operation. It only applies if the final_stocklikeattribute in the class is set toFalse -

automargin(def:False): Used by the methodget_marginto automatically calculate the margin/guarantees needed with the following policy-

Use param

marginif paramautomarginevaluates toFalse -

Use param

multand usemult * priceifautomargin < 0 -

Use param

automarginand useautomargin * priceifautomargin > 0

-

-

commtype(def:None): Supported values areCommInfoBase.COMM_PERC(commission to be understood as %) andCommInfoBase.COMM_FIXED(commission to be understood as monetary units)The default value of

Noneis a supported value to retain compatibility with the legacyCommissionInfoobject. Ifcommtypeis set to None, then the following applies:-

marginisNone: Internal_commtypeis set toCOMM_PERCand_stocklikeis set toTrue(Operating %-wise with Stocks) -

marginis notNone:_commtypeset toCOMM_FIXEDand_stocklikeset toFalse(Operating with fixed rount-trip commission with Futures)

If this param is set to something else than

None, then it will be passed to the internal_commtypeattribute and the same will be done with the paramstocklikeand the internal attribute_stocklike -

-

stocklike(def:False): Indicates if the instrument is Stock-like or Futures-like (see thecommtypediscussion above) -

percabs(def:False): whencommtypeis set to COMM_PERC, whether the parametercommissionhas to be understood as XX% or 0.XXIf this param is

True: 0.XX If this param isFalse: XX% -

interest(def:0.0)If this is non-zero, this is the yearly interest charged for holding a short selling position. This is mostly meant for stock short-selling

The formula:

days * price * abs(size) * (interest / 365)It must be specified in absolute terms: 0.05 -> 5%

Note

the behavior can be changed by overriding the method:

_get_credit_interest -

interest_long(def:False)Some products like ETFs get charged on interest for short and long positions. If ths is

Trueandinterestis non-zero the interest will be charged on both directions -

leverage(def:1.0)Amount of leverage for the asset with regards to the needed cash

- ``_stocklike``()

Final value to use for Stock-like/Futures-like behavior

- ``_commtype``()

Final value to use for PERC vs FIXED commissions

This two are used internally instead of the declared params to enable the()

compatibility check described above for the legacy ``CommissionInfo``()

object()

class backtrader.CommissionInfo()

Base Class for the actual Commission Schemes.

CommInfoBase was created to keep suppor for the original, incomplete,

support provided by backtrader. New commission schemes derive from this

class which subclasses CommInfoBase.

The default value of percabs is also changed to True

Params:

-

percabs(def: True): whencommtypeis set to COMM_PERC, whether the parametercommissionhas to be understood as XX% or 0.XXIf this param is True: 0.XX If this param is False: XX%

get_leverage()

Returns the level of leverage allowed for this comission scheme

getsize(price, cash)

Returns the needed size to meet a cash operation at a given price

getoperationcost(size, price)

Returns the needed amount of cash an operation would cost

getvaluesize(size, price)

Returns the value of size for given a price. For future-like

objects it is fixed at size * margin

getvalue(position, price)

Returns the value of a position given a price. For future-like

objects it is fixed at size * margin

get_margin(price)

Returns the actual margin/guarantees needed for a single item of the asset at the given price. The default implementation has this policy:

-

Use param

marginif paramautomarginevaluates toFalse -

Use param

mult, i.e.mult * priceifautomargin < 0 -

Use param

automargin, i.e.automargin * priceifautomargin > 0

getcommission(size, price)

Calculates the commission of an operation at a given price

_getcommission(size, price, pseudoexec)

Calculates the commission of an operation at a given price

pseudoexec: if True the operation has not yet been executed

profitandloss(size, price, newprice)

Return actual profit and loss a position has

cashadjust(size, price, newprice)

Calculates cash adjustment for a given price difference

get_credit_interest(data, pos, dt)

Calculates the credit due for short selling or product specific

_get_credit_interest(data, size, price, days, dt0, dt1)

This method returns the cost in terms of credit interest charged by the broker.

In the case of size > 0 this method will only be called if the

parameter to the class interest_long is True

The formulat for the calculation of the credit interest rate is:

The formula: days * price * abs(size) * (interest / 365)

Params:

* `data`: data feed for which interest is charged

* `size`: current position size. > 0 for long positions and < 0 for

short positions (this parameter will not be `0`)

* `price`: current position price

* `days`: number of days elapsed since last credit calculation

(this is (dt0 - dt1).days)

* `dt0`: (datetime.datetime) current datetime

* `dt1`: (datetime.datetime) datetime of previous calculation

dt0 and dt1 are not used in the default implementation and are

provided as extra input for overridden methods