Stop Trading

Trading can be dangerous and trading using stop orders can help into either avoiding big losses or securing profits. backtrader provides you with several mechanisms to implement Stop - based strategies

Basic Strategy

A classic Fast EMA crosses over a Slow EMA approach will be used. But:

-

Only the up-cross will be taken into account to issue a

buyorder -

Exiting the market, i.e.:

sellwill be done via aStop

The strategy will therefore start with this simple skeleton

class BaseStrategy(bt.Strategy):

params = dict(

fast_ma=10,

slow_ma=20,

)

def __init__(self):

# omitting a data implies self.datas[0] (aka self.data and self.data0)

fast_ma = bt.ind.EMA(period=self.p.fast_ma)

slow_ma = bt.ind.EMA(period=self.p.slow_ma)

# our entry point

self.crossup = bt.ind.CrossUp(fast_ma, slow_ma)

And using inheritance we’ll work out different approaches as to how to implement the Stops

Manual Approach

To avoid having too many approaches, this subclass of our basic strategy will allow:

-

Either having a

Stopfixed at a percentage below the acquisition price -

Or setting a dynamic

StopTrailwhich chases the price as it moves (using points in this case)

class ManualStopOrStopTrail(BaseStrategy):

params = dict(

stop_loss=0.02, # price is 2% less than the entry point

trail=False,

)

def notify_order(self, order):

if not order.status == order.Completed:

return # discard any other notification

if not self.position: # we left the market

print('SELL@price: {:.2f}'.format(order.executed.price))

return

# We have entered the market

print('BUY @price: {:.2f}'.format(order.executed.price))

if not self.p.trail:

stop_price = order.executed.price * (1.0 - self.p.stop_loss)

self.sell(exectype=bt.Order.Stop, price=stop_price)

else:

self.sell(exectype=bt.Order.StopTrail, trailamount=self.p.trail)

def next(self):

if not self.position and self.crossup > 0:

# not in the market and signal triggered

self.buy()

As you may see, we have added parameters for

-

The percentage:

stop_loss=0.02(2%) -

Or

trail=False, which when set to a numeric value will tell the strategy to use aStopTrail

For the documentation on orders see:

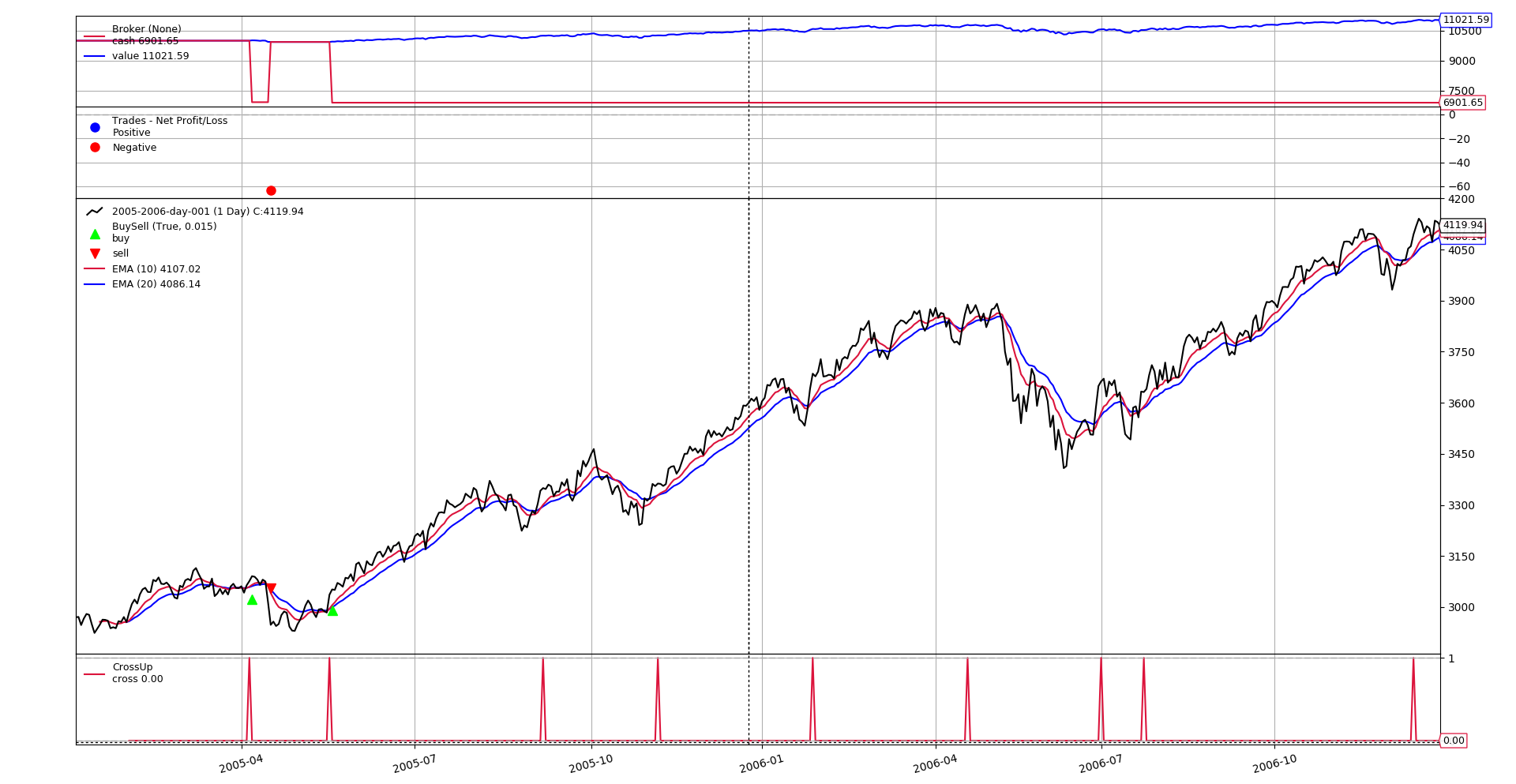

Let’s execute our script with a fixed Stop:

$ ./stop-loss-approaches.py manual --plot

BUY @price: 3073.40

SELL@price: 3009.93

BUY @price: 3034.88

And the chart

As we see:

-

When there is an up-cross a

buyis issued -

When this

buyis notified asCompletedwe issue aStoporder with pricestop_losspercent below theexecuted.price

Result:

-

The first instance is quickly stopped-out

-

But because the sample data is one from a trending market … there is no further instance of the price going below the

stop_losspercentage

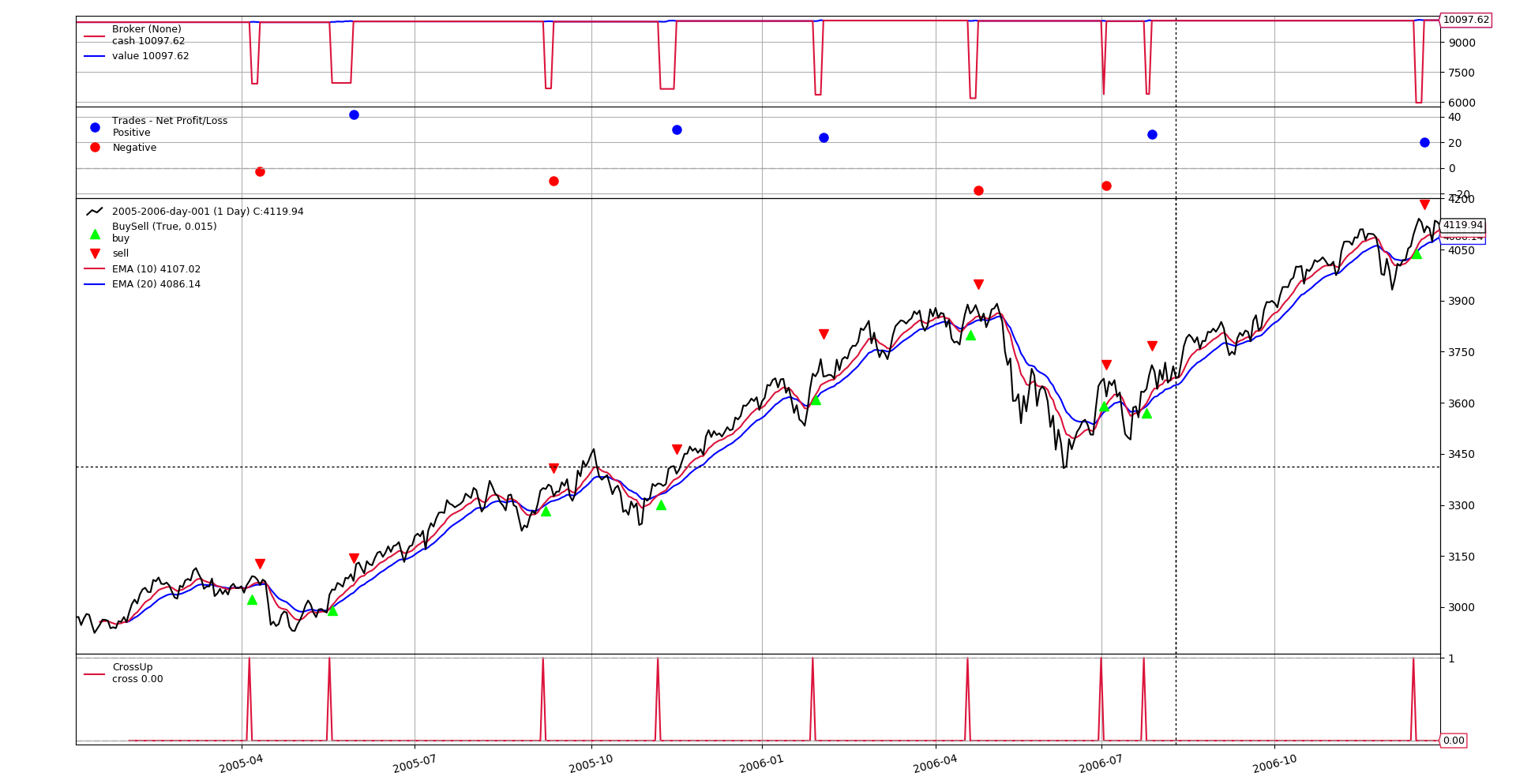

Let’s use the same approach but applying a StopTrail order:

$ ./stop-loss-approaches.py manual --plot --strat trail=20

BUY @price: 3073.40

SELL@price: 3070.72

BUY @price: 3034.88

SELL@price: 3076.54

BUY @price: 3349.72

SELL@price: 3339.65

BUY @price: 3364.26

SELL@price: 3393.96

BUY @price: 3684.38

SELL@price: 3708.25

BUY @price: 3884.57

SELL@price: 3867.00

BUY @price: 3664.59

SELL@price: 3650.75

BUY @price: 3635.17

SELL@price: 3661.55

BUY @price: 4100.49

SELL@price: 4120.66

And the chart

Now we see how this, compared to the previous approach, is not so productive.

-

Although the market is trending, the price drops several times more than

20points (our trail value) -

And this takes us out of the market

-

And because the market is trending, it takes time for the moving averages to cross again in the desired direction

Why using notify_order?

Because this ensures that the order that has to be controlled by the Stop

has actually been executed. This may not be a big deal during backtesting but

it is when trading live.

Let’s simplify the approach for backtesting, by using the cheat-on-close

mode available with backtrader.

class ManualStopOrStopTrailCheat(BaseStrategy):

params = dict(

stop_loss=0.02, # price is 2% less than the entry point

trail=False,

)

def __init__(self):

super().__init__()

self.broker.set_coc(True)

def notify_order(self, order):

if not order.status == order.Completed:

return # discard any other notification

if not self.position: # we left the market

print('SELL@price: {:.2f}'.format(order.executed.price))

return

# We have entered the market

print('BUY @price: {:.2f}'.format(order.executed.price))

def next(self):

if not self.position and self.crossup > 0:

# not in the market and signal triggered

self.buy()

if not self.p.trail:

stop_price = self.data.close[0] * (1.0 - self.p.stop_loss)

self.sell(exectype=bt.Order.Stop, price=stop_price)

else:

self.sell(exectype=bt.Order.StopTrail,

trailamount=self.p.trail)

In this case:

-

The

cheat-on-closemode is activated in the broker during the__init__phase of the strategy -

The

StopOrderis issued immediately after thebuyorder. This is becausecheat-on-closeensures it will be executed without waiting for the next barNotice that the closing price (

self.data.close[0]) is used for the stop, because there is no execution price yet. And we know that it will be the closing price thanks tocheat-on-close -

The

notify_ordermethod is now purely a logging method which tells us when things have been bought or sold.

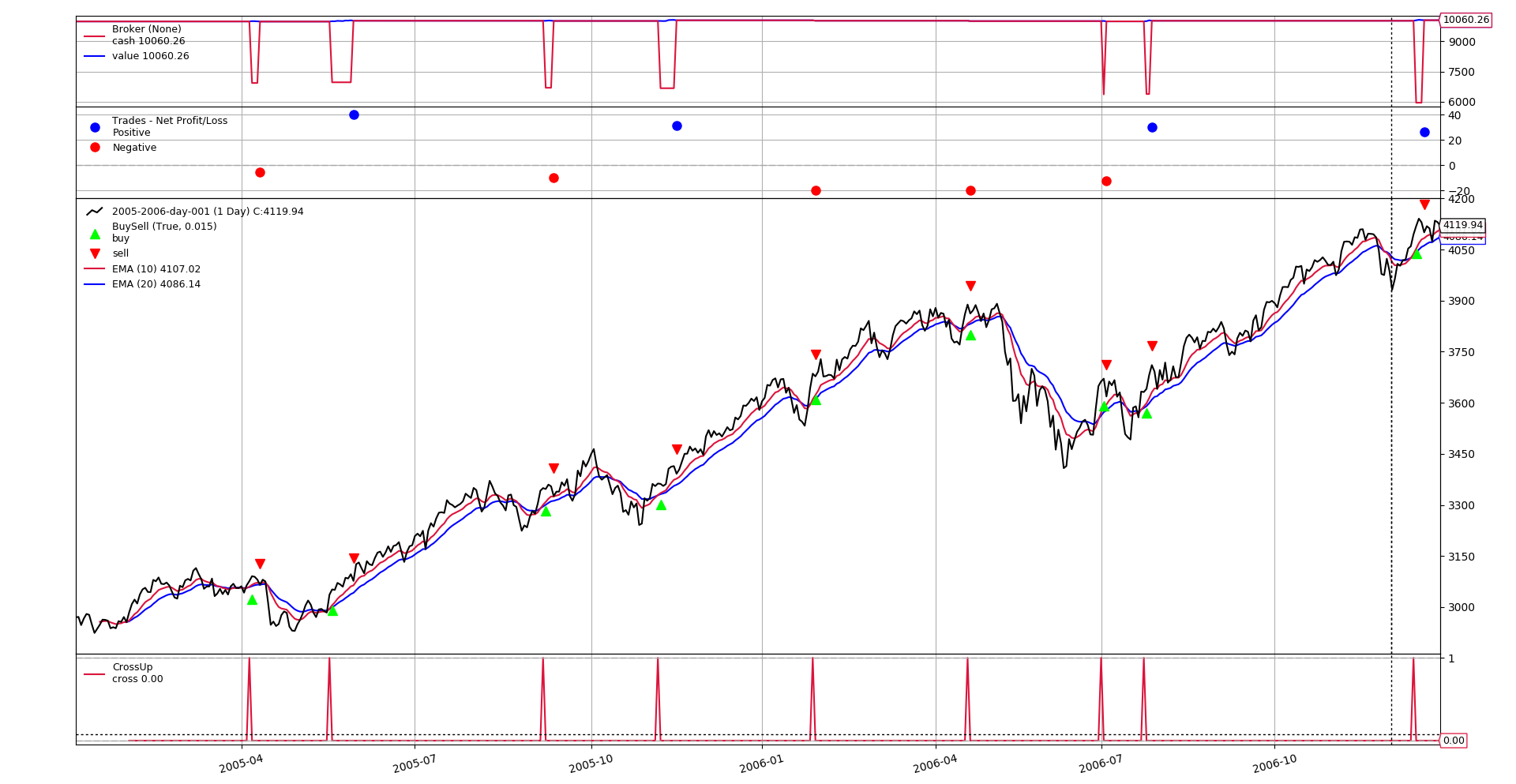

A sample run with StopTrail:

$ ./stop-loss-approaches.py manualcheat --plot --strat trail=20

BUY @price: 3076.23

SELL@price: 3070.72

BUY @price: 3036.30

SELL@price: 3076.54

BUY @price: 3349.46

SELL@price: 3339.65

BUY @price: 3362.83

SELL@price: 3393.96

SELL@price: 3685.48

SELL@price: 3665.48

SELL@price: 3888.46

SELL@price: 3868.46

BUY @price: 3662.92

SELL@price: 3650.75

BUY @price: 3631.50

SELL@price: 3661.55

BUY @price: 4094.33

SELL@price: 4120.66

And the chart

Notice that:

-

The results are very similar but not the same as before

This is due to

cheat-on-closegiving the strategy the closing price (which is non-realistic, but can be a good approximation) instead of the next available price (which is the next opening price)

Automating the approach

It would be perfect if the logic for the orders could be kept together in

next and one didn’t have to use cheat-on-close. And it can be done!!!

Let’s use

- Parent-Child orders

class AutoStopOrStopTrail(BaseStrategy):

params = dict(

stop_loss=0.02, # price is 2% less than the entry point

trail=False,

buy_limit=False,

)

buy_order = None # default value for a potential buy_order

def notify_order(self, order):

if order.status == order.Cancelled:

print('CANCEL@price: {:.2f} {}'.format(

order.executed.price, 'buy' if order.isbuy() else 'sell'))

return

if not order.status == order.Completed:

return # discard any other notification

if not self.position: # we left the market

print('SELL@price: {:.2f}'.format(order.executed.price))

return

# We have entered the market

print('BUY @price: {:.2f}'.format(order.executed.price))

def next(self):

if not self.position and self.crossup > 0:

if self.buy_order: # something was pending

self.cancel(self.buy_order)

# not in the market and signal triggered

if not self.p.buy_limit:

self.buy_order = self.buy(transmit=False)

else:

price = self.data.close[0] * (1.0 - self.p.buy_limit)

# transmit = False ... await child order before transmission

self.buy_order = self.buy(price=price, exectype=bt.Order.Limit,

transmit=False)

# Setting parent=buy_order ... sends both together

if not self.p.trail:

stop_price = self.data.close[0] * (1.0 - self.p.stop_loss)

self.sell(exectype=bt.Order.Stop, price=stop_price,

parent=self.buy_order)

else:

self.sell(exectype=bt.Order.StopTrail,

trailamount=self.p.trail,

parent=self.buy_order)

This new strategy, which still builds on BaseStrategy, does:

-

Add the possibility to issue the

buyorder as aLimitorderThe parameter

buy_limit(when notFalse) will be a percentage to take off the current price to set the expected buy point. -

Sets

transmit=Falsefor thebuyorder. This means the order won’t be transmitted to the broker immediately. It will await the transmission signal from a child order -

Immediately issues a child order by using:

parent=buy_order-

This will trigger transmitting both orders to the broker

-

And will tag the child order for scheduling when the parent order has been executed.

No risk of the

Stoporder executing before thebuyorder is in place.- If the parent order is cancelled, the child order will also be cancelled

-

-

Being this a sample and with a trending market, the

Limitorder may never be executed and still be active when a new signal comes in. In this case the sample will simple cancel the pendingbuyorder and carry on with a new one at the current price levels.This, as stated above, will cancel the child

Stoporder. -

Cancelled orders will be logged

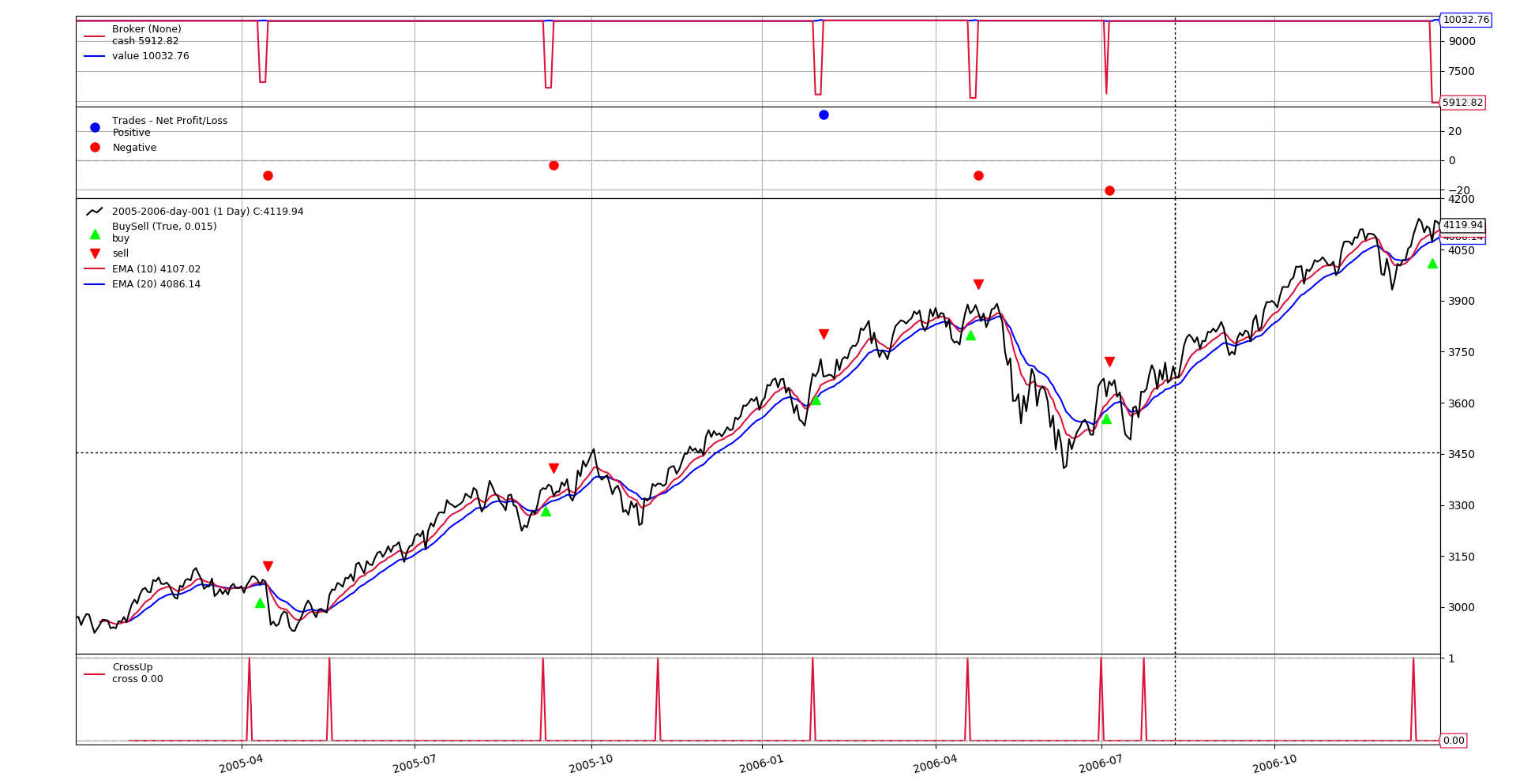

Let’s execute trying to buy 0.5% below the current close price and with

trail=30

A sample run with StopTrail:

$ ./stop-loss-approaches.py auto --plot --strat trail=30,buy_limit=0.005

BUY @price: 3060.85

SELL@price: 3050.54

CANCEL@price: 0.00 buy

CANCEL@price: 0.00 sell

BUY @price: 3332.71

SELL@price: 3329.65

CANCEL@price: 0.00 buy

CANCEL@price: 0.00 sell

BUY @price: 3667.05

SELL@price: 3698.25

BUY @price: 3869.02

SELL@price: 3858.46

BUY @price: 3644.61

SELL@price: 3624.02

CANCEL@price: 0.00 buy

CANCEL@price: 0.00 sell

BUY @price: 4073.86

And the chart

The log and the buy/sell signs on the chart show that no sell order was

executed without having a corresponding buy order, and that cancelled

buy orders where immediately followed by the cancellation of the child

sell order (without any manual coding)

Conclusion

Using different approaches for how to trade with stops has been shown. This can be used to avoid losses or secure profit.

Beware: very tight stop orders could also simply have the effect of getting your positions out of the market, if the stop is set within the normal range of movement of the price.

Script Usage

$ ./stop-loss-approaches.py --help

usage: stop-loss-approaches.py [-h] [--data0 DATA0] [--fromdate FROMDATE]

[--todate TODATE] [--cerebro kwargs]

[--broker kwargs] [--sizer kwargs]

[--strat kwargs] [--plot [kwargs]]

{manual,manualcheat,auto}

Stop-Loss Approaches

positional arguments:

{manual,manualcheat,auto}

Stop approach to use

optional arguments:

-h, --help show this help message and exit

--data0 DATA0 Data to read in (default:

../../datas/2005-2006-day-001.txt)

--fromdate FROMDATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default: )

--todate TODATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default: )

--cerebro kwargs kwargs in key=value format (default: )

--broker kwargs kwargs in key=value format (default: )

--sizer kwargs kwargs in key=value format (default: )

--strat kwargs kwargs in key=value format (default: )

--plot [kwargs] kwargs in key=value format (default: )

The code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import backtrader as bt

class BaseStrategy(bt.Strategy):

params = dict(

fast_ma=10,

slow_ma=20,

)

def __init__(self):

# omitting a data implies self.datas[0] (aka self.data and self.data0)

fast_ma = bt.ind.EMA(period=self.p.fast_ma)

slow_ma = bt.ind.EMA(period=self.p.slow_ma)

# our entry point

self.crossup = bt.ind.CrossUp(fast_ma, slow_ma)

class ManualStopOrStopTrail(BaseStrategy):

params = dict(

stop_loss=0.02, # price is 2% less than the entry point

trail=False,

)

def notify_order(self, order):

if not order.status == order.Completed:

return # discard any other notification

if not self.position: # we left the market

print('SELL@price: {:.2f}'.format(order.executed.price))

return

# We have entered the market

print('BUY @price: {:.2f}'.format(order.executed.price))

if not self.p.trail:

stop_price = order.executed.price * (1.0 - self.p.stop_loss)

self.sell(exectype=bt.Order.Stop, price=stop_price)

else:

self.sell(exectype=bt.Order.StopTrail, trailamount=self.p.trail)

def next(self):

if not self.position and self.crossup > 0:

# not in the market and signal triggered

self.buy()

class ManualStopOrStopTrailCheat(BaseStrategy):

params = dict(

stop_loss=0.02, # price is 2% less than the entry point

trail=False,

)

def __init__(self):

super().__init__()

self.broker.set_coc(True)

def notify_order(self, order):

if not order.status == order.Completed:

return # discard any other notification

if not self.position: # we left the market

print('SELL@price: {:.2f}'.format(order.executed.price))

return

# We have entered the market

print('BUY @price: {:.2f}'.format(order.executed.price))

def next(self):

if not self.position and self.crossup > 0:

# not in the market and signal triggered

self.buy()

if not self.p.trail:

stop_price = self.data.close[0] * (1.0 - self.p.stop_loss)

self.sell(exectype=bt.Order.Stop, price=stop_price)

else:

self.sell(exectype=bt.Order.StopTrail,

trailamount=self.p.trail)

class AutoStopOrStopTrail(BaseStrategy):

params = dict(

stop_loss=0.02, # price is 2% less than the entry point

trail=False,

buy_limit=False,

)

buy_order = None # default value for a potential buy_order

def notify_order(self, order):

if order.status == order.Cancelled:

print('CANCEL@price: {:.2f} {}'.format(

order.executed.price, 'buy' if order.isbuy() else 'sell'))

return

if not order.status == order.Completed:

return # discard any other notification

if not self.position: # we left the market

print('SELL@price: {:.2f}'.format(order.executed.price))

return

# We have entered the market

print('BUY @price: {:.2f}'.format(order.executed.price))

def next(self):

if not self.position and self.crossup > 0:

if self.buy_order: # something was pending

self.cancel(self.buy_order)

# not in the market and signal triggered

if not self.p.buy_limit:

self.buy_order = self.buy(transmit=False)

else:

price = self.data.close[0] * (1.0 - self.p.buy_limit)

# transmit = False ... await child order before transmission

self.buy_order = self.buy(price=price, exectype=bt.Order.Limit,

transmit=False)

# Setting parent=buy_order ... sends both together

if not self.p.trail:

stop_price = self.data.close[0] * (1.0 - self.p.stop_loss)

self.sell(exectype=bt.Order.Stop, price=stop_price,

parent=self.buy_order)

else:

self.sell(exectype=bt.Order.StopTrail,

trailamount=self.p.trail,

parent=self.buy_order)

APPROACHES = dict(

manual=ManualStopOrStopTrail,

manualcheat=ManualStopOrStopTrailCheat,

auto=AutoStopOrStopTrail,

)

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

# Data feed kwargs

kwargs = dict()

# Parse from/to-date

dtfmt, tmfmt = '%Y-%m-%d', 'T%H:%M:%S'

for a, d in ((getattr(args, x), x) for x in ['fromdate', 'todate']):

if a:

strpfmt = dtfmt + tmfmt * ('T' in a)

kwargs[d] = datetime.datetime.strptime(a, strpfmt)

data0 = bt.feeds.BacktraderCSVData(dataname=args.data0, **kwargs)

cerebro.adddata(data0)

# Broker

cerebro.broker = bt.brokers.BackBroker(**eval('dict(' + args.broker + ')'))

# Sizer

cerebro.addsizer(bt.sizers.FixedSize, **eval('dict(' + args.sizer + ')'))

# Strategy

StClass = APPROACHES[args.approach]

cerebro.addstrategy(StClass, **eval('dict(' + args.strat + ')'))

# Execute

cerebro.run(**eval('dict(' + args.cerebro + ')'))

if args.plot: # Plot if requested to

cerebro.plot(**eval('dict(' + args.plot + ')'))

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description=(

'Stop-Loss Approaches'

)

)

parser.add_argument('--data0', default='../../datas/2005-2006-day-001.txt',

required=False, help='Data to read in')

# Strategy to choose

parser.add_argument('approach', choices=APPROACHES.keys(),

help='Stop approach to use')

# Defaults for dates

parser.add_argument('--fromdate', required=False, default='',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--todate', required=False, default='',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--cerebro', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--broker', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--sizer', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--strat', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--plot', required=False, default='',

nargs='?', const='{}',

metavar='kwargs', help='kwargs in key=value format')

return parser.parse_args(pargs)

if __name__ == '__main__':

runstrat()