Visual Chart Live Data/Trading

Starting with release 1.5.1.93, backtrader supports Visual Chart Live Feeds and Live Trading.

Needed things:

-

Visual Chart 6 (this one runs on Windows)

-

comtypes, specifically this fork: https://github.com/mementum/comtypesInstall it with:

pip install https://github.com/mementum/comtypes/archive/master.zipThe Visual Chart API is based on COM and the current

comtypesmain branch doesn’t support unpacking ofVT_ARRAYSofVT_RECORD. And this is used by Visual ChartPull Request #104 has been submitted but not yet integrated. As soon as it is integrated, the main branch can be used.

-

pytz(optional but strongly recommended)In many cases the internal

SymbolInfo.TimeOffsetprovided by the data feeds suffices to return data feeds in market time (even if the default configuration isLocalTimein Visual Chart)

If you don’t know what’s Visual Chart and/or its currently associated broker Esfera Capital, then visit the following sites:

Initial statement:

-

As always and before risking your money, TEST, TEST, TEST and RE-TEST a thousand times.

From bugs in this software, to bugs in your own software and the management of unexpected situations: Anything can go wrong

Some notes about this:

-

The data feed is rather good and supports built-in resampling. Good, because there is no need to do resampling.

-

The data feed doesn’t support Seconds resolution. Not good but solvable by the built-in resampling of backtrader

-

Backfilling is built-in

-

Some on the markets in

International Indices(in exchange096) have odd timezones and market offsets.Some work has gone into this to for example deliver

096.DJIin the expectedUS/Easterntimezone -

The data feed offers continuous futures which is very handy to have a large history.

As such a second parameter can be passed to a data to indicate which is the actual trading asset.

-

DateTime for a Good Til Date order can only be specified as a date. The time component is ignored.

-

There is no direct way to find the offset from the local equipment to the data server and a heuristic is needed to find this out from RealTime Ticks at the start of a session.

-

Passing a datetime with a time component (rather than the default 00:00:00) seems to create a time filter in the COM API. For example if you say you want the Minute data, starting 3 days ago at 14:30, you could do:

dt = datetime.now() - timedelta(days=3) dt.replace(hour=14, minute=30) vcstore.getdata(dataname='001ES', fromdate=dt)Data is then skipped until 14:30 not only 3 days ago, BUT EVERY OF THE DAYS AFTERWARDS

As such, please pass only full dates in the sense that the default time component is untouched.

-

The broker supports the notion of Positions but only when they are open. The last event with regards to a Position (which is size is 0) is not sent.

As such, Position accounting is done entirely by backtrader

-

The broker doesn’t report commissions.

The workaround is to supply your own

CommissionInfoderived class when instantiating the broker. See the backtader docs for creating your own class. It is rather easy. -

CancelledvsExpiredorders. This distinction doesn’t exist and an heuristic would be needed to try to clear the distinction out.As such only

Cancelledwill be reported

Some additional notes:

-

RealTime ticks are mostly not used. They produce large amounts of unneeded information for backtrader purposes. They have 2 main purposes before being completely disconnected by backtrader

-

Finding out if a Symbol exists.

-

Calculating the offset to the data server

Of course the information is gathered in realtime for prices but from DataSource objects, which provide the historical data at the same time.

-

As much as possible has been documented and is available at the usual documentation link:

A couple of runs from the sample vctest.pye against the Visual Chart and

the Demo Broker

First: 015ES (EuroStoxx50 continuous) with resampling to 1 minute and

featuring a disconnection and reconnection:

$ ./vctest.py --data0 015ES --timeframe Minutes --compression 1 --fromdate 2016-07-12

Output:

--------------------------------------------------

Strategy Created

--------------------------------------------------

Datetime, Open, High, Low, Close, Volume, OpenInterest, SMA

***** DATA NOTIF: CONNECTED

***** DATA NOTIF: DELAYED

0001, 2016-07-12T08:01:00.000000, 2871.0, 2872.0, 2869.0, 2872.0, 1915.0, 0.0, nan

0002, 2016-07-12T08:02:00.000000, 2872.0, 2872.0, 2870.0, 2871.0, 479.0, 0.0, nan

0003, 2016-07-12T08:03:00.000000, 2871.0, 2871.0, 2869.0, 2870.0, 518.0, 0.0, nan

0004, 2016-07-12T08:04:00.000000, 2870.0, 2871.0, 2870.0, 2871.0, 248.0, 0.0, nan

0005, 2016-07-12T08:05:00.000000, 2870.0, 2871.0, 2870.0, 2871.0, 234.0, 0.0, 2871.0

...

...

0639, 2016-07-12T18:39:00.000000, 2932.0, 2933.0, 2932.0, 2932.0, 1108.0, 0.0, 2932.8

0640, 2016-07-12T18:40:00.000000, 2931.0, 2932.0, 2931.0, 2931.0, 65.0, 0.0, 2932.6

***** DATA NOTIF: LIVE

0641, 2016-07-12T18:41:00.000000, 2932.0, 2932.0, 2930.0, 2930.0, 2093.0, 0.0, 2931.8

***** STORE NOTIF: (u'VisualChart is Disconnected', -65520)

***** DATA NOTIF: CONNBROKEN

***** STORE NOTIF: (u'VisualChart is Connected', -65521)

***** DATA NOTIF: CONNECTED

***** DATA NOTIF: DELAYED

0642, 2016-07-12T18:42:00.000000, 2931.0, 2931.0, 2931.0, 2931.0, 137.0, 0.0, 2931.2

0643, 2016-07-12T18:43:00.000000, 2931.0, 2931.0, 2931.0, 2931.0, 432.0, 0.0, 2931.0

...

0658, 2016-07-12T18:58:00.000000, 2929.0, 2929.0, 2929.0, 2929.0, 4.0, 0.0, 2930.0

0659, 2016-07-12T18:59:00.000000, 2929.0, 2930.0, 2929.0, 2930.0, 353.0, 0.0, 2930.0

***** DATA NOTIF: LIVE

0660, 2016-07-12T19:00:00.000000, 2930.0, 2930.0, 2930.0, 2930.0, 376.0, 0.0, 2930.0

0661, 2016-07-12T19:01:00.000000, 2929.0, 2930.0, 2929.0, 2930.0, 35.0, 0.0, 2929.8

Note

The execution environment has pytz installed

Note

Notice the absence of --resample: for Minutes the resampling

is built-in Visual Chart

And finally some trading, buying 2 contract of 015ES with a single

Market order and selling them in 2 orders of 1 contract each.

Execution:

$ ./vctest.py --data0 015ES --timeframe Minutes --compression 1 --fromdate 2016-07-12 2>&1 --broker --account accname --trade --stake 2

The output is rather verbose, showing all parts of the order exeuction. Summarising a bit:

--------------------------------------------------

Strategy Created

--------------------------------------------------

Datetime, Open, High, Low, Close, Volume, OpenInterest, SMA

***** DATA NOTIF: CONNECTED

***** DATA NOTIF: DELAYED

0001, 2016-07-12T08:01:00.000000, 2871.0, 2872.0, 2869.0, 2872.0, 1915.0, 0.0, nan

...

0709, 2016-07-12T19:50:00.000000, 2929.0, 2930.0, 2929.0, 2930.0, 11.0, 0.0, 2930.4

***** DATA NOTIF: LIVE

0710, 2016-07-12T19:51:00.000000, 2930.0, 2930.0, 2929.0, 2929.0, 134.0, 0.0, 2930.0

-------------------------------------------------- ORDER BEGIN 2016-07-12 19:52:01.629000

Ref: 1

OrdType: 0

OrdType: Buy

Status: 1

Status: Submitted

Size: 2

Price: None

Price Limit: None

ExecType: 0

ExecType: Market

CommInfo: <backtrader.brokers.vcbroker.VCCommInfo object at 0x000000001100CE10>

End of Session: 736157.916655

Info: AutoOrderedDict()

Broker: <backtrader.brokers.vcbroker.VCBroker object at 0x000000000475D400>

Alive: True

-------------------------------------------------- ORDER END

-------------------------------------------------- ORDER BEGIN 2016-07-12 19:52:01.629000

Ref: 1

OrdType: 0

OrdType: Buy

Status: 2

Status: Accepted

Size: 2

Price: None

Price Limit: None

ExecType: 0

ExecType: Market

CommInfo: <backtrader.brokers.vcbroker.VCCommInfo object at 0x000000001100CE10>

End of Session: 736157.916655

Info: AutoOrderedDict()

Broker: None

Alive: True

-------------------------------------------------- ORDER END

-------------------------------------------------- ORDER BEGIN 2016-07-12 19:52:01.629000

Ref: 1

OrdType: 0

OrdType: Buy

Status: 4

Status: Completed

Size: 2

Price: None

Price Limit: None

ExecType: 0

ExecType: Market

CommInfo: <backtrader.brokers.vcbroker.VCCommInfo object at 0x000000001100CE10>

End of Session: 736157.916655

Info: AutoOrderedDict()

Broker: None

Alive: False

-------------------------------------------------- ORDER END

-------------------------------------------------- TRADE BEGIN 2016-07-12 19:52:01.629000

ref:1

data:<backtrader.feeds.vcdata.VCData object at 0x000000000475D9E8>

tradeid:0

size:2.0

price:2930.0

value:5860.0

commission:0.0

pnl:0.0

pnlcomm:0.0

justopened:True

isopen:True

isclosed:0

baropen:710

dtopen:736157.74375

barclose:0

dtclose:0.0

barlen:0

historyon:False

history:[]

status:1

-------------------------------------------------- TRADE END

...

The following happens:

-

Data is received as normal

-

A

BUYfor2with execution typeMarketis issued-

SubmittedandAcceptednotifications are received (onlySubmittedis shown above) -

A streak of

Partialexecutions (only 1 shown) untilCompletedis received.

The actual execution is not shown, but is available in the

orderinstance received underorder.executed -

-

Although not shown, 2 x

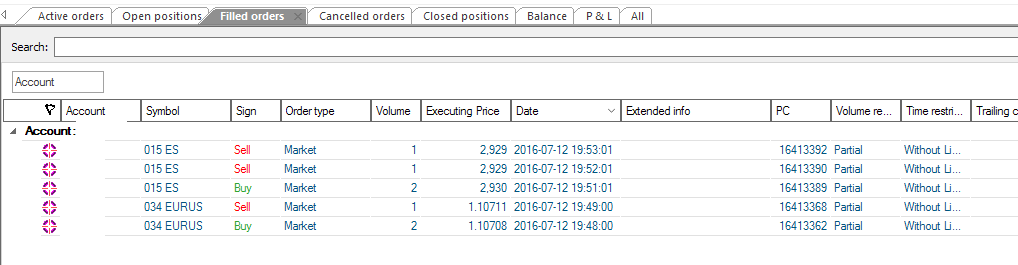

MarketSELLorders are issued to undo the operationThe screenshot shows the logs in Visual Chart after two different runs across an evening with

015ES(EuroStoxx 50) and034EURUS(EUR.USD Forex Pair)

The sample can do much more and is intended as a thorough test of the facilities and if possible to uncover any rough edges.

The usage:

$ ./vctest.py --help

usage: vctest.py [-h] [--exactbars EXACTBARS] [--plot] [--stopafter STOPAFTER]

[--nostore] [--qcheck QCHECK] [--no-timeoffset] --data0 DATA0

[--tradename TRADENAME] [--data1 DATA1] [--timezone TIMEZONE]

[--no-backfill_start] [--latethrough] [--historical]

[--fromdate FROMDATE] [--todate TODATE]

[--smaperiod SMAPERIOD] [--replay | --resample]

[--timeframe {Ticks,MicroSeconds,Seconds,Minutes,Days,Weeks,Months,Years}]

[--compression COMPRESSION] [--no-bar2edge] [--no-adjbartime]

[--no-rightedge] [--broker] [--account ACCOUNT] [--trade]

[--donotsell]

[--exectype {Market,Close,Limit,Stop,StopLimit}]

[--price PRICE] [--pstoplimit PSTOPLIMIT] [--stake STAKE]

[--valid VALID] [--cancel CANCEL]

Test Visual Chart 6 integration

optional arguments:

-h, --help show this help message and exit

--exactbars EXACTBARS

exactbars level, use 0/-1/-2 to enable plotting

(default: 1)

--plot Plot if possible (default: False)

--stopafter STOPAFTER

Stop after x lines of LIVE data (default: 0)

--nostore Do not Use the store pattern (default: False)

--qcheck QCHECK Timeout for periodic notification/resampling/replaying

check (default: 0.5)

--no-timeoffset Do not Use TWS/System time offset for non timestamped

prices and to align resampling (default: False)

--data0 DATA0 data 0 into the system (default: None)

--tradename TRADENAME

Actual Trading Name of the asset (default: None)

--data1 DATA1 data 1 into the system (default: None)

--timezone TIMEZONE timezone to get time output into (pytz names)

(default: None)

--historical do only historical download (default: False)

--fromdate FROMDATE Starting date for historical download with format:

YYYY-MM-DD[THH:MM:SS] (default: None)

--todate TODATE End date for historical download with format: YYYY-MM-

DD[THH:MM:SS] (default: None)

--smaperiod SMAPERIOD

Period to apply to the Simple Moving Average (default:

5)

--replay replay to chosen timeframe (default: False)

--resample resample to chosen timeframe (default: False)

--timeframe {Ticks,MicroSeconds,Seconds,Minutes,Days,Weeks,Months,Years}

TimeFrame for Resample/Replay (default: Ticks)

--compression COMPRESSION

Compression for Resample/Replay (default: 1)

--no-bar2edge no bar2edge for resample/replay (default: False)

--no-adjbartime no adjbartime for resample/replay (default: False)

--no-rightedge no rightedge for resample/replay (default: False)

--broker Use VisualChart as broker (default: False)

--account ACCOUNT Choose broker account (else first) (default: None)

--trade Do Sample Buy/Sell operations (default: False)

--donotsell Do not sell after a buy (default: False)

--exectype {Market,Close,Limit,Stop,StopLimit}

Execution to Use when opening position (default:

Market)

--price PRICE Price in Limit orders or Stop Trigger Price (default:

None)

--pstoplimit PSTOPLIMIT

Price for the limit in StopLimit (default: None)

--stake STAKE Stake to use in buy operations (default: 10)

--valid VALID Seconds or YYYY-MM-DD (default: None)

--cancel CANCEL Cancel a buy order after n bars in operation, to be

combined with orders like Limit (default: 0)

The code:

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

# The above could be sent to an independent module

import backtrader as bt

from backtrader.utils import flushfile # win32 quick stdout flushing

from backtrader.utils.py3 import string_types

class TestStrategy(bt.Strategy):

params = dict(

smaperiod=5,

trade=False,

stake=10,

exectype=bt.Order.Market,

stopafter=0,

valid=None,

cancel=0,

donotsell=False,

price=None,

pstoplimit=None,

)

def __init__(self):

# To control operation entries

self.orderid = list()

self.order = None

self.counttostop = 0

self.datastatus = 0

# Create SMA on 2nd data

self.sma = bt.indicators.MovAv.SMA(self.data, period=self.p.smaperiod)

print('--------------------------------------------------')

print('Strategy Created')

print('--------------------------------------------------')

def notify_data(self, data, status, *args, **kwargs):

print('*' * 5, 'DATA NOTIF:', data._getstatusname(status), *args)

if status == data.LIVE:

self.counttostop = self.p.stopafter

self.datastatus = 1

def notify_store(self, msg, *args, **kwargs):

print('*' * 5, 'STORE NOTIF:', msg)

def notify_order(self, order):

if order.status in [order.Completed, order.Cancelled, order.Rejected]:

self.order = None

print('-' * 50, 'ORDER BEGIN', datetime.datetime.now())

print(order)

print('-' * 50, 'ORDER END')

def notify_trade(self, trade):

print('-' * 50, 'TRADE BEGIN', datetime.datetime.now())

print(trade)

print('-' * 50, 'TRADE END')

def prenext(self):

self.next(frompre=True)

def next(self, frompre=False):

txt = list()

txt.append('%04d' % len(self))

dtfmt = '%Y-%m-%dT%H:%M:%S.%f'

txt.append('%s' % self.data.datetime.datetime(0).strftime(dtfmt))

txt.append('{}'.format(self.data.open[0]))

txt.append('{}'.format(self.data.high[0]))

txt.append('{}'.format(self.data.low[0]))

txt.append('{}'.format(self.data.close[0]))

txt.append('{}'.format(self.data.volume[0]))

txt.append('{}'.format(self.data.openinterest[0]))

txt.append('{}'.format(self.sma[0]))

print(', '.join(txt))

if len(self.datas) > 1:

txt = list()

txt.append('%04d' % len(self))

dtfmt = '%Y-%m-%dT%H:%M:%S.%f'

txt.append('%s' % self.data1.datetime.datetime(0).strftime(dtfmt))

txt.append('{}'.format(self.data1.open[0]))

txt.append('{}'.format(self.data1.high[0]))

txt.append('{}'.format(self.data1.low[0]))

txt.append('{}'.format(self.data1.close[0]))

txt.append('{}'.format(self.data1.volume[0]))

txt.append('{}'.format(self.data1.openinterest[0]))

txt.append('{}'.format(float('NaN')))

print(', '.join(txt))

if self.counttostop: # stop after x live lines

self.counttostop -= 1

if not self.counttostop:

self.env.runstop()

return

if not self.p.trade:

return

# if True and len(self.orderid) < 1:

if self.datastatus and not self.position and len(self.orderid) < 1:

self.order = self.buy(size=self.p.stake,

exectype=self.p.exectype,

price=self.p.price,

plimit=self.p.pstoplimit,

valid=self.p.valid)

self.orderid.append(self.order)

elif self.position.size > 0 and not self.p.donotsell:

if self.order is None:

size = self.p.stake // 2

if not size:

size = self.position.size # use the remaining

self.order = self.sell(size=size, exectype=bt.Order.Market)

elif self.order is not None and self.p.cancel:

if self.datastatus > self.p.cancel:

self.cancel(self.order)

if self.datastatus:

self.datastatus += 1

def start(self):

header = ['Datetime', 'Open', 'High', 'Low', 'Close', 'Volume',

'OpenInterest', 'SMA']

print(', '.join(header))

self.done = False

def runstrategy():

args = parse_args()

# Create a cerebro

cerebro = bt.Cerebro()

storekwargs = dict()

if not args.nostore:

vcstore = bt.stores.VCStore(**storekwargs)

if args.broker:

brokerargs = dict(account=args.account, **storekwargs)

if not args.nostore:

broker = vcstore.getbroker(**brokerargs)

else:

broker = bt.brokers.VCBroker(**brokerargs)

cerebro.setbroker(broker)

timeframe = bt.TimeFrame.TFrame(args.timeframe)

if args.resample or args.replay:

datatf = bt.TimeFrame.Ticks

datacomp = 1

else:

datatf = timeframe

datacomp = args.compression

fromdate = None

if args.fromdate:

dtformat = '%Y-%m-%d' + ('T%H:%M:%S' * ('T' in args.fromdate))

fromdate = datetime.datetime.strptime(args.fromdate, dtformat)

todate = None

if args.todate:

dtformat = '%Y-%m-%d' + ('T%H:%M:%S' * ('T' in args.todate))

todate = datetime.datetime.strptime(args.todate, dtformat)

VCDataFactory = vcstore.getdata if not args.nostore else bt.feeds.VCData

datakwargs = dict(

timeframe=datatf, compression=datacomp,

fromdate=fromdate, todate=todate,

historical=args.historical,

qcheck=args.qcheck,

tz=args.timezone

)

if args.nostore and not args.broker: # neither store nor broker

datakwargs.update(storekwargs) # pass the store args over the data

data0 = VCDataFactory(dataname=args.data0, tradename=args.tradename,

**datakwargs)

data1 = None

if args.data1 is not None:

data1 = VCDataFactory(dataname=args.data1, **datakwargs)

rekwargs = dict(

timeframe=timeframe, compression=args.compression,

bar2edge=not args.no_bar2edge,

adjbartime=not args.no_adjbartime,

rightedge=not args.no_rightedge,

)

if args.replay:

cerebro.replaydata(dataname=data0, **rekwargs)

if data1 is not None:

cerebro.replaydata(dataname=data1, **rekwargs)

elif args.resample:

cerebro.resampledata(dataname=data0, **rekwargs)

if data1 is not None:

cerebro.resampledata(dataname=data1, **rekwargs)

else:

cerebro.adddata(data0)

if data1 is not None:

cerebro.adddata(data1)

if args.valid is None:

valid = None

else:

try:

valid = float(args.valid)

except:

dtformat = '%Y-%m-%d' + ('T%H:%M:%S' * ('T' in args.valid))

valid = datetime.datetime.strptime(args.valid, dtformat)

else:

valid = datetime.timedelta(seconds=args.valid)

# Add the strategy

cerebro.addstrategy(TestStrategy,

smaperiod=args.smaperiod,

trade=args.trade,

exectype=bt.Order.ExecType(args.exectype),

stake=args.stake,

stopafter=args.stopafter,

valid=valid,

cancel=args.cancel,

donotsell=args.donotsell,

price=args.price,

pstoplimit=args.pstoplimit)

# Live data ... avoid long data accumulation by switching to "exactbars"

cerebro.run(exactbars=args.exactbars)

if args.plot and args.exactbars < 1: # plot if possible

cerebro.plot()

def parse_args():

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description='Test Visual Chart 6 integration')

parser.add_argument('--exactbars', default=1, type=int,

required=False, action='store',

help='exactbars level, use 0/-1/-2 to enable plotting')

parser.add_argument('--plot',

required=False, action='store_true',

help='Plot if possible')

parser.add_argument('--stopafter', default=0, type=int,

required=False, action='store',

help='Stop after x lines of LIVE data')

parser.add_argument('--nostore',

required=False, action='store_true',

help='Do not Use the store pattern')

parser.add_argument('--qcheck', default=0.5, type=float,

required=False, action='store',

help=('Timeout for periodic '

'notification/resampling/replaying check'))

parser.add_argument('--no-timeoffset',

required=False, action='store_true',

help=('Do not Use TWS/System time offset for non '

'timestamped prices and to align resampling'))

parser.add_argument('--data0', default=None,

required=True, action='store',

help='data 0 into the system')

parser.add_argument('--tradename', default=None,

required=False, action='store',

help='Actual Trading Name of the asset')

parser.add_argument('--data1', default=None,

required=False, action='store',

help='data 1 into the system')

parser.add_argument('--timezone', default=None,

required=False, action='store',

help='timezone to get time output into (pytz names)')

parser.add_argument('--historical',

required=False, action='store_true',

help='do only historical download')

parser.add_argument('--fromdate',

required=False, action='store',

help=('Starting date for historical download '

'with format: YYYY-MM-DD[THH:MM:SS]'))

parser.add_argument('--todate',

required=False, action='store',

help=('End date for historical download '

'with format: YYYY-MM-DD[THH:MM:SS]'))

parser.add_argument('--smaperiod', default=5, type=int,

required=False, action='store',

help='Period to apply to the Simple Moving Average')

pgroup = parser.add_mutually_exclusive_group(required=False)

pgroup.add_argument('--replay',

required=False, action='store_true',

help='replay to chosen timeframe')

pgroup.add_argument('--resample',

required=False, action='store_true',

help='resample to chosen timeframe')

parser.add_argument('--timeframe', default=bt.TimeFrame.Names[0],

choices=bt.TimeFrame.Names,

required=False, action='store',

help='TimeFrame for Resample/Replay')

parser.add_argument('--compression', default=1, type=int,

required=False, action='store',

help='Compression for Resample/Replay')

parser.add_argument('--no-bar2edge',

required=False, action='store_true',

help='no bar2edge for resample/replay')

parser.add_argument('--no-adjbartime',

required=False, action='store_true',

help='no adjbartime for resample/replay')

parser.add_argument('--no-rightedge',

required=False, action='store_true',

help='no rightedge for resample/replay')

parser.add_argument('--broker',

required=False, action='store_true',

help='Use VisualChart as broker')

parser.add_argument('--account', default=None,

required=False, action='store',

help='Choose broker account (else first)')

parser.add_argument('--trade',

required=False, action='store_true',

help='Do Sample Buy/Sell operations')

parser.add_argument('--donotsell',

required=False, action='store_true',

help='Do not sell after a buy')

parser.add_argument('--exectype', default=bt.Order.ExecTypes[0],

choices=bt.Order.ExecTypes,

required=False, action='store',

help='Execution to Use when opening position')

parser.add_argument('--price', default=None, type=float,

required=False, action='store',

help='Price in Limit orders or Stop Trigger Price')

parser.add_argument('--pstoplimit', default=None, type=float,

required=False, action='store',

help='Price for the limit in StopLimit')

parser.add_argument('--stake', default=10, type=int,

required=False, action='store',

help='Stake to use in buy operations')

parser.add_argument('--valid', default=None,

required=False, action='store',

help='Seconds or YYYY-MM-DD')

parser.add_argument('--cancel', default=0, type=int,

required=False, action='store',

help=('Cancel a buy order after n bars in operation,'

' to be combined with orders like Limit'))

return parser.parse_args()

if __name__ == '__main__':

runstrategy()