Order Management and Execution

Backtesting, and hence backtrader, would not be complete if orders could not be simulated. To do so, the following is available in the platform.

For order management 3 primitives:

-

buy -

sell -

cancel

Note

An update primitive is obviously something logic but common sense

dictates that such a method is mostly used by manual operators working with

a judgmental trading approach.

For order execution logic the following execution types:

-

Market -

Close -

Limit -

Stop -

StopLimit

Order Management

The main goal is ease of use and therefore the most direct (and simple) way to do order management is from the strategy itself.

The buy and self primitives have the following signature as Strategy

methods:

-

def buy(self, data=None, size=None, price=None, plimit=None, exectype=None, valid=None):

-

def buy(self, data=None, size=None, price=None, exectype=None, valid=None)

data-> data feed reference which is the assed to buy

If

Noneis passed the main data of the strategy is used as the targetsize-> int/long determining the stake to apply

if

Noneis passed, theSizeravailable in the strategy will be used to automatically determine the stake. The defaultSizeruses a fixed state of 1-

price-> will be ignored forMarketand can be left asNoneorders but must be a float for the other order types. If left asNonethe current closing price will be used -

plimit-> limit price inStopLimitorders wherepricewill be used as the trigger price

If left as

Nonethenpricewill be used as the limit (trigger and limit are the same)exectype-> One of the order execution types. IfNoneis passed thenMarketwill be assumed

The execution types are enumerated in

Order. Example:Order.Limitvalid-> float value from date2num (or from the data feed) or a datetime.datetime Python object

Note: A

Marketorder will be executed regardless of thevalidparameterRETURN VALUE: an

Orderinstance -

def sell(self, data=None, size=None, price=None, exectype=None, valid=None)

Because canceling an order just requires the order reference returned by

either buy or self, the primitive from the broker can be used (see below)

Some examples:

# buy the main date, with sizer default stake, Market order

order = self.buy()

# Market order - valid will be "IGNORED"

order = self.buy(valid=datetime.datetime.now() + datetime.timedelta(days=3))

# Market order - price will be IGNORED

order = self.buy(price=self.data.close[0] * 1.02)

# Market order - manual stake

order = self.buy(size=25)

# Limit order - want to set the price and can set a validity

order = self.buy(exectype=Order.Limit,

price=self.data.close[0] * 1.02,

valid=datetime.datetime.now() + datetime.timedelta(days=3)))

# StopLimit order - want to set the price, price limit

order = self.buy(exectype=Order.StopLimit,

price=self.data.close[0] * 1.02,

plimit=self.data.close[0] * 1.07)

# Canceling an existing order

self.broker.cancel(order)

Note

All order types can be create by creating an Order instance (or one of

its subclasses) and then passed to to the broker with:

order = self.broker.submit(order)

Note

There are buy and sell primitives in the broker itself, but they

are less forgiving with regards to default parameters.

Order Execution Logic

The broker uses 2 main guidelines (assumptions?) for order execution.

-

The current data has already happened and cannot be used to execcute an order.

If the logic in the strategy is something like:

if self.data.close > self.sma: # where sma is a Simple Moving Average self.buy() The expectation CANNOT be that the order will be executed with the ``close`` price which is being examined in the logic BECAUSE it has already happened. The order CAN BE 1st EXECUTED withing the bounds of the next set of Open/High/Low/Close price points (and the conditions set forth herein by the order) -

Volume does not play a role

It actually does in real trading if the trader goes for non-liquid assets or precisely the extremes (high/low) of a price bar are hit.

But hitting the high/low points is a seldom occurrence (if you do … you don’t need

backtrader) and the chosen assets will have enough liquidity to absorb the orders of any regular trading

Market

Execution:

Opening price of the next set of Open/High/Low/Close prices (commonly referred as bar)

Rationale:

If the logic has executed at point X in time and issued a Market order,

the next price spot that will happen is the upcoming open price

Note

This order executes always and disregards any price and valid

parameters used to create it

Close

Execution:

Using the close price of the next barwhen the next bar actually CLOSES

Rationale:

Most backtesting feeds contain already closed bars and the order will

execute immediately with the close price of the next bar. A daily data

feed is the most common example.

But the system could be fed with “tick” prices and the actual bar (time/date wise) is being udpated constantly with the new ticks, without actually moving to the next bar (because time and/or date have not changed)

Only when the time or date changes, the bar has actually been closed and the order gets executed

Limit

Execution:

The price set at order creation if the data touches it, starting with the

next price bar.

The order will be canceled if valid is set and the time point is reached

Price Matching:

backtrader tries to provide most realistic execution price for

Limit orders.

Using the 4 price spots (Open/High/Low/Close) it can be partially inferred if

the requested price can be improved.

For Buy Orders

- Case 1:

If the `open` price of the bar is below the limit price the order

executes immediately with the `open` price. The order has been swept

during the opening phase of the session

- Case 2:

If the `open` price has not penetrated below the limit price but the

`low` price is below the limit price, then the limit price has been

seen during the session and the order can be executed

The logic is obviously inverted for Sell orders.

Stop

Execution:

The trigger price set at order creation if the data touches it,

starting with the next price bar.

The order will be canceled if valid is set and the time point is reached

Price Matching:

backtrader tries to provide most realistic trigger price for

Stop orders.

Using the 4 price spots (Open/High/Low/Close) it can be partially inferred if

the requested price can be improved.

For \Stoporders whichBuy`

- Case 1:

If the `open` price of the bar is above the stop price the order is

executed immediately with the `open` price.

Intended to stop a loss if the price is moving upwards against an

existing short position

- Case 2:

If the `open` price has not penetrated above the stop price but the

`high` price is above the stop price, then the stop price has been

seen during the session and the order can be executed

The logic is obviously inverted for Stop orders which Sell.

StopLimit

Execution:

The trigger price sets the order in motion starting with the next price bar.

Price Matching:

-

Trigger: Uses the

Stopmatching logic (but only triggers and turns the order into aLimitorder) -

Limit: Uses the

Limitprice matching logic

Some samples

As always pictures (with code) are worth several million long explanations. Please note that the snippets concentrate on the order creation part. The full code is at the bottom.

A price closes above/below a simple moving average strategy will be used for the generation of the buy/sell signals

The signal is seen at the bottom of the charts: the CrossOver using the

crossover indicator.

A reference to generated “buy” orders will be kept to only allow one simultaneous order at most in the system.

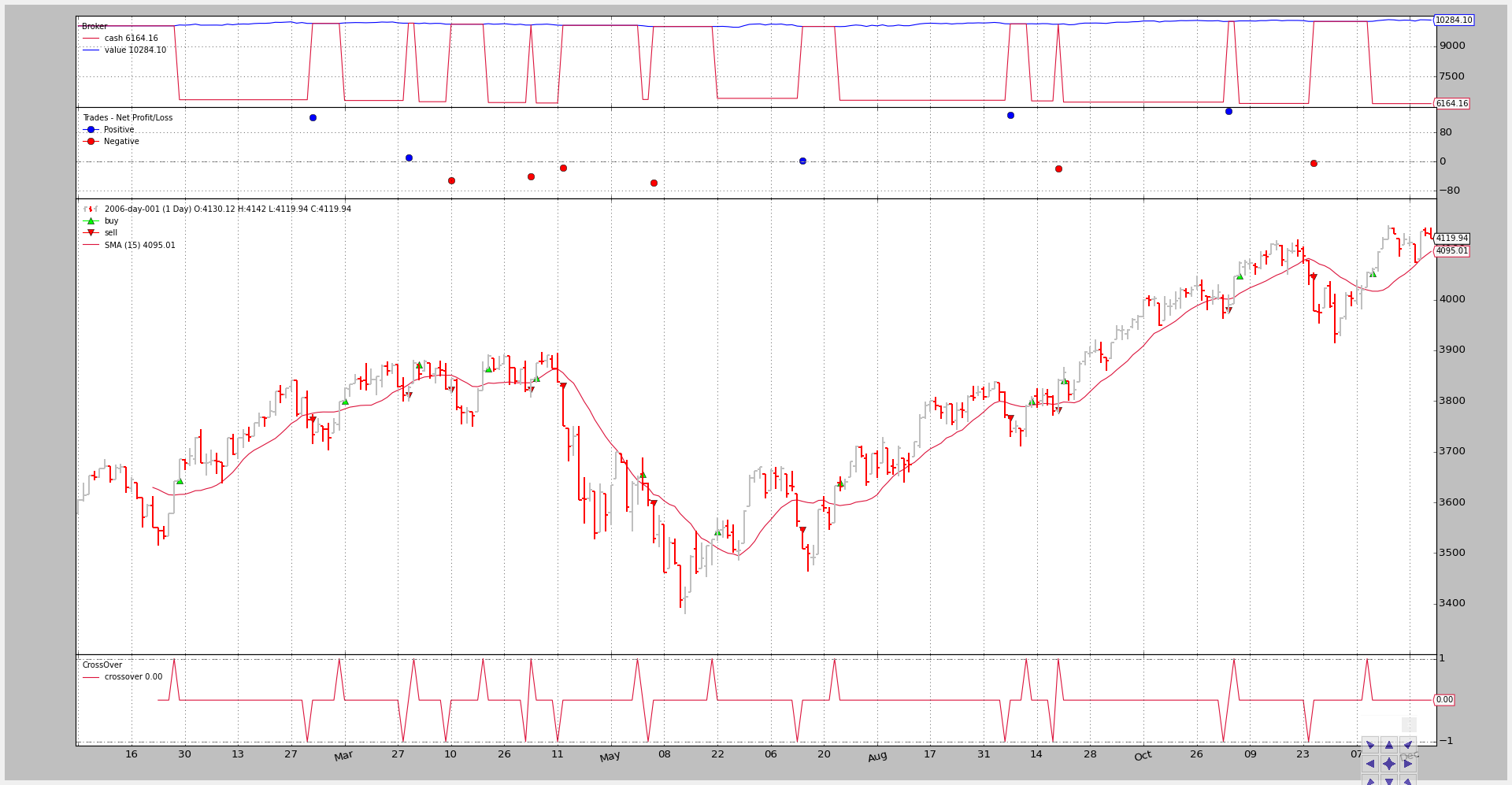

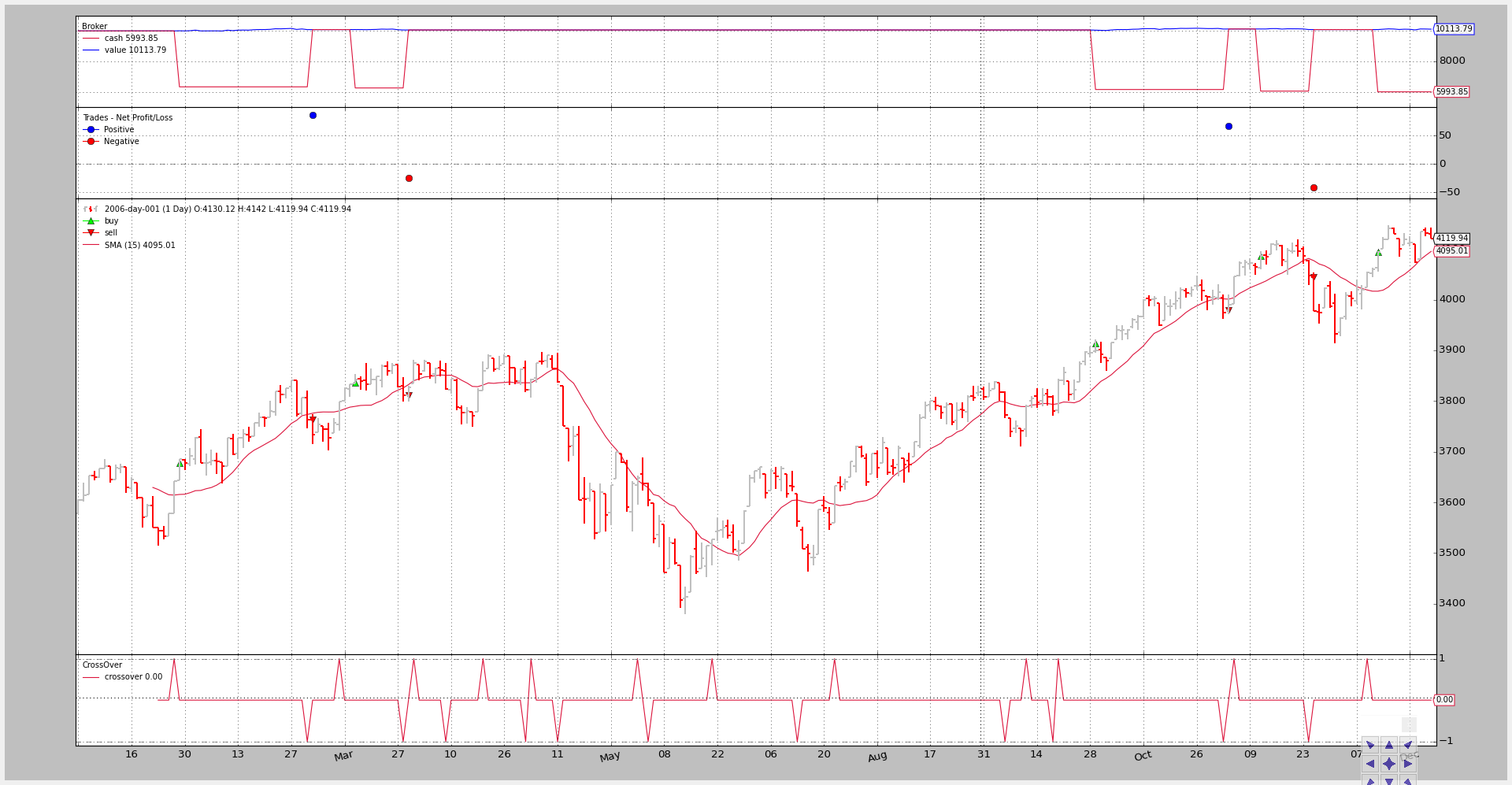

Execution Type: Market

See in the chart how how the orders are executed one bar after the signal is generated with the opening price.

if self.p.exectype == 'Market':

self.buy(exectype=bt.Order.Market) # default if not given

self.log('BUY CREATE, exectype Market, price %.2f' %

self.data.close[0])

The output chart.

The command line and output:

$ ./order-execution-samples.py --exectype Market

2006-01-26T23:59:59+00:00, BUY CREATE, exectype Market, price 3641.42

2006-01-26T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-01-27T23:59:59+00:00, BUY EXECUTED, Price: 3643.35, Cost: 3643.35, Comm 0.00

2006-03-02T23:59:59+00:00, SELL CREATE, 3763.73

2006-03-02T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-03-03T23:59:59+00:00, SELL EXECUTED, Price: 3763.95, Cost: 3763.95, Comm 0.00

...

...

2006-12-11T23:59:59+00:00, BUY CREATE, exectype Market, price 4052.89

2006-12-11T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-12-12T23:59:59+00:00, BUY EXECUTED, Price: 4052.55, Cost: 4052.55, Comm 0.00

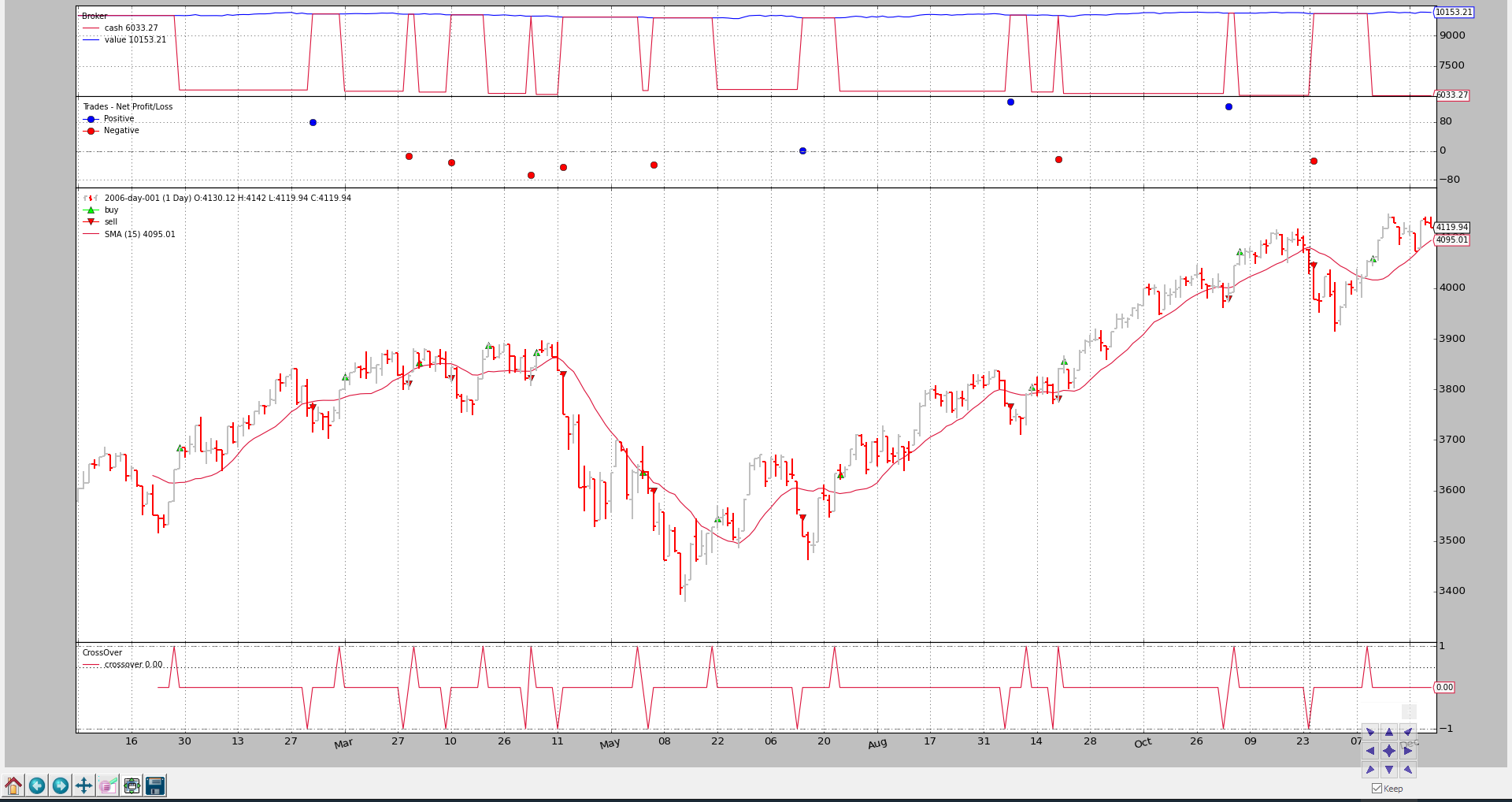

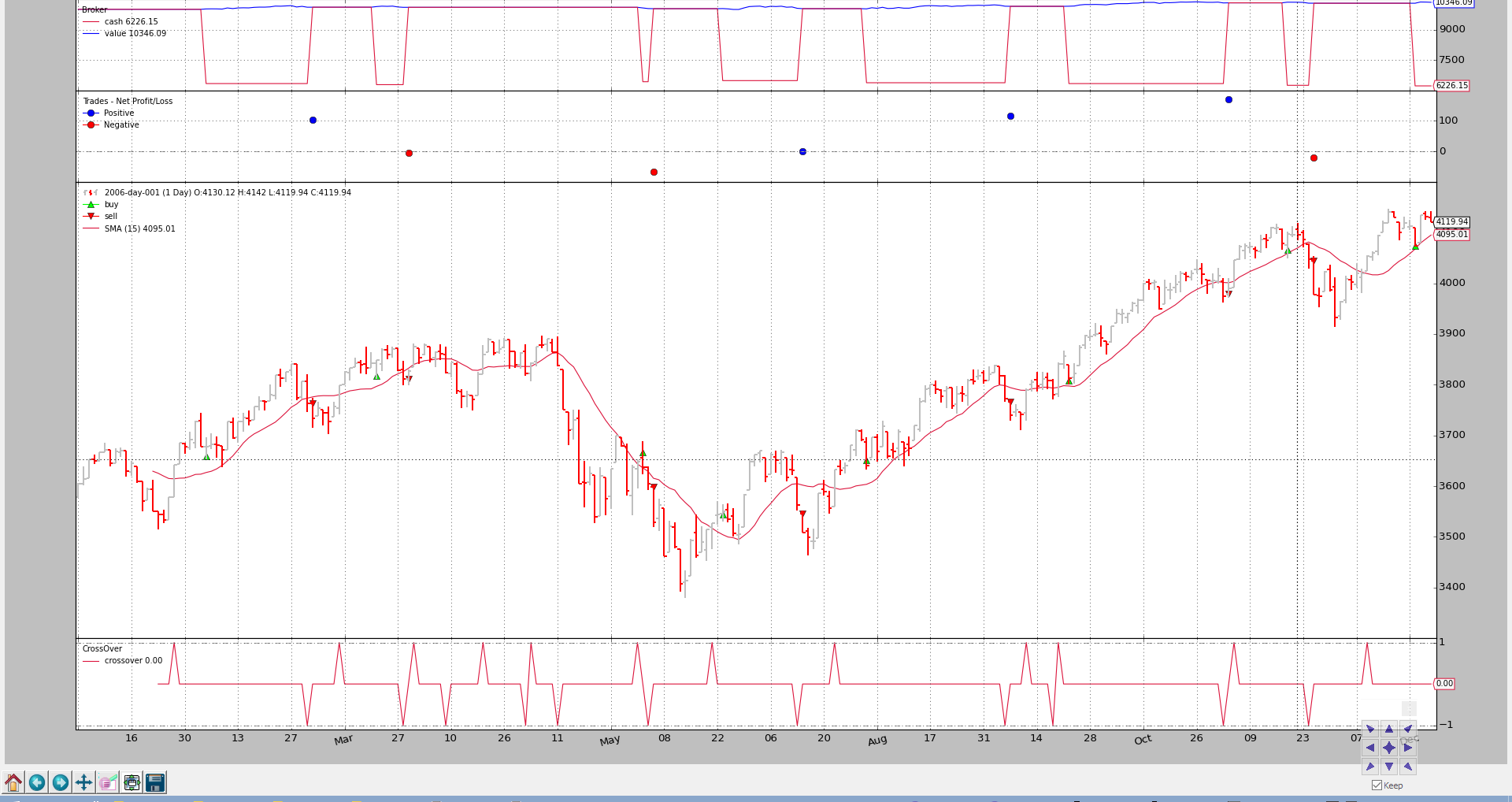

Execution Type: Close

Note

Following Issue #11 a development branch was created updating the chart and output. The wrong close price was being used.

Now the orders are also executed one bar after the signal but with the closing price.

elif self.p.exectype == 'Close':

self.buy(exectype=bt.Order.Close)

self.log('BUY CREATE, exectype Close, price %.2f' %

self.data.close[0])

The output chart.

The command line and output:

$ ./order-execution-samples.py --exectype Close

2006-01-26T23:59:59+00:00, BUY CREATE, exectype Close, price 3641.42

2006-01-26T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-01-27T23:59:59+00:00, BUY EXECUTED, Price: 3685.48, Cost: 3685.48, Comm 0.00

2006-03-02T23:59:59+00:00, SELL CREATE, 3763.73

2006-03-02T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-03-03T23:59:59+00:00, SELL EXECUTED, Price: 3763.95, Cost: 3763.95, Comm 0.00

...

...

2006-11-06T23:59:59+00:00, BUY CREATE, exectype Close, price 4045.22

2006-11-06T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-11-07T23:59:59+00:00, BUY EXECUTED, Price: 4072.86, Cost: 4072.86, Comm 0.00

2006-11-24T23:59:59+00:00, SELL CREATE, 4048.16

2006-11-24T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-11-27T23:59:59+00:00, SELL EXECUTED, Price: 4045.05, Cost: 4045.05, Comm 0.00

2006-12-11T23:59:59+00:00, BUY CREATE, exectype Close, price 4052.89

2006-12-11T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-12-12T23:59:59+00:00, BUY EXECUTED, Price: 4059.74, Cost: 4059.74, Comm 0.00

Execution Type: Limit

Validity is being calculated some lines before in case it has been passed as argument.

if self.p.valid:

valid = self.data.datetime.date(0) + \

datetime.timedelta(days=self.p.valid)

else:

valid = None

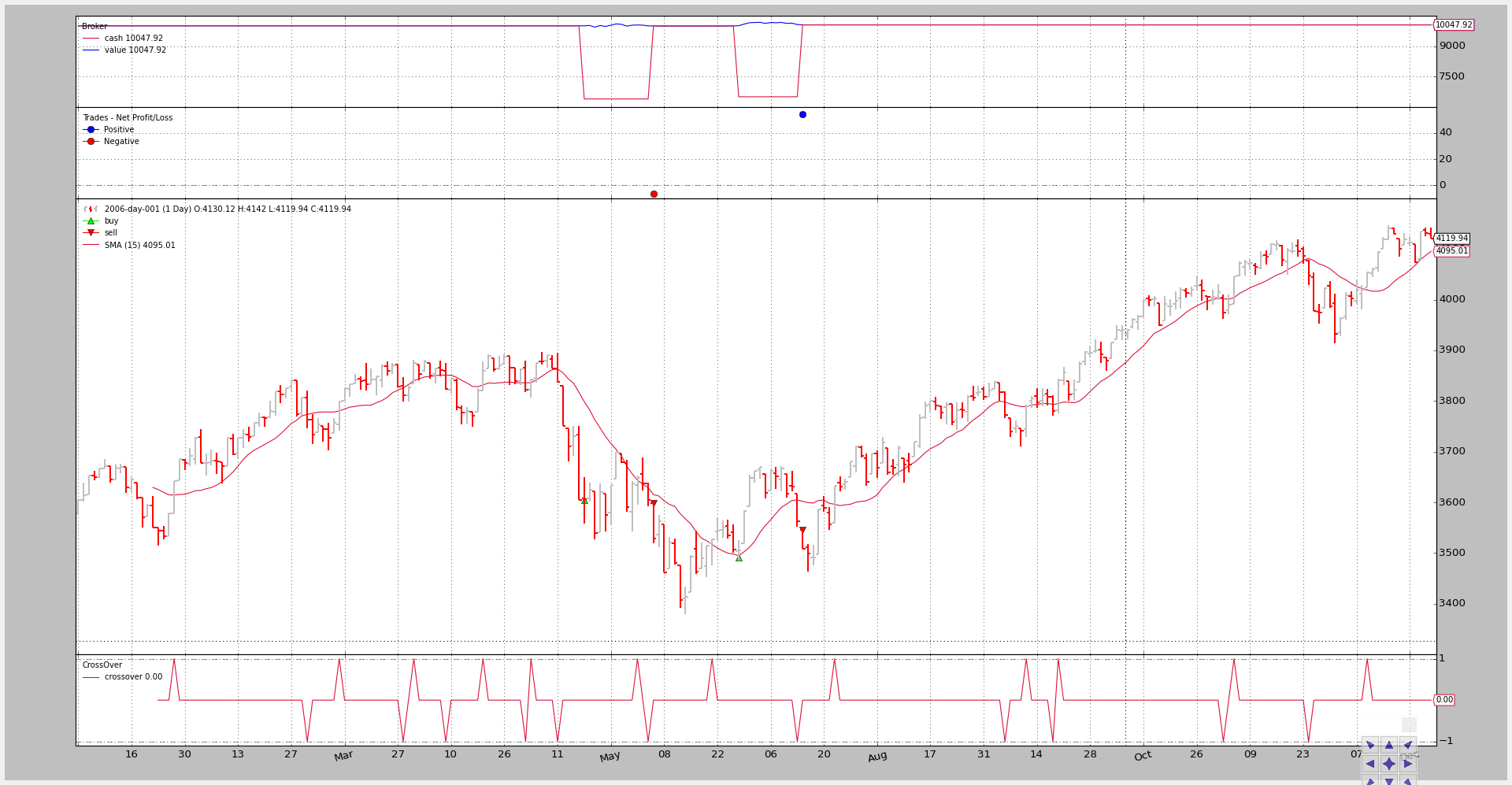

A limit price 1% below the signal generation price (the close at the signal bar) is set. Notice how this prevents many from the orders above from being executed.

elif self.p.exectype == 'Limit':

price = self.data.close * (1.0 - self.p.perc1 / 100.0)

self.buy(exectype=bt.Order.Limit, price=price, valid=valid)

if self.p.valid:

txt = 'BUY CREATE, exectype Limit, price %.2f, valid: %s'

self.log(txt % (price, valid.strftime('%Y-%m-%d')))

else:

txt = 'BUY CREATE, exectype Limit, price %.2f'

self.log(txt % price)

The output chart.

Just 4 orders have been issued. Limiting the price trying to catch a small dip has completly changed the output.

The command line and output:

$ ./order-execution-samples.py --exectype Limit --perc1 1

2006-01-26T23:59:59+00:00, BUY CREATE, exectype Limit, price 3605.01

2006-01-26T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-05-18T23:59:59+00:00, BUY EXECUTED, Price: 3605.01, Cost: 3605.01, Comm 0.00

2006-06-05T23:59:59+00:00, SELL CREATE, 3604.33

2006-06-05T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-06-06T23:59:59+00:00, SELL EXECUTED, Price: 3598.58, Cost: 3598.58, Comm 0.00

2006-06-21T23:59:59+00:00, BUY CREATE, exectype Limit, price 3491.57

2006-06-21T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-06-28T23:59:59+00:00, BUY EXECUTED, Price: 3491.57, Cost: 3491.57, Comm 0.00

2006-07-13T23:59:59+00:00, SELL CREATE, 3562.56

2006-07-13T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-07-14T23:59:59+00:00, SELL EXECUTED, Price: 3545.92, Cost: 3545.92, Comm 0.00

2006-07-24T23:59:59+00:00, BUY CREATE, exectype Limit, price 3596.60

2006-07-24T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

Execution Type: Limit with validity

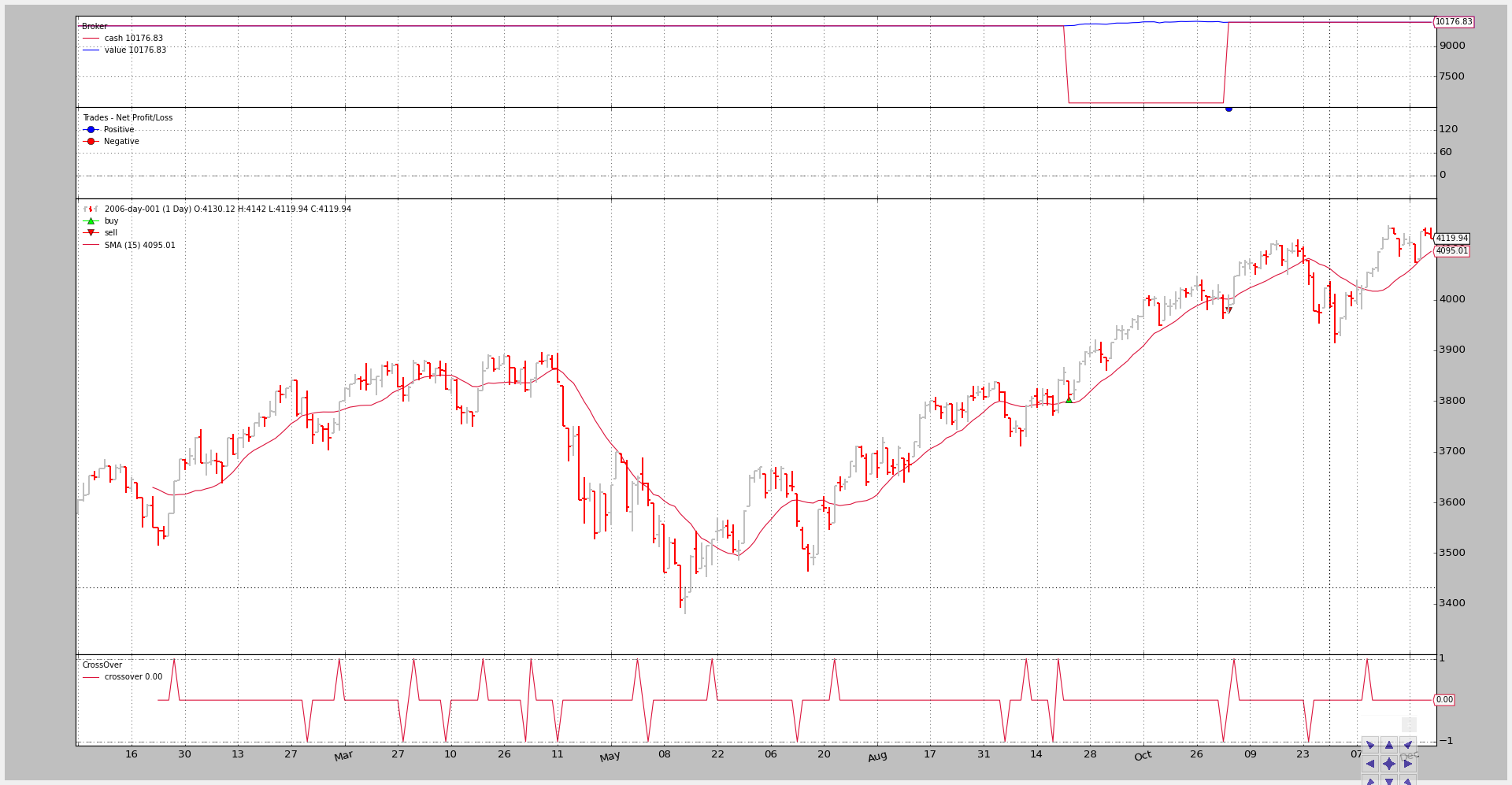

To not wait forever on a limit order which may only execute when the price is moving against the “buy” order, the order will only be valid 4 (calendar) days.

The output chart.

More orders have been generated, but all but one “buy” order expired, further limiting the amount of operations.

The command line and output:

$ ./order-execution-samples.py --exectype Limit --perc1 1 --valid 4

2006-01-26T23:59:59+00:00, BUY CREATE, exectype Limit, price 3605.01, valid: 2006-01-30

2006-01-26T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-01-30T23:59:59+00:00, BUY EXPIRED

2006-03-10T23:59:59+00:00, BUY CREATE, exectype Limit, price 3760.48, valid: 2006-03-14

2006-03-10T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-03-14T23:59:59+00:00, BUY EXPIRED

2006-03-30T23:59:59+00:00, BUY CREATE, exectype Limit, price 3835.86, valid: 2006-04-03

2006-03-30T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-04-03T23:59:59+00:00, BUY EXPIRED

2006-04-20T23:59:59+00:00, BUY CREATE, exectype Limit, price 3821.40, valid: 2006-04-24

2006-04-20T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-04-24T23:59:59+00:00, BUY EXPIRED

2006-05-04T23:59:59+00:00, BUY CREATE, exectype Limit, price 3804.65, valid: 2006-05-08

2006-05-04T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-05-08T23:59:59+00:00, BUY EXPIRED

2006-06-01T23:59:59+00:00, BUY CREATE, exectype Limit, price 3611.85, valid: 2006-06-05

2006-06-01T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-06-05T23:59:59+00:00, BUY EXPIRED

2006-06-21T23:59:59+00:00, BUY CREATE, exectype Limit, price 3491.57, valid: 2006-06-25

2006-06-21T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-06-26T23:59:59+00:00, BUY EXPIRED

2006-07-24T23:59:59+00:00, BUY CREATE, exectype Limit, price 3596.60, valid: 2006-07-28

2006-07-24T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-07-28T23:59:59+00:00, BUY EXPIRED

2006-09-12T23:59:59+00:00, BUY CREATE, exectype Limit, price 3751.07, valid: 2006-09-16

2006-09-12T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-09-18T23:59:59+00:00, BUY EXPIRED

2006-09-20T23:59:59+00:00, BUY CREATE, exectype Limit, price 3802.90, valid: 2006-09-24

2006-09-20T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-09-22T23:59:59+00:00, BUY EXECUTED, Price: 3802.90, Cost: 3802.90, Comm 0.00

2006-11-02T23:59:59+00:00, SELL CREATE, 3974.62

2006-11-02T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-11-03T23:59:59+00:00, SELL EXECUTED, Price: 3979.73, Cost: 3979.73, Comm 0.00

2006-11-06T23:59:59+00:00, BUY CREATE, exectype Limit, price 4004.77, valid: 2006-11-10

2006-11-06T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-11-10T23:59:59+00:00, BUY EXPIRED

2006-12-11T23:59:59+00:00, BUY CREATE, exectype Limit, price 4012.36, valid: 2006-12-15

2006-12-11T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-12-15T23:59:59+00:00, BUY EXPIRED

Execution Type: Stop

A stop price 1% above the signal price is set. That means that the strategy only buys if the signal is generated and the price continues climbing up, which could be intrepreted as a signal of strength.

This completely alters the execution panorama.

elif self.p.exectype == 'Stop':

price = self.data.close * (1.0 + self.p.perc1 / 100.0)

self.buy(exectype=bt.Order.Stop, price=price, valid=valid)

if self.p.valid:

txt = 'BUY CREATE, exectype Stop, price %.2f, valid: %s'

self.log(txt % (price, valid.strftime('%Y-%m-%d')))

else:

txt = 'BUY CREATE, exectype Stop, price %.2f'

self.log(txt % price)

The output chart.

The command line and output:

$ ./order-execution-samples.py --exectype Stop --perc1 1

2006-01-26T23:59:59+00:00, BUY CREATE, exectype Stop, price 3677.83

2006-01-26T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-01-27T23:59:59+00:00, BUY EXECUTED, Price: 3677.83, Cost: 3677.83, Comm 0.00

2006-03-02T23:59:59+00:00, SELL CREATE, 3763.73

2006-03-02T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-03-03T23:59:59+00:00, SELL EXECUTED, Price: 3763.95, Cost: 3763.95, Comm 0.00

2006-03-10T23:59:59+00:00, BUY CREATE, exectype Stop, price 3836.44

2006-03-10T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-03-15T23:59:59+00:00, BUY EXECUTED, Price: 3836.44, Cost: 3836.44, Comm 0.00

2006-03-28T23:59:59+00:00, SELL CREATE, 3811.45

2006-03-28T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-03-29T23:59:59+00:00, SELL EXECUTED, Price: 3811.85, Cost: 3811.85, Comm 0.00

2006-03-30T23:59:59+00:00, BUY CREATE, exectype Stop, price 3913.36

2006-03-30T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-09-29T23:59:59+00:00, BUY EXECUTED, Price: 3913.36, Cost: 3913.36, Comm 0.00

2006-11-02T23:59:59+00:00, SELL CREATE, 3974.62

2006-11-02T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-11-03T23:59:59+00:00, SELL EXECUTED, Price: 3979.73, Cost: 3979.73, Comm 0.00

2006-11-06T23:59:59+00:00, BUY CREATE, exectype Stop, price 4085.67

2006-11-06T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-11-13T23:59:59+00:00, BUY EXECUTED, Price: 4085.67, Cost: 4085.67, Comm 0.00

2006-11-24T23:59:59+00:00, SELL CREATE, 4048.16

2006-11-24T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-11-27T23:59:59+00:00, SELL EXECUTED, Price: 4045.05, Cost: 4045.05, Comm 0.00

2006-12-11T23:59:59+00:00, BUY CREATE, exectype Stop, price 4093.42

2006-12-11T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-12-13T23:59:59+00:00, BUY EXECUTED, Price: 4093.42, Cost: 4093.42, Comm 0.00

Execution Type: StopLimit

A stop price 1% above the signal price is set. But the limit price is set 0.5% above the signal (close) price which could be interpreted as: wait for the strength to show up but do not buy the peak. Wait for a dip.

Validity is capped at 20 (calendar) days

elif self.p.exectype == 'StopLimit':

price = self.data.close * (1.0 + self.p.perc1 / 100.0)

plimit = self.data.close * (1.0 + self.p.perc2 / 100.0)

self.buy(exectype=bt.Order.StopLimit, price=price, valid=valid,

plimit=plimit)

if self.p.valid:

txt = ('BUY CREATE, exectype StopLimit, price %.2f,'

' valid: %s, pricelimit: %.2f')

self.log(txt % (price, valid.strftime('%Y-%m-%d'), plimit))

else:

txt = ('BUY CREATE, exectype StopLimit, price %.2f,'

' pricelimit: %.2f')

self.log(txt % (price, plimit))

The output chart.

The command line and output:

$ ./order-execution-samples.py --exectype StopLimit --perc1 1 --perc2 0.5 --valid 20

2006-01-26T23:59:59+00:00, BUY CREATE, exectype StopLimit, price 3677.83, valid: 2006-02-15, pricelimit: 3659.63

2006-01-26T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-02-03T23:59:59+00:00, BUY EXECUTED, Price: 3659.63, Cost: 3659.63, Comm 0.00

2006-03-02T23:59:59+00:00, SELL CREATE, 3763.73

2006-03-02T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-03-03T23:59:59+00:00, SELL EXECUTED, Price: 3763.95, Cost: 3763.95, Comm 0.00

2006-03-10T23:59:59+00:00, BUY CREATE, exectype StopLimit, price 3836.44, valid: 2006-03-30, pricelimit: 3817.45

2006-03-10T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-03-21T23:59:59+00:00, BUY EXECUTED, Price: 3817.45, Cost: 3817.45, Comm 0.00

2006-03-28T23:59:59+00:00, SELL CREATE, 3811.45

2006-03-28T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-03-29T23:59:59+00:00, SELL EXECUTED, Price: 3811.85, Cost: 3811.85, Comm 0.00

2006-03-30T23:59:59+00:00, BUY CREATE, exectype StopLimit, price 3913.36, valid: 2006-04-19, pricelimit: 3893.98

2006-03-30T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-04-19T23:59:59+00:00, BUY EXPIRED

...

...

2006-12-11T23:59:59+00:00, BUY CREATE, exectype StopLimit, price 4093.42, valid: 2006-12-31, pricelimit: 4073.15

2006-12-11T23:59:59+00:00, ORDER ACCEPTED/SUBMITTED

2006-12-22T23:59:59+00:00, BUY EXECUTED, Price: 4073.15, Cost: 4073.15, Comm 0.00

Test Script Execution

Detailed in the command line help:

$ ./order-execution-samples.py --help

usage: order-execution-samples.py [-h] [--infile INFILE]

[--csvformat {bt,visualchart,sierrachart,yahoo,yahoo_unreversed}]

[--fromdate FROMDATE] [--todate TODATE]

[--plot] [--plotstyle {bar,line,candle}]

[--numfigs NUMFIGS] [--smaperiod SMAPERIOD]

[--exectype EXECTYPE] [--valid VALID]

[--perc1 PERC1] [--perc2 PERC2]

Showcase for Order Execution Types

optional arguments:

-h, --help show this help message and exit

--infile INFILE, -i INFILE

File to be read in

--csvformat {bt,visualchart,sierrachart,yahoo,yahoo_unreversed},

-c {bt,visualchart,sierrachart,yahoo,yahoo_unreversed}

CSV Format

--fromdate FROMDATE, -f FROMDATE

Starting date in YYYY-MM-DD format

--todate TODATE, -t TODATE

Ending date in YYYY-MM-DD format

--plot, -p Plot the read data

--plotstyle {bar,line,candle}, -ps {bar,line,candle}

Plot the read data

--numfigs NUMFIGS, -n NUMFIGS

Plot using n figures

--smaperiod SMAPERIOD, -s SMAPERIOD

Simple Moving Average Period

--exectype EXECTYPE, -e EXECTYPE

Execution Type: Market (default), Close, Limit,

Stop, StopLimit

--valid VALID, -v VALID

Validity for Limit sample: default 0 days

--perc1 PERC1, -p1 PERC1

% distance from close price at order creation time for

the limit/trigger price in Limit/Stop orders

--perc2 PERC2, -p2 PERC2

% distance from close price at order creation time for

the limit price in StopLimit orders

The full code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import os.path

import time

import sys

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

class OrderExecutionStrategy(bt.Strategy):

params = (

('smaperiod', 15),

('exectype', 'Market'),

('perc1', 3),

('perc2', 1),

('valid', 4),

)

def log(self, txt, dt=None):

''' Logging function fot this strategy'''

dt = dt or self.data.datetime[0]

if isinstance(dt, float):

dt = bt.num2date(dt)

print('%s, %s' % (dt.isoformat(), txt))

def notify_order(self, order):

if order.status in [order.Submitted, order.Accepted]:

# Buy/Sell order submitted/accepted to/by broker - Nothing to do

self.log('ORDER ACCEPTED/SUBMITTED', dt=order.created.dt)

self.order = order

return

if order.status in [order.Expired]:

self.log('BUY EXPIRED')

elif order.status in [order.Completed]:

if order.isbuy():

self.log(

'BUY EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

else: # Sell

self.log('SELL EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

# Sentinel to None: new orders allowed

self.order = None

def __init__(self):

# SimpleMovingAverage on main data

# Equivalent to -> sma = btind.SMA(self.data, period=self.p.smaperiod)

sma = btind.SMA(period=self.p.smaperiod)

# CrossOver (1: up, -1: down) close / sma

self.buysell = btind.CrossOver(self.data.close, sma, plot=True)

# Sentinel to None: new ordersa allowed

self.order = None

def next(self):

if self.order:

# An order is pending ... nothing can be done

return

# Check if we are in the market

if self.position:

# In the maerket - check if it's the time to sell

if self.buysell < 0:

self.log('SELL CREATE, %.2f' % self.data.close[0])

self.sell()

elif self.buysell > 0:

if self.p.valid:

valid = self.data.datetime.date(0) + \

datetime.timedelta(days=self.p.valid)

else:

valid = None

# Not in the market and signal to buy

if self.p.exectype == 'Market':

self.buy(exectype=bt.Order.Market) # default if not given

self.log('BUY CREATE, exectype Market, price %.2f' %

self.data.close[0])

elif self.p.exectype == 'Close':

self.buy(exectype=bt.Order.Close)

self.log('BUY CREATE, exectype Close, price %.2f' %

self.data.close[0])

elif self.p.exectype == 'Limit':

price = self.data.close * (1.0 - self.p.perc1 / 100.0)

self.buy(exectype=bt.Order.Limit, price=price, valid=valid)

if self.p.valid:

txt = 'BUY CREATE, exectype Limit, price %.2f, valid: %s'

self.log(txt % (price, valid.strftime('%Y-%m-%d')))

else:

txt = 'BUY CREATE, exectype Limit, price %.2f'

self.log(txt % price)

elif self.p.exectype == 'Stop':

price = self.data.close * (1.0 + self.p.perc1 / 100.0)

self.buy(exectype=bt.Order.Stop, price=price, valid=valid)

if self.p.valid:

txt = 'BUY CREATE, exectype Stop, price %.2f, valid: %s'

self.log(txt % (price, valid.strftime('%Y-%m-%d')))

else:

txt = 'BUY CREATE, exectype Stop, price %.2f'

self.log(txt % price)

elif self.p.exectype == 'StopLimit':

price = self.data.close * (1.0 + self.p.perc1 / 100.0)

plimit = self.data.close * (1.0 + self.p.perc2 / 100.0)

self.buy(exectype=bt.Order.StopLimit, price=price, valid=valid,

plimit=plimit)

if self.p.valid:

txt = ('BUY CREATE, exectype StopLimit, price %.2f,'

' valid: %s, pricelimit: %.2f')

self.log(txt % (price, valid.strftime('%Y-%m-%d'), plimit))

else:

txt = ('BUY CREATE, exectype StopLimit, price %.2f,'

' pricelimit: %.2f')

self.log(txt % (price, plimit))

def runstrat():

args = parse_args()

cerebro = bt.Cerebro()

data = getdata(args)

cerebro.adddata(data)

cerebro.addstrategy(

OrderExecutionStrategy,

exectype=args.exectype,

perc1=args.perc1,

perc2=args.perc2,

valid=args.valid,

smaperiod=args.smaperiod

)

cerebro.run()

if args.plot:

cerebro.plot(numfigs=args.numfigs, style=args.plotstyle)

def getdata(args):

dataformat = dict(

bt=btfeeds.BacktraderCSVData,

visualchart=btfeeds.VChartCSVData,

sierrachart=btfeeds.SierraChartCSVData,

yahoo=btfeeds.YahooFinanceCSVData,

yahoo_unreversed=btfeeds.YahooFinanceCSVData

)

dfkwargs = dict()

if args.csvformat == 'yahoo_unreversed':

dfkwargs['reverse'] = True

if args.fromdate:

fromdate = datetime.datetime.strptime(args.fromdate, '%Y-%m-%d')

dfkwargs['fromdate'] = fromdate

if args.todate:

fromdate = datetime.datetime.strptime(args.todate, '%Y-%m-%d')

dfkwargs['todate'] = todate

dfkwargs['dataname'] = args.infile

dfcls = dataformat[args.csvformat]

return dfcls(**dfkwargs)

def parse_args():

parser = argparse.ArgumentParser(

description='Showcase for Order Execution Types')

parser.add_argument('--infile', '-i', required=False,

default='../datas/2006-day-001.txt',

help='File to be read in')

parser.add_argument('--csvformat', '-c', required=False, default='bt',

choices=['bt', 'visualchart', 'sierrachart',

'yahoo', 'yahoo_unreversed'],

help='CSV Format')

parser.add_argument('--fromdate', '-f', required=False, default=None,

help='Starting date in YYYY-MM-DD format')

parser.add_argument('--todate', '-t', required=False, default=None,

help='Ending date in YYYY-MM-DD format')

parser.add_argument('--plot', '-p', action='store_false', required=False,

help='Plot the read data')

parser.add_argument('--plotstyle', '-ps', required=False, default='bar',

choices=['bar', 'line', 'candle'],

help='Plot the read data')

parser.add_argument('--numfigs', '-n', required=False, default=1,

help='Plot using n figures')

parser.add_argument('--smaperiod', '-s', required=False, default=15,

help='Simple Moving Average Period')

parser.add_argument('--exectype', '-e', required=False, default='Market',

help=('Execution Type: Market (default), Close, Limit,'

' Stop, StopLimit'))

parser.add_argument('--valid', '-v', required=False, default=0, type=int,

help='Validity for Limit sample: default 0 days')

parser.add_argument('--perc1', '-p1', required=False, default=0.0,

type=float,

help=('%% distance from close price at order creation'

' time for the limit/trigger price in Limit/Stop'

' orders'))

parser.add_argument('--perc2', '-p2', required=False, default=0.0,

type=float,

help=('%% distance from close price at order creation'

' time for the limit price in StopLimit orders'))

return parser.parse_args()

if __name__ == '__main__':

runstrat()