Benchmarking

backtrader includes 2 different types of objects which can aid with tracking:

-

Observers

-

Analyzers

Ticket #89 is about adding benchmarking aginst an asset. Sensible as one may actually have a strategy that even if positive is below what simply tracking the asset would have delivered.

In the realm of Analyzers there was already a TimeReturn object which

tracks the evolution of the returns of the entire portfolio value (i.e:

including cash)

This could have also obviously been an Observer, so whilst adding some benchmarking some work has also gone into being able to plug together an Observer and an Analyzer which are meant to track the same thing.

Note

The major difference between Observers and Analyzers is the lines nature of observers, which is recording every value and makes them suitable for plotting and always for real time querying. This of course consumes memory.

Analyzers on the other hand return a set of results via

get_analysis and the implementation may not deliver any result

until the very end of a run.

Analyzers - Benchmarking

The standard TimeReturn analyzer has been extended to support tracking a

data feed. The 2 major parameters invoved:

-

timeframe(default:None) IfNonethen the complete return over the entire backtested period will be reportedPass

TimeFrame.NoTimeFrameto consider the entire dataset with no time constraints -

data(default:None)Reference asset to track instead of the portfolio value.

Note

this data must have been added to a

cerebroinstance withaddata,resampledataorreplaydata

(For more details and parameters go to the reference in the docs)

As such, the returns of the porftolio on a yearly basis can be tracked like this:

import backtrader as bt

cerebro = bt.Cerebro()

cerebro.addanalyzer(bt.analyzers.TimeReturn, timeframe=bt.TimeFrame.Years)

... # add datas, strategies ...

results = cerebro.run()

strat0 = results[0]

# If no name has been specified, the name is the class name lowercased

tret_analyzer = strat0.analyzers.getbyname('timereturn')

print(tret_analyzer.get_analysis())

If we wanted to track the returns of a data:

import backtrader as bt

cerebro = bt.Cerebro()

data = bt.feeds.OneOfTheFeeds(dataname='abcde', ...)

cerebro.adddata(data)

cerebro.addanalyzer(bt.analyzers.TimeReturn, timeframe=bt.TimeFrame.Years,

data=data)

... # add strategies ...

results = cerebro.run()

strat0 = results[0]

# If no name has been specified, the name is the class name lowercased

tret_analyzer = strat0.analyzers.getbyname('timereturn')

print(tret_analyzer.get_analysis())

If both are to be tracked, the best is to assign names to the analyzers:

import backtrader as bt

cerebro = bt.Cerebro()

data = bt.feeds.OneOfTheFeeds(dataname='abcde', ...)

cerebro.adddata(data)

cerebro.addanalyzer(bt.analyzers.TimeReturn, timeframe=bt.TimeFrame.Years,

data=data, _name='datareturns')

cerebro.addanalyzer(bt.analyzers.TimeReturn, timeframe=bt.TimeFrame.Years)

_name='timereturns')

... # add strategies ...

results = cerebro.run()

strat0 = results[0]

# If no name has been specified, the name is the class name lowercased

tret_analyzer = strat0.analyzers.getbyname('timereturns')

print(tret_analyzer.get_analysis())

tdata_analyzer = strat0.analyzers.getbyname('datareturns')

print(tdata_analyzer.get_analysis())

Observers - Benchmarking

Thanks to the background machinery allowing the usage of Analyzers inside Observers, 2 new observers have been added:

-

TimeReturn -

Benchmark

Both use the bt.analyzers.TimeReturn analyzer to collect results.

Rather than having code snippets like above, a full sample with some runs to show their functionality.

Observing TimeReturn

Execution:

$ ./observer-benchmark.py --plot --timereturn --timeframe notimeframe

Output.

Notice the execution options:

-

--timereturn: we are telling the sample to do just that -

--timeframe notimeframe: telling the analyzer to consider the entire data set disregarding timeframe boundaries.

The last plotted value is -0.26.

- The starting cash (obvious from the chart) is

50,000monetary units and the strategy ends up with36,970monetary units and hence a-26%value decrement.

Observing Benchmarking

Because benchmarking will also display the timereturn results, let’s run the same thing but with benchmarking active:

$ ./observer-benchmark.py --plot --timeframe notimeframe

Output.

Hey, hey hey!!!

-

The strategy is better as the asset:

-0.26vs-0.33It shouldn’t be a matter for celebration but at least is clear the strategy is not even as bad as the asset.

Moving down to track things on a yearly basis:

$ ./observer-benchmark.py --plot --timeframe years

Output

Watch out!

-

The strategy last value has changed very slightly from

-0.26to-0.27 -

The asset on the on the other hand shows a last value of

-0.35(versus-0.33above)

The reason for values so close to each other is that when moving from 2005 to 2006, both the strategy and the benchmarking asset were almost at the starting level in 2005.

Switching to a lower timeframe like weeks the entire picture changes:

$ ./observer-benchmark.py --plot --timeframe weeks

Output

Now:

-

The

Benchmarkobserver shows a much more nervous aspect. Things move up and down, because nowweeklyreturns for both the portfolio and the data are being tracked -

And because no trade was active in the last week of the year and the asset barely moved, the last displayed values are 0.00 (The last closing value before the last week was

25.54and the sample data closed at25.55, and the difference is felt first at the 4th decimal point)

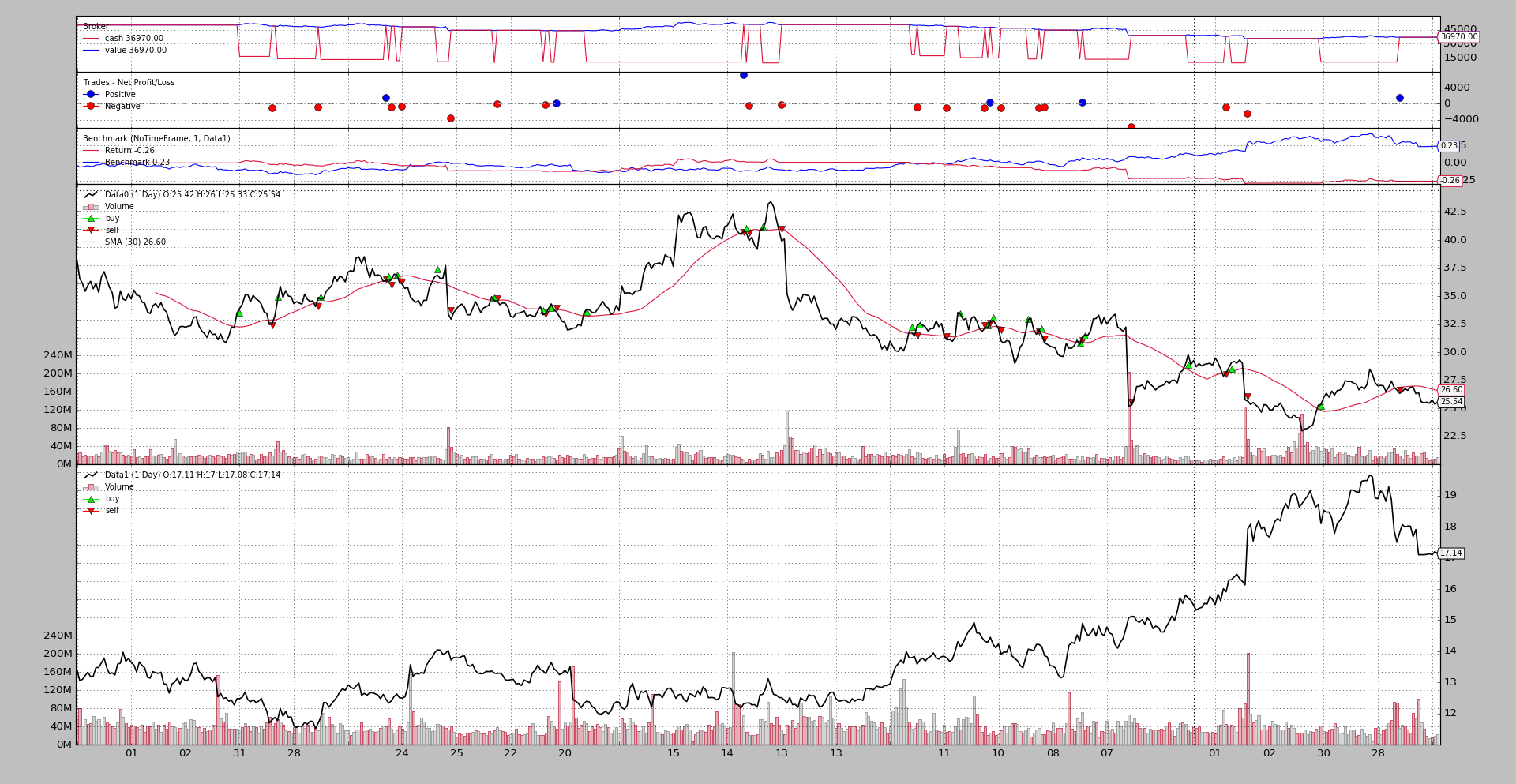

Observing Benchmarking - Another data

The sample allows to benchmark against a different data. The default is to

benchmark against Oracle when using --benchdata1. Considering the entire

dataset with --timeframe notimeframe:

$ ./observer-benchmark.py --plot --timeframe notimeframe --benchdata1

Output:

It’s clear now why there was no reason for celebration above:

-

The results of the strategy have not changed for

notimeframeand remain at-26%(-0.26) -

But when benchmarking against another data, this data has a

+23%(0.23) in the same period

Either the strategy needs a change or another asset better be traded.

Concluding

There are now two ways, using the same underlying code/calculations, to track the TimeReturn and Benchmark

- Observers (

TimeReturnandBenchmark)

and

- Analyzer (

TimeReturnandTimeReturnwith adataparameter)

Of course benchmarking doesn’t guarantee profit, just comparison.

Usage of the sample:

$ ./observer-benchmark.py --help

usage: observer-benchmark.py [-h] [--data0 DATA0] [--data1 DATA1]

[--benchdata1] [--fromdate FROMDATE]

[--todate TODATE] [--printout] [--cash CASH]

[--period PERIOD] [--stake STAKE] [--timereturn]

[--timeframe {months,days,notimeframe,years,None,weeks}]

[--plot [kwargs]]

Benchmark/TimeReturn Observers Sample

optional arguments:

-h, --help show this help message and exit

--data0 DATA0 Data0 to be read in (default:

../../datas/yhoo-1996-2015.txt)

--data1 DATA1 Data1 to be read in (default:

../../datas/orcl-1995-2014.txt)

--benchdata1 Benchmark against data1 (default: False)

--fromdate FROMDATE Starting date in YYYY-MM-DD format (default:

2005-01-01)

--todate TODATE Ending date in YYYY-MM-DD format (default: 2006-12-31)

--printout Print data lines (default: False)

--cash CASH Cash to start with (default: 50000)

--period PERIOD Period for the crossover moving average (default: 30)

--stake STAKE Stake to apply for the buy operations (default: 1000)

--timereturn Use TimeReturn observer instead of Benchmark (default:

None)

--timeframe {months,days,notimeframe,years,None,weeks}

TimeFrame to apply to the Observer (default: None)

--plot [kwargs], -p [kwargs]

Plot the read data applying any kwargs passed For

example: --plot style="candle" (to plot candles)

(default: None)

The code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import random

import backtrader as bt

class St(bt.Strategy):

params = (

('period', 10),

('printout', False),

('stake', 1000),

)

def __init__(self):

sma = bt.indicators.SMA(self.data, period=self.p.period)

self.crossover = bt.indicators.CrossOver(self.data, sma)

def start(self):

if self.p.printout:

txtfields = list()

txtfields.append('Len')

txtfields.append('Datetime')

txtfields.append('Open')

txtfields.append('High')

txtfields.append('Low')

txtfields.append('Close')

txtfields.append('Volume')

txtfields.append('OpenInterest')

print(','.join(txtfields))

def next(self):

if self.p.printout:

# Print only 1st data ... is just a check that things are running

txtfields = list()

txtfields.append('%04d' % len(self))

txtfields.append(self.data.datetime.datetime(0).isoformat())

txtfields.append('%.2f' % self.data0.open[0])

txtfields.append('%.2f' % self.data0.high[0])

txtfields.append('%.2f' % self.data0.low[0])

txtfields.append('%.2f' % self.data0.close[0])

txtfields.append('%.2f' % self.data0.volume[0])

txtfields.append('%.2f' % self.data0.openinterest[0])

print(','.join(txtfields))

if self.position:

if self.crossover < 0.0:

if self.p.printout:

print('CLOSE {} @%{}'.format(size,

self.data.close[0]))

self.close()

else:

if self.crossover > 0.0:

self.buy(size=self.p.stake)

if self.p.printout:

print('BUY {} @%{}'.format(self.p.stake,

self.data.close[0]))

TIMEFRAMES = {

None: None,

'days': bt.TimeFrame.Days,

'weeks': bt.TimeFrame.Weeks,

'months': bt.TimeFrame.Months,

'years': bt.TimeFrame.Years,

'notimeframe': bt.TimeFrame.NoTimeFrame,

}

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

cerebro.broker.set_cash(args.cash)

dkwargs = dict()

if args.fromdate:

fromdate = datetime.datetime.strptime(args.fromdate, '%Y-%m-%d')

dkwargs['fromdate'] = fromdate

if args.todate:

todate = datetime.datetime.strptime(args.todate, '%Y-%m-%d')

dkwargs['todate'] = todate

data0 = bt.feeds.YahooFinanceCSVData(dataname=args.data0, **dkwargs)

cerebro.adddata(data0, name='Data0')

cerebro.addstrategy(St,

period=args.period,

stake=args.stake,

printout=args.printout)

if args.timereturn:

cerebro.addobserver(bt.observers.TimeReturn,

timeframe=TIMEFRAMES[args.timeframe])

else:

benchdata = data0

if args.benchdata1:

data1 = bt.feeds.YahooFinanceCSVData(dataname=args.data1, **dkwargs)

cerebro.adddata(data1, name='Data1')

benchdata = data1

cerebro.addobserver(bt.observers.Benchmark,

data=benchdata,

timeframe=TIMEFRAMES[args.timeframe])

cerebro.run()

if args.plot:

pkwargs = dict()

if args.plot is not True: # evals to True but is not True

pkwargs = eval('dict(' + args.plot + ')') # args were passed

cerebro.plot(**pkwargs)

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description='Benchmark/TimeReturn Observers Sample')

parser.add_argument('--data0', required=False,

default='../../datas/yhoo-1996-2015.txt',

help='Data0 to be read in')

parser.add_argument('--data1', required=False,

default='../../datas/orcl-1995-2014.txt',

help='Data1 to be read in')

parser.add_argument('--benchdata1', required=False, action='store_true',

help=('Benchmark against data1'))

parser.add_argument('--fromdate', required=False,

default='2005-01-01',

help='Starting date in YYYY-MM-DD format')

parser.add_argument('--todate', required=False,

default='2006-12-31',

help='Ending date in YYYY-MM-DD format')

parser.add_argument('--printout', required=False, action='store_true',

help=('Print data lines'))

parser.add_argument('--cash', required=False, action='store',

type=float, default=50000,

help=('Cash to start with'))

parser.add_argument('--period', required=False, action='store',

type=int, default=30,

help=('Period for the crossover moving average'))

parser.add_argument('--stake', required=False, action='store',

type=int, default=1000,

help=('Stake to apply for the buy operations'))

parser.add_argument('--timereturn', required=False, action='store_true',

default=None,

help=('Use TimeReturn observer instead of Benchmark'))

parser.add_argument('--timeframe', required=False, action='store',

default=None, choices=TIMEFRAMES.keys(),

help=('TimeFrame to apply to the Observer'))

# Plot options

parser.add_argument('--plot', '-p', nargs='?', required=False,

metavar='kwargs', const=True,

help=('Plot the read data applying any kwargs passed\n'

'\n'

'For example:\n'

'\n'

' --plot style="candle" (to plot candles)\n'))

if pargs:

return parser.parse_args(pargs)

return parser.parse_args()

if __name__ == '__main__':

runstrat()