Release 1.9.51.121

Even being a minor release, there are some interesting things which probably grant having a dedicated blog post for them.

linealias

Pull-Request #320 included

the indicator RelativeMomentumIndex (or RMI) which according to the

literature is an evolution of the RSI, which:

- Considers up and down periods with a lookback larger than

1

As such and rather than having an indicator repeating most of what the RSI

does, it seemed useful to do two things:

-

Extend

RSI(and sub-indicators likeUpDayandDownDayto support a lookback period larger than 1.RMIcan then be implemented as a subclass which simply has some different default values. -

The logical name for the line of the

RMIindicator isrmi, but theRSIalready has decided the name asrsi. This is solved by adding a new functionality namedlinealias

The RMI implementation it looks like this:

class RelativeMomentumIndex(RSI):

alias = ('RMI', )

linealias = (('rsi', 'rmi',),) # add an alias for this class rmi -> rsi

plotlines = dict(rsi=dict(_name='rmi')) # change line plotting name

An alias for the line rsi from the base class is added, with the name

rmi. If someone wanted to make a subclass and use the name rmi it would

now be possible.

Additionally, the plotting name of the rsi line is also changed to

rmi. An alternative implementation was possible:

class RelativeMomentumIndex(RSI):

alias = ('RMI', )

linesoverrride = True # allow redefinition of the lines hierarcy

lines = ('rmi',) # define the line

linealias = (('rmi', 'rsi',),) # add an alias for base class rsi -> rmi

Here the existing hierarchy from RSI is no longer considered and lines

is used to define the only line named rmi. There is no need to define the

plotting name, because the only line has now the expected name.

But the base class would fail to fill in the values, because it is expecting a

line with the name rsi to be in place. Hence the addition of a reverse

alias to let it find the line.

Interactive Brokers for Optimization

Using a live connection to Interactive Brokers as the data source for

optimization was not foreseen. Yet a user tried it and pacing violations

started being met. The reason being that the Interactive Brokers data feed

marks itself as being a live feed, allowing the system to bypass some things

like for example data preloading.

With no preloading, each instance of the optimization would retry to

re-download the same historical data from Interactive Brokers. With this in

mind it’s obvious that the feed could look to see if the user has requested

just a historical download and in this case not report itself as live,

allowing the platform to preload the data and share it amongst optimization instances.

See the community thread. Optimizing with IBStore causes redundant connections/downloads

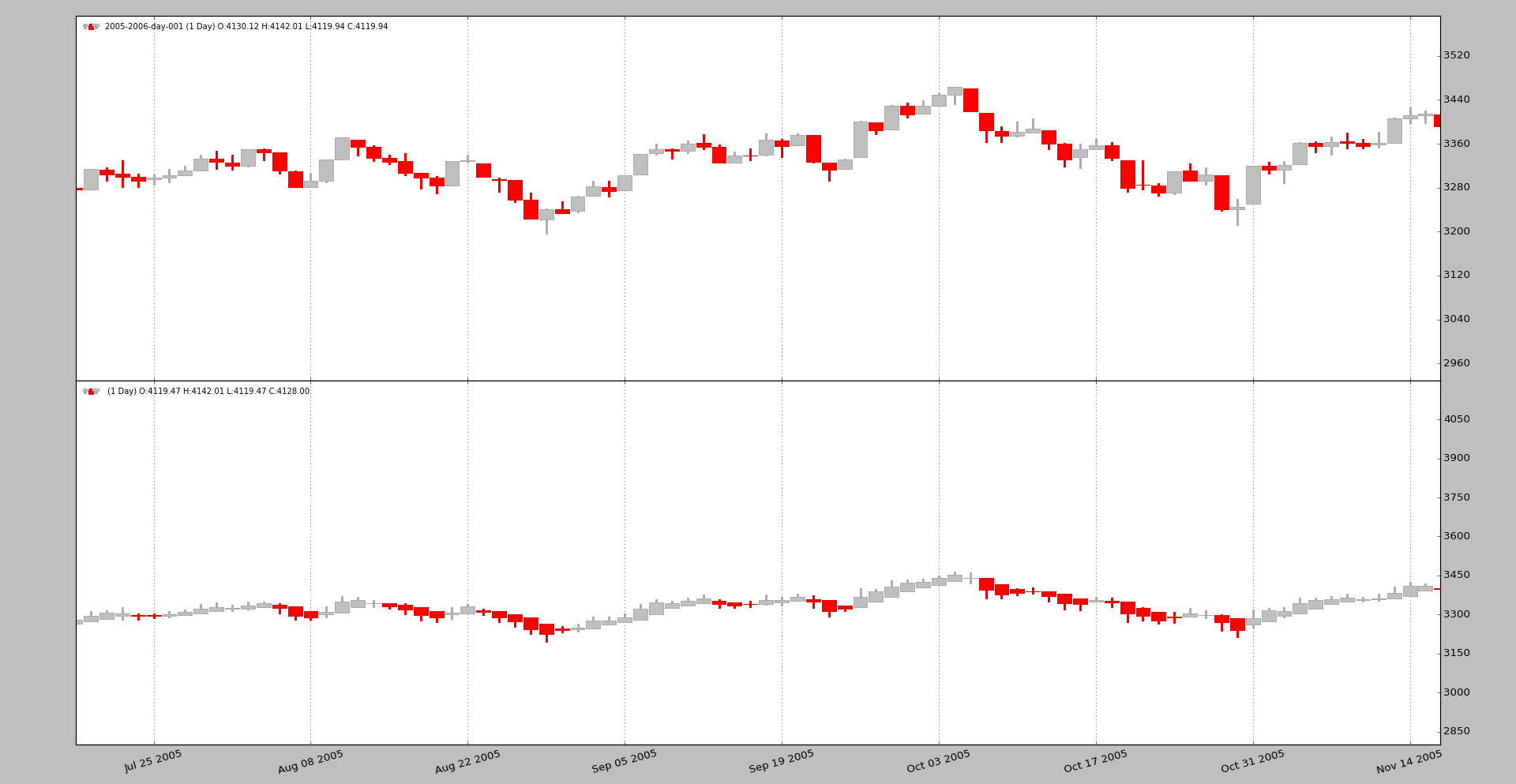

Heikin-Ashi Candlesticks

This other community thread was looking to develop the Heikin-Ashi

candlesticks as an indicator: Develop Heikinashi Indicators,

facing some problems with the recursive definition, because a seed value is

needed, which can be done during the prenext phase of the indicator.

Being an interesting display alternative to the traditional candlesticks, this has been implemented as a filter, which allows to modify the data source to really deliver Heikin-Ashi candlesticks. Just like this:

data0 = MyDataFeed(dataname='xxx', timeframe=bt.TimeFrame.Days, compression=1)

data0.addfilter(bt.filters.HeikinAshi)

cerebro.adddata(data0)

A comparison between the candles can quickly be made by anyone with this code:

data0 = MyDataFeed(dataname='xxx', timeframe=bt.TimeFrame.Days, compression=1)

cerebro.adddata(data0)

data1 = data0.clone()

data1.addfilter(bt.filters.HeikinAshi)

cerebro.adddata(data1)

To plot candles, remember to do:

cerebro.plot(style='candle')

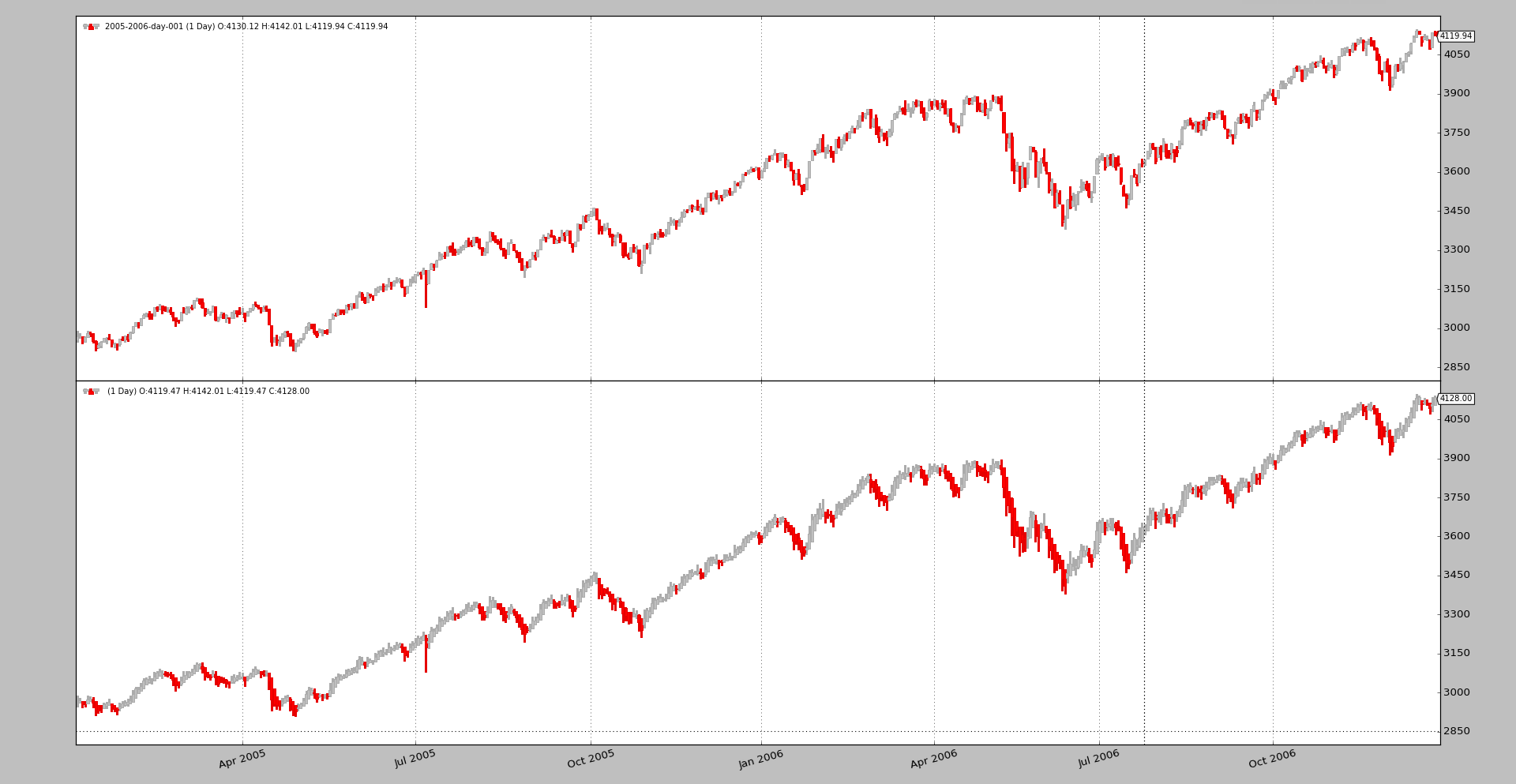

Using the sample daily data for 2005 and 2006 in the sources.

And zooming in a bit to better appreciate the differences

Allowing re-scaling of the y-axis by secondary actors

The axisfor data feeds have always used the main data feed as the

scale-owner, because the data is always the most important part of the view. If

we consider for example the BollingerBands, it could be that the top band

would be far away from the maximum of the data and allowing this band to

re-scale the chart, would reduce the size occupied by the data in the chart,

which wouldn’t be wished.

The behavior can be controlled now with plotylimited as in:

...

data0 = MyDataFeed(dataname='xxx', timeframe=bt.TimeFrame.Days, compression=1)

data0.plotinfo.plotlog = False # allow other actors to resize the axis

...

In the following chart the data feed at the bottom is plotted with

plotylimited=False. The BollingerBands don’t get off the chart, because

they contribute to the scaling and everything fits in the chart.

This was also commented in the community. How max - min plot boundaries are set?

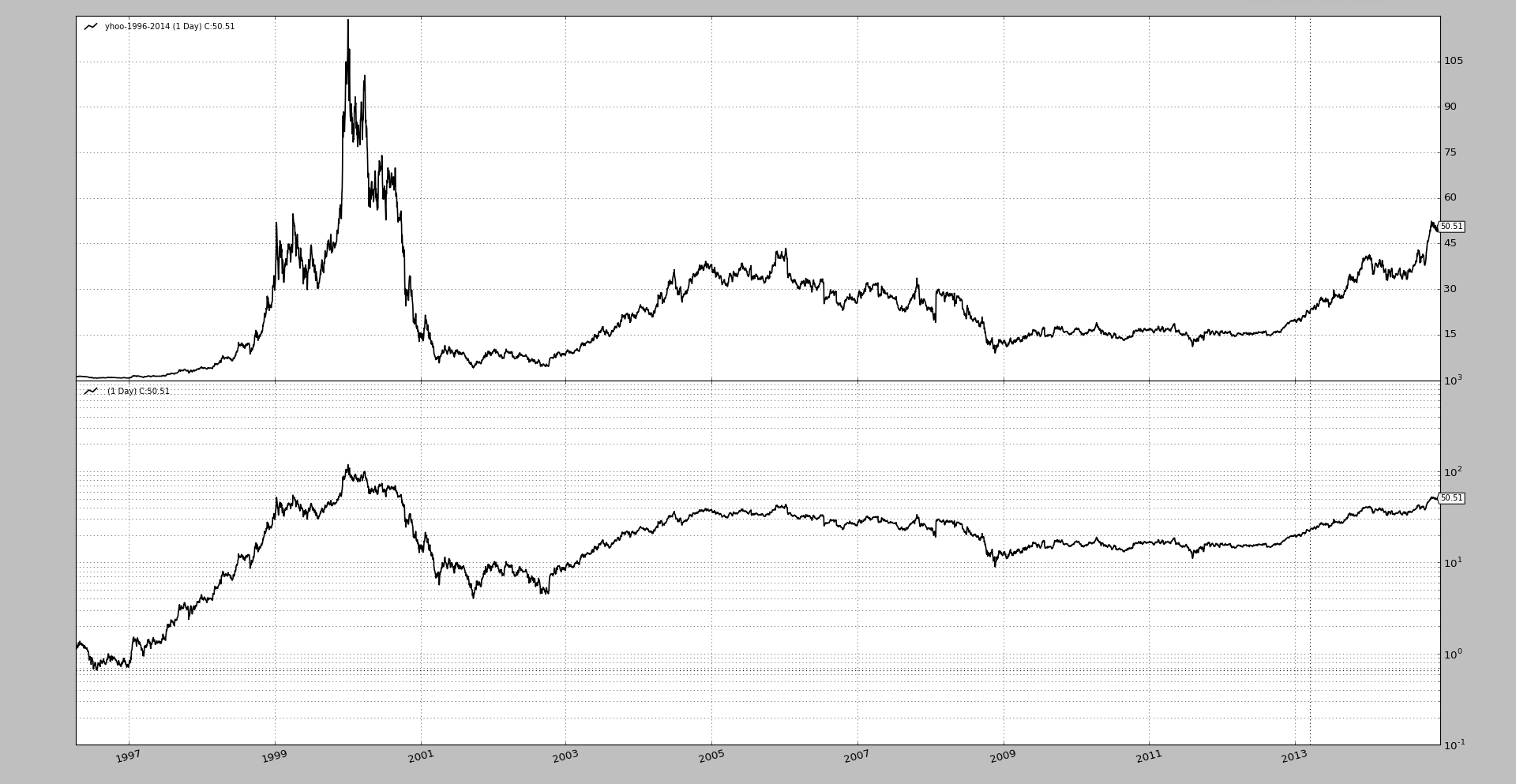

Semilogarithmic Plot (aka Logarithmic)

Individual axis can now be plotted with a semilogarithmic scale (the y-scale). For example with:

...

data0 = MyDataFeed(dataname='xxx', timeframe=bt.TimeFrame.Days, compression=1)

data0.plotinfo.plotlog = True

data0.plotinfo.plotylimited = True

cerebro.adddata(data0)

...

That means that the axis controlled by this data feed for plotting will use a logarithmic scale, but other won’t and therefore

-

A moving average plotted over the data will also be plotted with that scale

-

A stochastic (which is in a different axix and has a different scale) will still be plotted linearly

Note

Notice that plotylimited=True is used. This is to let

matplotlib calculate the limits of the logarithmic chart (because

the ticks are a power of 10) properly to fit things into the chart.

A sample simply comparing a long term period of Yahoo data.

Allow plotmaster to point to itself

Plotting several data feeds on the same axis was already possible, but a small

nuisance didn’t allow a clean loop to set the plotinfo.plotmaster

value. The following had to be done before:

mydatas = []

data = MyDataFeed(dataname=mytickers[0], timeframe=..., compression=...)

mydatafeeds.append(data)

for ticker in mytickers[1:]

data = MyDataFeed(dataname=ticker, timeframe=..., compression=...)

mydatafeeds.append(data)

data.plotinfo.plotmaster = mydatas[0]

And this cleaner loop is possible now:

mydatas = []

for ticker in mytickers:

data = MyDataFeed(dataname=ticker, timeframe=..., compression=...)

mydatafeeds.append(data)

data.plotinfo.plotmaster = mydatas[0]

And dnames got documented

Referencing the data feeds by names was already available, but it had skipped

making it to the documentation, so it was a hidden jewel. The dnames

attribute in the strategy supports dot-notation and [] notation (it is

actually a dict subclass). If we first add some data feeds:

mytickers = ['YHOO', 'IBM', 'AAPL']

for t in mytickers:

d = bt.feeds.YahooFinanceData(dataname=t, fromdate=..., name=t.lower())

Later in the strategy one can do the following:

def __init__(self):

yhoosma = bt.ind.SMA(self.dnames.yhoo, period=20)

aaplsma = bt.ind.SMA(self.dnames['aapl'], period=30)

# or even go over the keys/items/values like in a regular dict

# for example with a dictionary comprehension

stocs = {name: bt.ind.Stochastic(data) for name, data in self.dnames.items()}

Conclusion

A small release with small changes which adds some nifty features.