Rolling over Futures

Not every provider offers a continuous future for the instruments with which one can trade. Sometimes the data offered is that of the still valid expiration dates, i.e.: those still being traded

This is not so helpful when it comes to backtesting because the data is scattered over several different instruments which additionally … overlap in time.

Being able to properly join the data of those instruments, from the past, into a continuous stream alleviates the pain. The problem:

- There is no law as to how best join the different expiration dates into a continuous future

Some literature, courtesy of SierraChart at:

The RollOver Data Feed

backtrader has added with 1.8.10.99 the possibility to join futures’ data

from different expiration dates into a continuous future:

import backtrader as bt

cerebro = bt.Cerebro()

data0 = bt.feeds.MyFeed(dataname='Expiry0')

data1 = bt.feeds.MyFeed(dataname='Expiry1')

...

dataN = bt.feeds.MyFeed(dataname='ExpiryN')

drollover = cerebro.rolloverdata(data0, data1, ..., dataN, name='MyRoll', **kwargs)

cerebro.run()

Note

The possible **kwargs are explained below

It can also be done by directly accessing the RollOver feed (which is

helpful if subclassing is done):

import backtrader as bt

cerebro = bt.Cerebro()

data0 = bt.feeds.MyFeed(dataname='Expiry0')

data1 = bt.feeds.MyFeed(dataname='Expiry1')

...

dataN = bt.feeds.MyFeed(dataname='ExpiryN')

drollover = bt.feeds.RollOver(data0, data1, ..., dataN, dataname='MyRoll', **kwargs)

cerebro.adddata(drollover)

cerebro.run()

Note

The possible **kwargs are explained below

Note

When using RollOver the name is assigned using dataname. This

is the standard parameter used for all data feeds to pass the

name/ticker. In this case it is reused to assign a common name to

the complete set of rolled over futures.

In the case of cerebro.rolloverdata, the name is assigned to a

feed using name, which is already one named argument of that method

Bottomline:

-

Data Feeds are created as usual but ARE NOT added to

cerebro -

Those data feeds are given as input to

bt.feeds.RollOverA

datanameis also given, mostly for identification purposes. -

This roll over data feed is then added to

cerebro

Options for the Roll-Over

Two parameters are provided to control the roll-over process

-

checkdate(default:None)This must be a callable with the following signature:

checkdate(dt, d):Where:

-

dtis adatetime.datetimeobject -

dis the current data feed for the active future

Expected Return Values:

-

True: as long as the callable returns this, a switchover can happen to the next futureIf a commodity expires on the 3rd Friday of March,

checkdatecould returnTruefor the entire week in which the expiration takes place. -

False: the expiration cannot take place

-

-

checkcondition(default:None)Note

This will only be called if

checkdatehas returnedTrueIf

Nonethis will evaluate toTrue(execute roll over) internallyElse this must be a callable with this signature:

checkcondition(d0, d1)Where:

-

d0is the current data feed for the active future -

d1is the data feed for the next expiration

Expected Return Values:

-

True: roll-over to the next futureFollowing with the example from

checkdate, this could say that the roll-over can only happen if the volume fromd0is already less than the volume fromd1 -

False: the expiration cannot take place

-

Subclassing RollOver

If specifying the callables isn’t enough, there is always the chance to

subclass RollOver. The methods to subclass:

-

def _checkdate(self, dt, d):Which matches the signature of the parameter of the same name above. The expected return values are also the saame.

-

def _checkcondition(self, d0, d1)Which matches the signature of the parameter of the same name above. The expected return values are also the saame.

Let’s Roll

Note

The default behavior in the sample is to use

cerebro.rolloverdata. This can be changed by passing the

-no-cerebro flag. In this case the sample uses RollOver and

cerebro.adddata

The implementation includes a sample which is available in the backtrader sources.

Futures concatenation

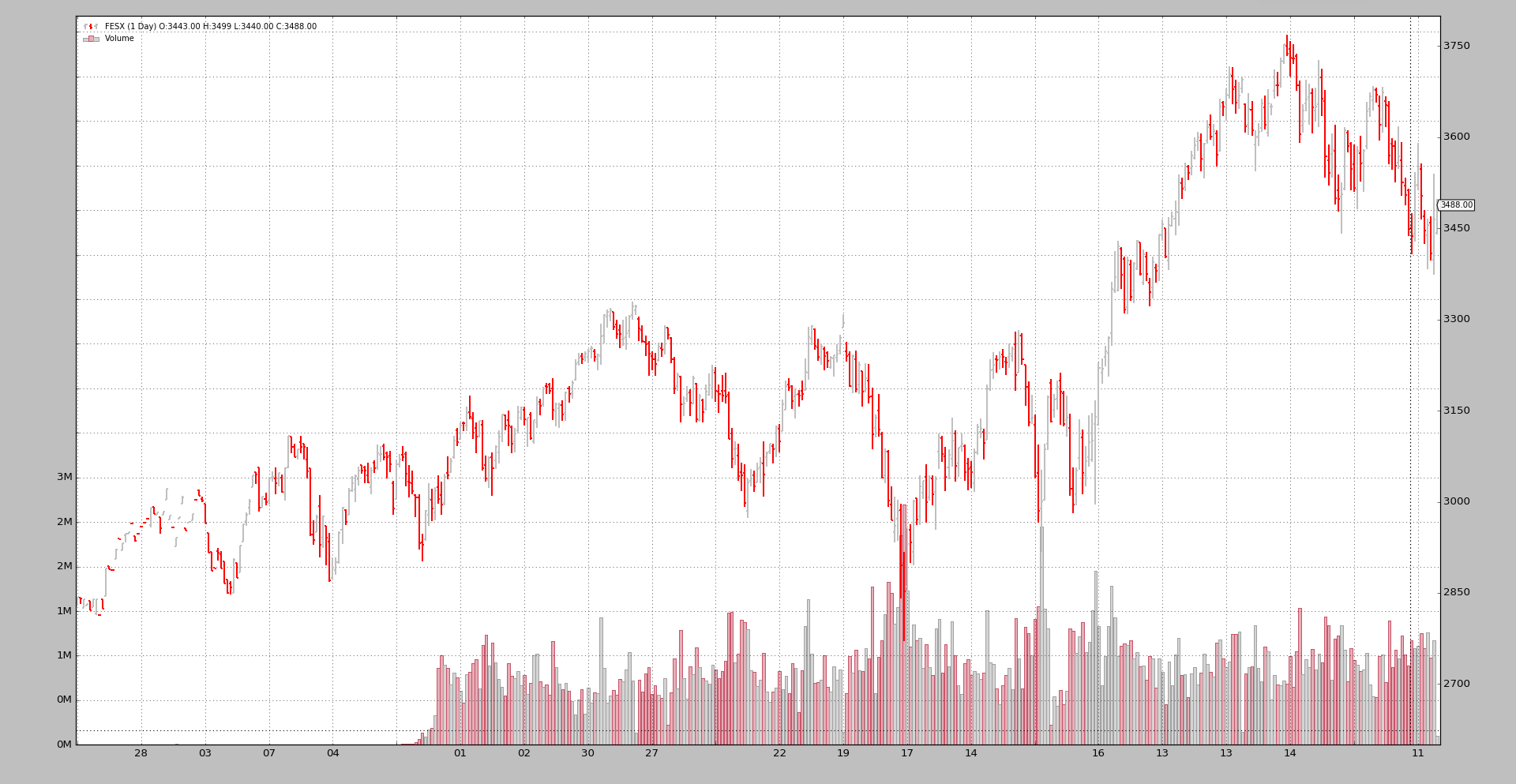

Let’s start by looking at a pure concatenation by running the sample with no arguments.

$ ./rollover.py

Len, Name, RollName, Datetime, WeekDay, Open, High, Low, Close, Volume, OpenInterest

0001, FESX, 199FESXM4, 2013-09-26, Thu, 2829.0, 2843.0, 2829.0, 2843.0, 3.0, 1000.0

0002, FESX, 199FESXM4, 2013-09-27, Fri, 2842.0, 2842.0, 2832.0, 2841.0, 16.0, 1101.0

...

0176, FESX, 199FESXM4, 2014-06-20, Fri, 3315.0, 3324.0, 3307.0, 3322.0, 134777.0, 520978.0

0177, FESX, 199FESXU4, 2014-06-23, Mon, 3301.0, 3305.0, 3265.0, 3285.0, 730211.0, 3003692.0

...

0241, FESX, 199FESXU4, 2014-09-19, Fri, 3287.0, 3308.0, 3286.0, 3294.0, 144692.0, 566249.0

0242, FESX, 199FESXZ4, 2014-09-22, Mon, 3248.0, 3263.0, 3231.0, 3240.0, 582077.0, 2976624.0

...

0306, FESX, 199FESXZ4, 2014-12-19, Fri, 3196.0, 3202.0, 3131.0, 3132.0, 226415.0, 677924.0

0307, FESX, 199FESXH5, 2014-12-22, Mon, 3151.0, 3177.0, 3139.0, 3168.0, 547095.0, 2952769.0

...

0366, FESX, 199FESXH5, 2015-03-20, Fri, 3680.0, 3698.0, 3672.0, 3695.0, 147632.0, 887205.0

0367, FESX, 199FESXM5, 2015-03-23, Mon, 3654.0, 3655.0, 3608.0, 3618.0, 802344.0, 3521988.0

...

0426, FESX, 199FESXM5, 2015-06-18, Thu, 3398.0, 3540.0, 3373.0, 3465.0, 1173246.0, 811805.0

0427, FESX, 199FESXM5, 2015-06-19, Fri, 3443.0, 3499.0, 3440.0, 3488.0, 104096.0, 516792.0

This uses cerebro.chaindata and the result should be clear:

-

Whenever a data feed is over the next one takes over

-

This happens always between a Friday and Monday: the futures in the samples always expire on Friday

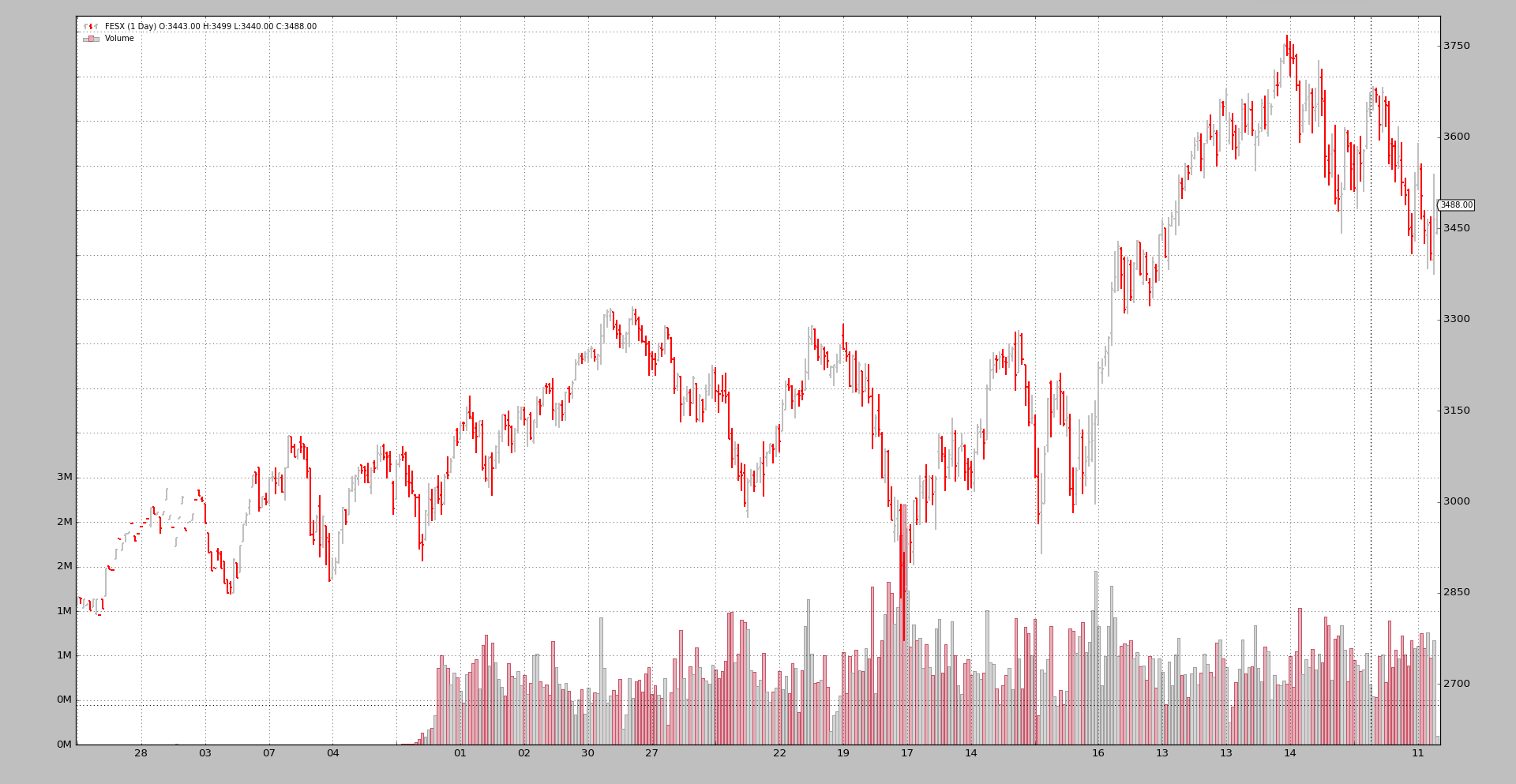

Futures roll-over with no checks

Let’s execute with --rollover

$ ./rollover.py --rollover --plot

Len, Name, RollName, Datetime, WeekDay, Open, High, Low, Close, Volume, OpenInterest

0001, FESX, 199FESXM4, 2013-09-26, Thu, 2829.0, 2843.0, 2829.0, 2843.0, 3.0, 1000.0

0002, FESX, 199FESXM4, 2013-09-27, Fri, 2842.0, 2842.0, 2832.0, 2841.0, 16.0, 1101.0

...

0176, FESX, 199FESXM4, 2014-06-20, Fri, 3315.0, 3324.0, 3307.0, 3322.0, 134777.0, 520978.0

0177, FESX, 199FESXU4, 2014-06-23, Mon, 3301.0, 3305.0, 3265.0, 3285.0, 730211.0, 3003692.0

...

0241, FESX, 199FESXU4, 2014-09-19, Fri, 3287.0, 3308.0, 3286.0, 3294.0, 144692.0, 566249.0

0242, FESX, 199FESXZ4, 2014-09-22, Mon, 3248.0, 3263.0, 3231.0, 3240.0, 582077.0, 2976624.0

...

0306, FESX, 199FESXZ4, 2014-12-19, Fri, 3196.0, 3202.0, 3131.0, 3132.0, 226415.0, 677924.0

0307, FESX, 199FESXH5, 2014-12-22, Mon, 3151.0, 3177.0, 3139.0, 3168.0, 547095.0, 2952769.0

...

0366, FESX, 199FESXH5, 2015-03-20, Fri, 3680.0, 3698.0, 3672.0, 3695.0, 147632.0, 887205.0

0367, FESX, 199FESXM5, 2015-03-23, Mon, 3654.0, 3655.0, 3608.0, 3618.0, 802344.0, 3521988.0

...

0426, FESX, 199FESXM5, 2015-06-18, Thu, 3398.0, 3540.0, 3373.0, 3465.0, 1173246.0, 811805.0

0427, FESX, 199FESXM5, 2015-06-19, Fri, 3443.0, 3499.0, 3440.0, 3488.0, 104096.0, 516792.0

The same behavior. It can clearly be seen that contract changes are being made on the 3rd Friday of either Mar, Jun, Sep, Dec.

But this is mostly WRONG. backtrader cannot know it, but the author knows that

the EuroStoxx 50 futures stop trading at 12:00 CET. So even if there is a

daily bar for the 3rd Friday of the expiration month, the change is happening

too late.

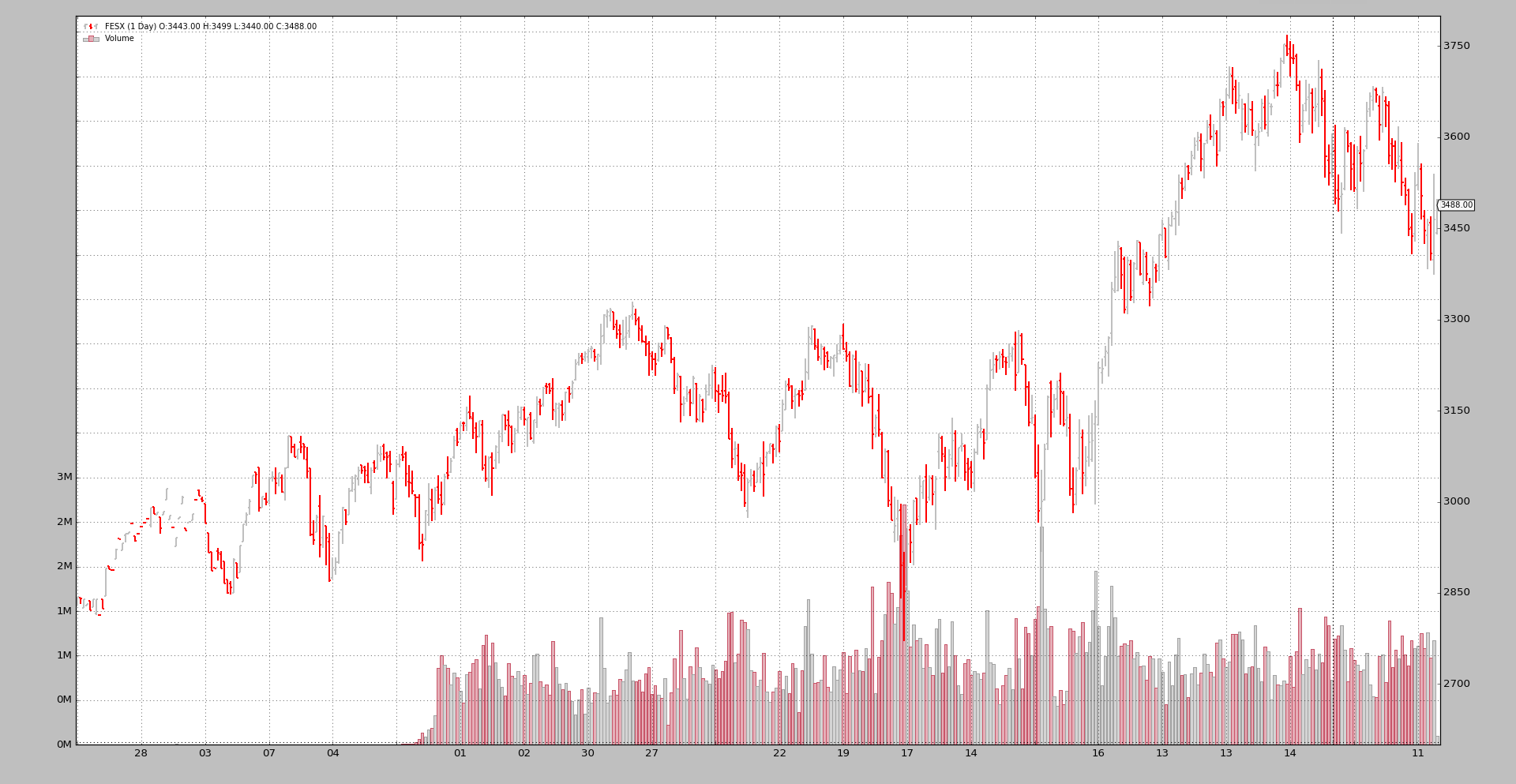

Changing during the Week

A checkdate callable is implemented in the sample, which calculates the date

of expiration for the currently active contract.

checkdate will allow a roll over as soon as the week of the 3rd Friday of

the month is reached (it may be Tuesday if for example Monday is a bank holiday)

$ ./rollover.py --rollover --checkdate --plot

Len, Name, RollName, Datetime, WeekDay, Open, High, Low, Close, Volume, OpenInterest

0001, FESX, 199FESXM4, 2013-09-26, Thu, 2829.0, 2843.0, 2829.0, 2843.0, 3.0, 1000.0

0002, FESX, 199FESXM4, 2013-09-27, Fri, 2842.0, 2842.0, 2832.0, 2841.0, 16.0, 1101.0

...

0171, FESX, 199FESXM4, 2014-06-13, Fri, 3283.0, 3292.0, 3253.0, 3276.0, 734907.0, 2715357.0

0172, FESX, 199FESXU4, 2014-06-16, Mon, 3261.0, 3275.0, 3252.0, 3262.0, 180608.0, 844486.0

...

0236, FESX, 199FESXU4, 2014-09-12, Fri, 3245.0, 3247.0, 3220.0, 3232.0, 650314.0, 2726874.0

0237, FESX, 199FESXZ4, 2014-09-15, Mon, 3209.0, 3224.0, 3203.0, 3221.0, 153448.0, 983793.0

...

0301, FESX, 199FESXZ4, 2014-12-12, Fri, 3127.0, 3143.0, 3038.0, 3042.0, 1409834.0, 2934179.0

0302, FESX, 199FESXH5, 2014-12-15, Mon, 3041.0, 3089.0, 2963.0, 2980.0, 329896.0, 904053.0

...

0361, FESX, 199FESXH5, 2015-03-13, Fri, 3657.0, 3680.0, 3627.0, 3670.0, 867678.0, 3499116.0

0362, FESX, 199FESXM5, 2015-03-16, Mon, 3594.0, 3641.0, 3588.0, 3629.0, 250445.0, 1056099.0

...

0426, FESX, 199FESXM5, 2015-06-18, Thu, 3398.0, 3540.0, 3373.0, 3465.0, 1173246.0, 811805.0

0427, FESX, 199FESXM5, 2015-06-19, Fri, 3443.0, 3499.0, 3440.0, 3488.0, 104096.0, 516792.0

Much better. The roll over is now happening 5 days before. A quick visual inspection of the Len indices show it. For example:

199FESXM4to199FESXU4happens at len171-172. Withoutcheckdateit happened at176-177

The roll over is happening on the Monday before the 3rd Friday of the expiration month.

Adding a volume condition

Even with the improvement, the situation can be further improved in that not only the date but also de negotiated volume will be taken into account. Do switch when the new contract trades more volume than the currently active one.

Let’s add a checkcondition to the mix and run.

$ ./rollover.py --rollover --checkdate --checkcondition --plot

Len, Name, RollName, Datetime, WeekDay, Open, High, Low, Close, Volume, OpenInterest

0001, FESX, 199FESXM4, 2013-09-26, Thu, 2829.0, 2843.0, 2829.0, 2843.0, 3.0, 1000.0

0002, FESX, 199FESXM4, 2013-09-27, Fri, 2842.0, 2842.0, 2832.0, 2841.0, 16.0, 1101.0

...

0175, FESX, 199FESXM4, 2014-06-19, Thu, 3307.0, 3330.0, 3300.0, 3321.0, 717979.0, 759122.0

0176, FESX, 199FESXU4, 2014-06-20, Fri, 3309.0, 3318.0, 3290.0, 3298.0, 711627.0, 2957641.0

...

0240, FESX, 199FESXU4, 2014-09-18, Thu, 3249.0, 3275.0, 3243.0, 3270.0, 846600.0, 803202.0

0241, FESX, 199FESXZ4, 2014-09-19, Fri, 3273.0, 3293.0, 3250.0, 3252.0, 1042294.0, 3021305.0

...

0305, FESX, 199FESXZ4, 2014-12-18, Thu, 3095.0, 3175.0, 3085.0, 3172.0, 1309574.0, 889112.0

0306, FESX, 199FESXH5, 2014-12-19, Fri, 3195.0, 3200.0, 3106.0, 3147.0, 1329040.0, 2964538.0

...

0365, FESX, 199FESXH5, 2015-03-19, Thu, 3661.0, 3691.0, 3646.0, 3668.0, 1271122.0, 1054639.0

0366, FESX, 199FESXM5, 2015-03-20, Fri, 3607.0, 3664.0, 3595.0, 3646.0, 1182235.0, 3407004.0

...

0426, FESX, 199FESXM5, 2015-06-18, Thu, 3398.0, 3540.0, 3373.0, 3465.0, 1173246.0, 811805.0

0427, FESX, 199FESXM5, 2015-06-19, Fri, 3443.0, 3499.0, 3440.0, 3488.0, 104096.0, 516792.0

Even better. We have moved the switch date to the Thursday before the well known 3rd Friday of the expiration month

This should come to no surprise because the expiring future trades a lot less hours on that Friday and the volume must be small.

Note

The roll over date could have also been set to that Thursday by the

checkdate callable. But that isn’t the point of the sample.

Concluding

backtrader includes now a flexible mechanism to allow rolling over futures to create a continuous stream.

Sample Usage

$ ./rollover.py --help

usage: rollover.py [-h] [--no-cerebro] [--rollover] [--checkdate]

[--checkcondition] [--plot [kwargs]]

Sample for Roll Over of Futures

optional arguments:

-h, --help show this help message and exit

--no-cerebro Use RollOver Directly (default: False)

--rollover

--checkdate Change during expiration week (default: False)

--checkcondition Change when a given condition is met (default: False)

--plot [kwargs], -p [kwargs]

Plot the read data applying any kwargs passed For

example: --plot style="candle" (to plot candles)

(default: None)

Sample Code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import bisect

import calendar

import datetime

import backtrader as bt

class TheStrategy(bt.Strategy):

def start(self):

header = ['Len', 'Name', 'RollName', 'Datetime', 'WeekDay', 'Open',

'High', 'Low', 'Close', 'Volume', 'OpenInterest']

print(', '.join(header))

def next(self):

txt = list()

txt.append('%04d' % len(self.data0))

txt.append('{}'.format(self.data0._dataname))

# Internal knowledge ... current expiration in use is in _d

txt.append('{}'.format(self.data0._d._dataname))

txt.append('{}'.format(self.data.datetime.date()))

txt.append('{}'.format(self.data.datetime.date().strftime('%a')))

txt.append('{}'.format(self.data.open[0]))

txt.append('{}'.format(self.data.high[0]))

txt.append('{}'.format(self.data.low[0]))

txt.append('{}'.format(self.data.close[0]))

txt.append('{}'.format(self.data.volume[0]))

txt.append('{}'.format(self.data.openinterest[0]))

print(', '.join(txt))

def checkdate(dt, d):

# Check if the date is in the week where the 3rd friday of Mar/Jun/Sep/Dec

# EuroStoxx50 expiry codes: MY

# M -> H, M, U, Z (Mar, Jun, Sep, Dec)

# Y -> 0, 1, 2, 3, 4, 5, 6, 7, 8, 9 -> year code. 5 -> 2015

MONTHS = dict(H=3, M=6, U=9, Z=12)

M = MONTHS[d._dataname[-2]]

centuria, year = divmod(dt.year, 10)

decade = centuria * 10

YCode = int(d._dataname[-1])

Y = decade + YCode

if Y < dt.year: # Example: year 2019 ... YCode is 0 for 2020

Y += 10

exp_day = 21 - (calendar.weekday(Y, M, 1) + 2) % 7

exp_dt = datetime.datetime(Y, M, exp_day)

# Get the year, week numbers

exp_year, exp_week, _ = exp_dt.isocalendar()

dt_year, dt_week, _ = dt.isocalendar()

# print('dt {} vs {} exp_dt'.format(dt, exp_dt))

# print('dt_week {} vs {} exp_week'.format(dt_week, exp_week))

# can switch if in same week

return (dt_year, dt_week) == (exp_year, exp_week)

def checkvolume(d0, d1):

return d0.volume[0] < d1.volume[0] # Switch if volume from d0 < d1

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

fcodes = ['199FESXM4', '199FESXU4', '199FESXZ4', '199FESXH5', '199FESXM5']

store = bt.stores.VChartFile()

ffeeds = [store.getdata(dataname=x) for x in fcodes]

rollkwargs = dict()

if args.checkdate:

rollkwargs['checkdate'] = checkdate

if args.checkcondition:

rollkwargs['checkcondition'] = checkvolume

if not args.no_cerebro:

if args.rollover:

cerebro.rolloverdata(name='FESX', *ffeeds, **rollkwargs)

else:

cerebro.chaindata(name='FESX', *ffeeds)

else:

drollover = bt.feeds.RollOver(*ffeeds, dataname='FESX', **rollkwargs)

cerebro.adddata(drollover)

cerebro.addstrategy(TheStrategy)

cerebro.run(stdstats=False)

if args.plot:

pkwargs = dict(style='bar')

if args.plot is not True: # evals to True but is not True

npkwargs = eval('dict(' + args.plot + ')') # args were passed

pkwargs.update(npkwargs)

cerebro.plot(**pkwargs)

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description='Sample for Roll Over of Futures')

parser.add_argument('--no-cerebro', required=False, action='store_true',

help='Use RollOver Directly')

parser.add_argument('--rollover', required=False, action='store_true')

parser.add_argument('--checkdate', required=False, action='store_true',

help='Change during expiration week')

parser.add_argument('--checkcondition', required=False,

action='store_true',

help='Change when a given condition is met')

# Plot options

parser.add_argument('--plot', '-p', nargs='?', required=False,

metavar='kwargs', const=True,

help=('Plot the read data applying any kwargs passed\n'

'\n'

'For example:\n'

'\n'

' --plot style="candle" (to plot candles)\n'))

if pargs is not None:

return parser.parse_args(pargs)

return parser.parse_args()

if __name__ == '__main__':

runstrat()