Hello Algotrading!

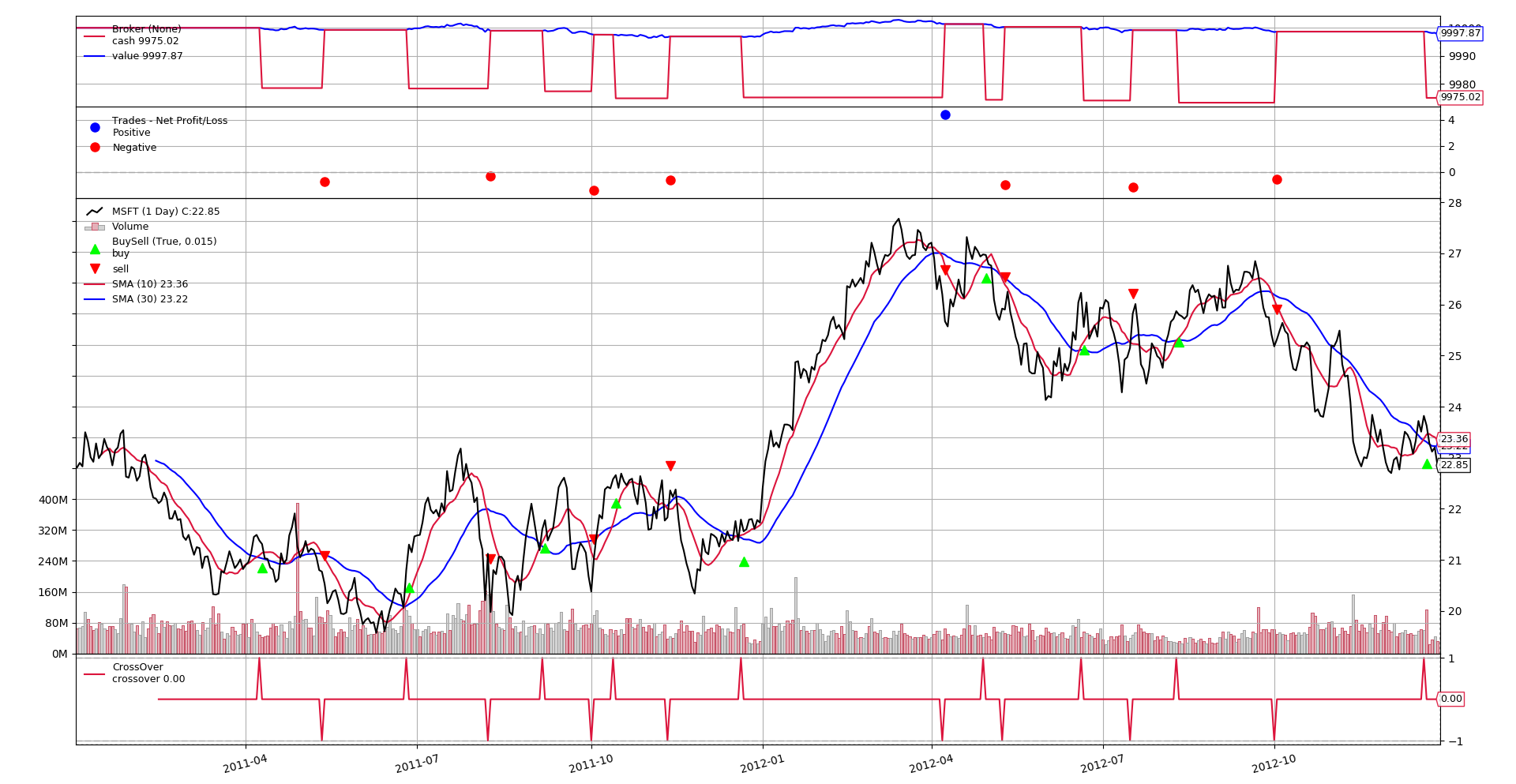

A classic Simple Moving Average Crossover strategy, can be easily implemented and in different ways. The results and the chart are the same for the three snippets presented below.

from datetime import datetime

import backtrader as bt

# Create a subclass of Strategy to define the indicators and logic

class SmaCross(bt.Strategy):

# list of parameters which are configurable for the strategy

params = dict(

pfast=10, # period for the fast moving average

pslow=30 # period for the slow moving average

)

def __init__(self):

sma1 = bt.ind.SMA(period=self.p.pfast) # fast moving average

sma2 = bt.ind.SMA(period=self.p.pslow) # slow moving average

self.crossover = bt.ind.CrossOver(sma1, sma2) # crossover signal

def next(self):

if not self.position: # not in the market

if self.crossover > 0: # if fast crosses slow to the upside

self.buy() # enter long

elif self.crossover < 0: # in the market & cross to the downside

self.close() # close long position

cerebro = bt.Cerebro() # create a "Cerebro" engine instance

# Create a data feed

data = bt.feeds.YahooFinanceData(dataname='MSFT',

fromdate=datetime(2011, 1, 1),

todate=datetime(2012, 12, 31))

cerebro.adddata(data) # Add the data feed

cerebro.addstrategy(SmaCross) # Add the trading strategy

cerebro.run() # run it all

cerebro.plot() # and plot it with a single command

from datetime import datetime

import backtrader as bt

# Create a subclass of Strategy to define the indicators and logic

class SmaCross(bt.Strategy):

# list of parameters which are configurable for the strategy

params = dict(

pfast=10, # period for the fast moving average

pslow=30 # period for the slow moving average

)

def __init__(self):

sma1 = bt.ind.SMA(period=self.p.pfast) # fast moving average

sma2 = bt.ind.SMA(period=self.p.pslow) # slow moving average

self.crossover = bt.ind.CrossOver(sma1, sma2) # crossover signal

def next(self):

if not self.position: # not in the market

if self.crossover > 0: # if fast crosses slow to the upside

self.order_target_size(target=1) # enter long

elif self.crossover < 0: # in the market & cross to the downside

self.order_target_size(target=0) # close long position

cerebro = bt.Cerebro() # create a "Cerebro" engine instance

# Create a data feed

data = bt.feeds.YahooFinanceData(dataname='MSFT',

fromdate=datetime(2011, 1, 1),

todate=datetime(2012, 12, 31))

cerebro.adddata(data) # Add the data feed

cerebro.addstrategy(SmaCross) # Add the trading strategy

cerebro.run() # run it all

cerebro.plot() # and plot it with a single command

from datetime import datetime

import backtrader as bt

# Create a subclass of SignaStrategy to define the indicators and signals

class SmaCross(bt.SignalStrategy):

# list of parameters which are configurable for the strategy

params = dict(

pfast=10, # period for the fast moving average

pslow=30 # period for the slow moving average

)

def __init__(self):

sma1 = bt.ind.SMA(period=self.p.pfast) # fast moving average

sma2 = bt.ind.SMA(period=self.p.pslow) # slow moving average

crossover = bt.ind.CrossOver(sma1, sma2) # crossover signal

self.signal_add(bt.SIGNAL_LONG, crossover) # use it as LONG signal

cerebro = bt.Cerebro() # create a "Cerebro" engine instance

# Create a data feed

data = bt.feeds.YahooFinanceData(dataname='MSFT',

fromdate=datetime(2011, 1, 1),

todate=datetime(2012, 12, 31))

cerebro.adddata(data) # Add the data feed

cerebro.addstrategy(SmaCross) # Add the trading strategy

cerebro.run() # run it all

cerebro.plot() # and plot it with a single command