Data Resampling

When data is only available in a single timeframe and the analysis has to be done for a different timeframe, it’s time to do some resampling.

“Resampling” should actually be called “Upsampling” given that one goes from a source timeframe to a larger time frame (for example: days to weeks)

backtrader has built-in support for resampling by passing the original data

through a filter object. Although there are several ways to achieve this, a

straightforward interface exists to achieve this:

-

Instead of using

cerebro.adddata(data)to put adatainto the system usecerebro.resampledata(data, **kwargs)

There are two main options that can be controlled

-

Change the timeframe

-

Compress bars

To do so, use the following parameters when calling resampledata:

-

timeframe(default: bt.TimeFrame.Days)Destination timeframe which to be useful has to be equal or larger than the source

-

compression(default: 1)Compress the selected value “n” to 1 bar

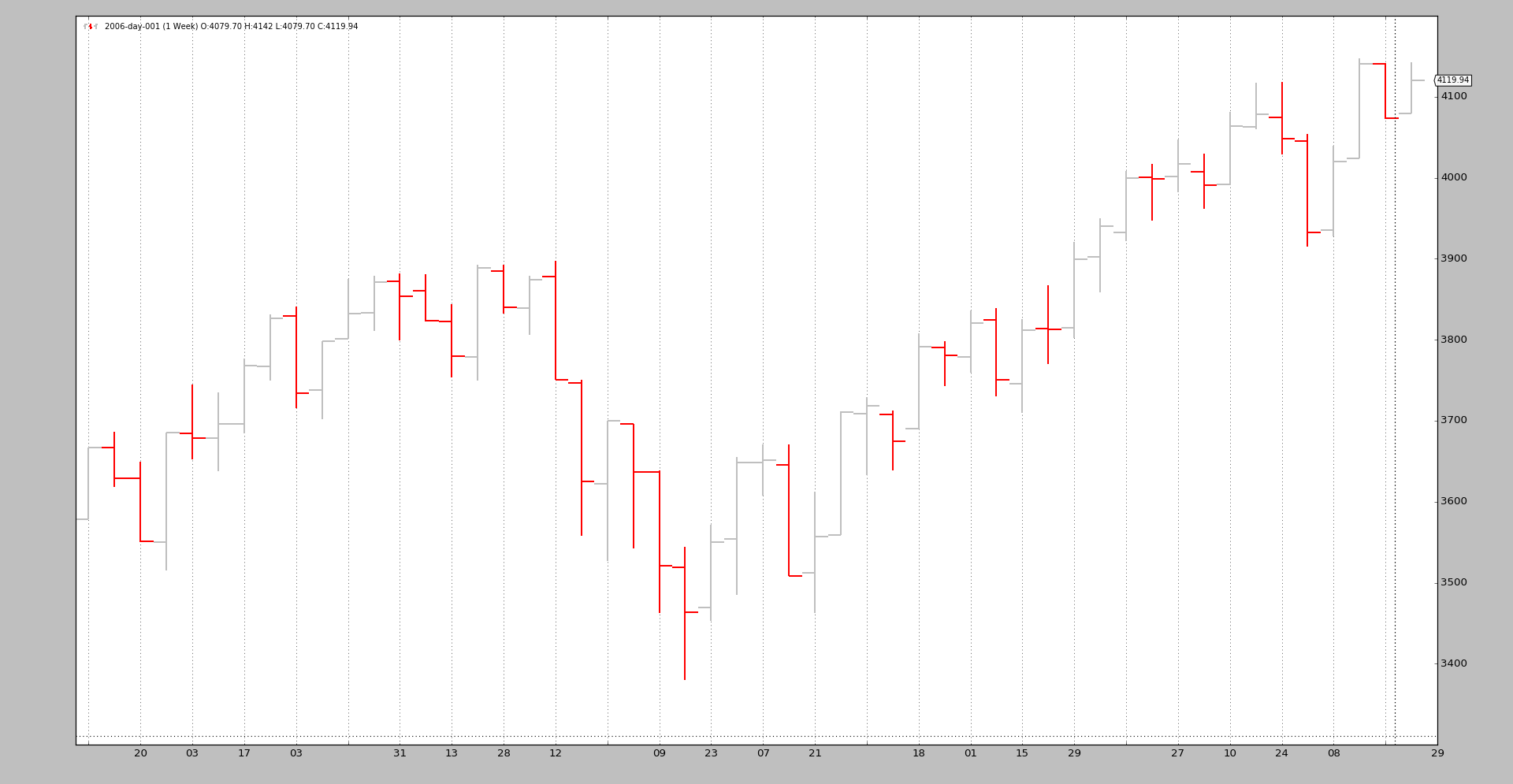

Let’s see an example from Daily to Weekly with a handcrafted script:

$ ./resampling-example.py --timeframe weekly --compression 1

The output:

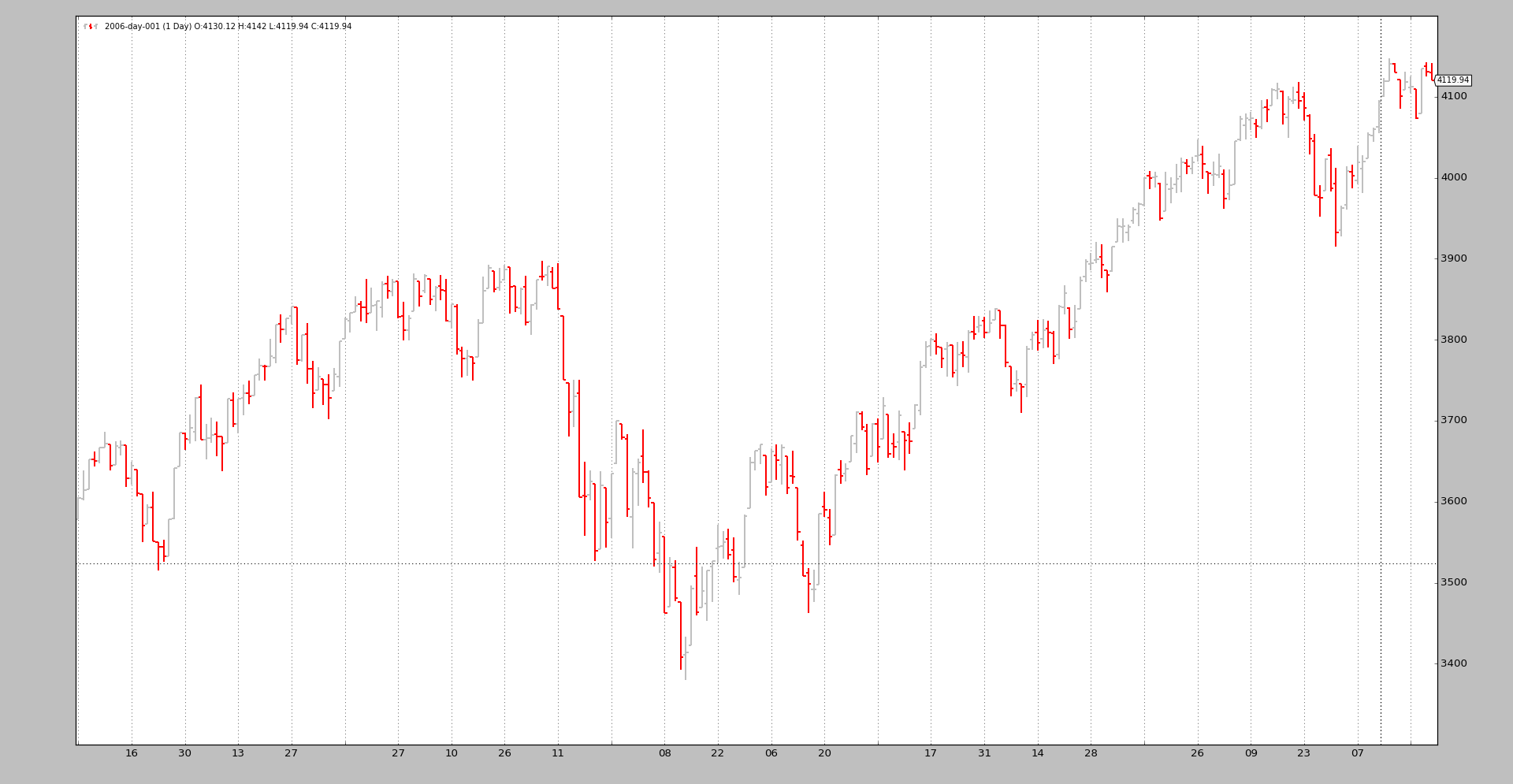

We can compare it to the original daily data:

$ ./resampling-example.py --timeframe daily --compression 1

The output:

The magic is done by executing the following steps:

-

Loading the data as usual

-

Feeding the data into cerebro with

resampledatawith the desired parameters:-

timeframe -

compression

-

The code in the sample (the entire script at the bottom).

# Load the Data

datapath = args.dataname or '../../datas/2006-day-001.txt'

data = btfeeds.BacktraderCSVData(dataname=datapath)

# Handy dictionary for the argument timeframe conversion

tframes = dict(

daily=bt.TimeFrame.Days,

weekly=bt.TimeFrame.Weeks,

monthly=bt.TimeFrame.Months)

# Add the resample data instead of the original

cerebro.resampledata(data,

timeframe=tframes[args.timeframe],

compression=args.compression)

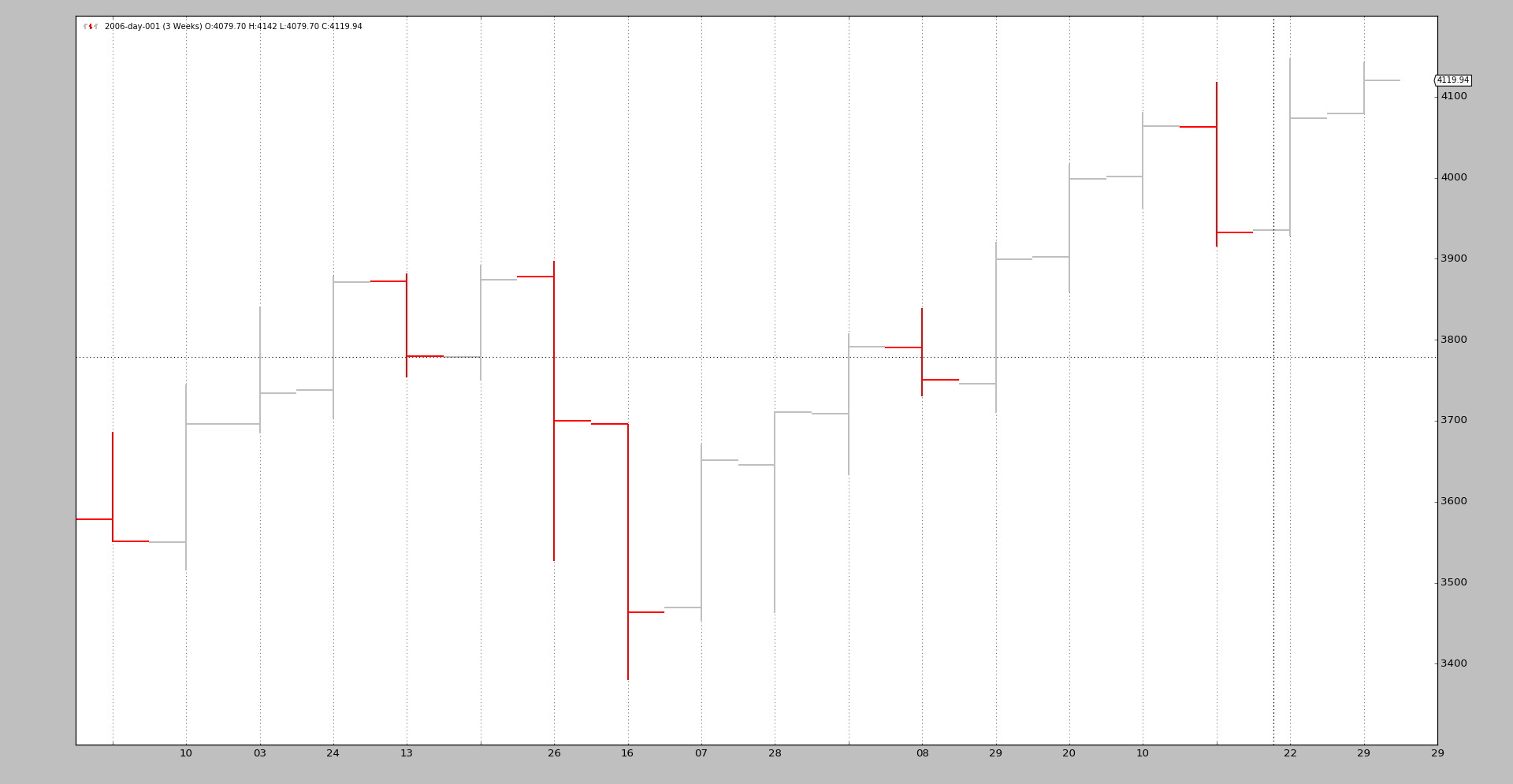

A last example in which we first change the time frame from daily to weekly and then apply a 3 to 1 compression:

$ ./resampling-example.py --timeframe weekly --compression 3

The output:

From the original 256 daily bars we end up with 18 3-week bars. The breakdown:

-

52 weeks

-

52 / 3 = 17.33 and therefore 18 bars

It doesn’t take much more. Of course intraday data can also be resampled.

The resampling filter supports additional parameters, which in most cases should not be touched:

-

bar2edge(default:True)resamples using time boundaries as the target. For example with a “ticks -> 5 seconds” the resulting 5 seconds bars will be aligned to xx:00, xx:05, xx:10 …

-

adjbartime(default:True)Use the time at the boundary to adjust the time of the delivered resampled bar instead of the last seen timestamp. If resampling to “5 seconds” the time of the bar will be adjusted for example to hh

05

even if the last seen timestamp was hh04.33

05

even if the last seen timestamp was hh04.33Note

Time will only be adjusted if “bar2edge” is True. It wouldn’t make sense to adjust the time if the bar has not been aligned to a boundary

-

rightedge(default:True)Use the right edge of the time boundaries to set the time.

If False and compressing to 5 seconds the time of a resampled bar for seconds between hh

00 and hh04 will be hh00 (the starting

boundaryIf True the used boundary for the time will be hh

05 (the ending

boundary) -

boundoff(default:0)Push the boundary for resampling/replaying by an amount of units.

If for example the resampling is from 1 minute to 15 minutes, the default behavior is to take the 1-minute bars from 00:01:00 until 00:15:00 to produce a 15-minutes replayed/resampled bar.

If

boundoffis set to1, then the boundary is pushed1 unitforward. In this case the original unit is a 1-minute bar. Consequently the resampling/replaying will now:- Use the bars from 00:00:00 to 00:14:00 for the generation of the 15-minutes bar

The sample code for the resampling test script.

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import backtrader as bt

import backtrader.feeds as btfeeds

def runstrat():

args = parse_args()

# Create a cerebro entity

cerebro = bt.Cerebro(stdstats=False)

# Add a strategy

cerebro.addstrategy(bt.Strategy)

# Load the Data

datapath = args.dataname or '../../datas/2006-day-001.txt'

data = btfeeds.BacktraderCSVData(dataname=datapath)

# Handy dictionary for the argument timeframe conversion

tframes = dict(

daily=bt.TimeFrame.Days,

weekly=bt.TimeFrame.Weeks,

monthly=bt.TimeFrame.Months)

# Add the resample data instead of the original

cerebro.resampledata(data,

timeframe=tframes[args.timeframe],

compression=args.compression)

# Run over everything

cerebro.run()

# Plot the result

cerebro.plot(style='bar')

def parse_args():

parser = argparse.ArgumentParser(

description='Pandas test script')

parser.add_argument('--dataname', default='', required=False,

help='File Data to Load')

parser.add_argument('--timeframe', default='weekly', required=False,

choices=['daily', 'weekly', 'monhtly'],

help='Timeframe to resample to')

parser.add_argument('--compression', default=1, required=False, type=int,

help='Compress n bars into 1')

return parser.parse_args()

if __name__ == '__main__':

runstrat()