Renko Bricks

The Renko Bricks is a different way to present the evolution of prices in

which price plays a more important role than time. This has been introduced as

a filter in release 1.9.54.122 of backtrader

Stockcharts has a good reference on the Renko Bricks. See Renko Bricks @StockCharts

Some examples

Note

The size=35 and align=10.0 parameters are appropriate for the

sample data in the backtrader repository. Those values have to be

fine tuned for each data asset.

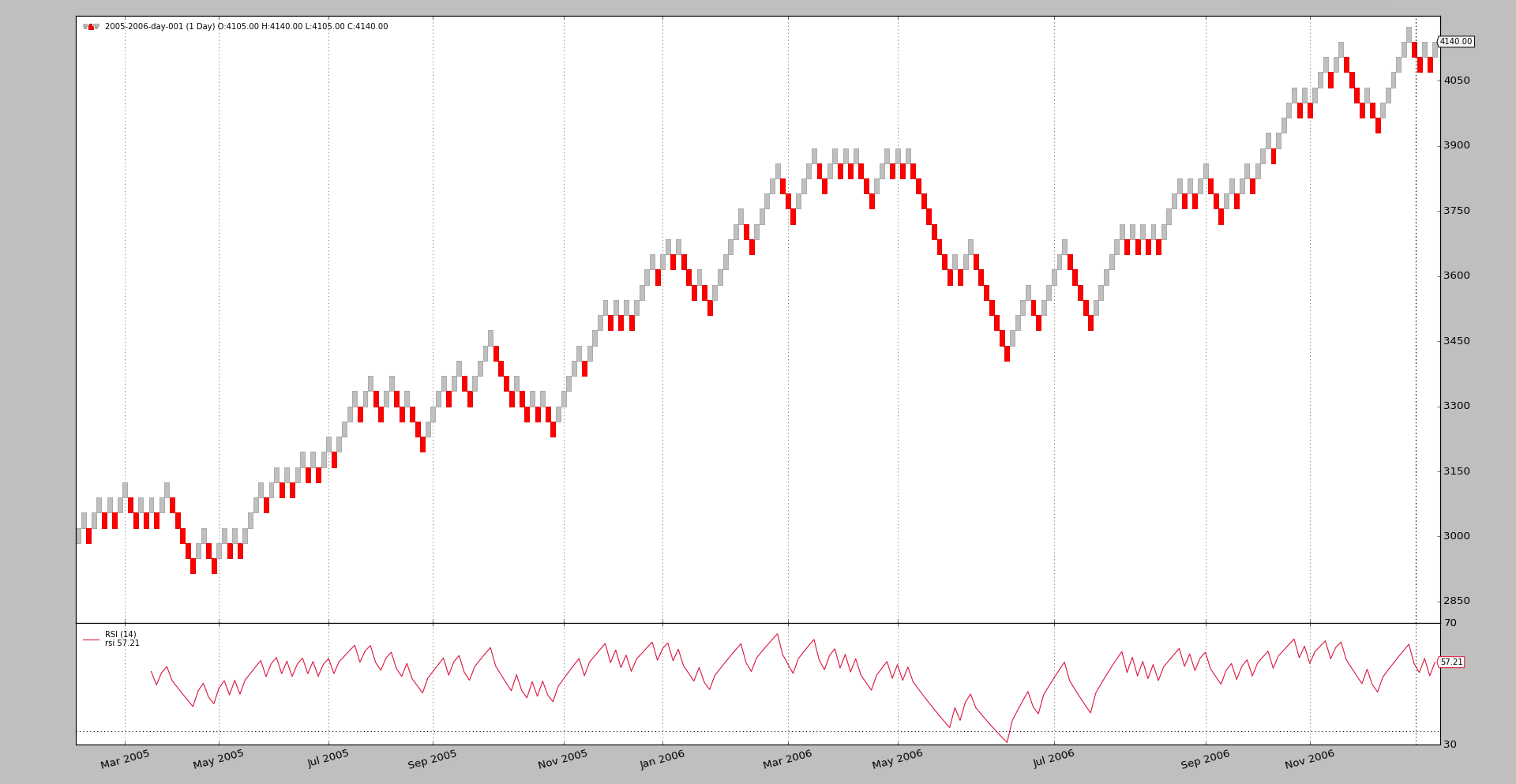

First, let’s put the Renko Bricks alone in a chart:

$ ./renko.py --renko size=35,align=10.0 --plot

The output

One can see that the chart immediately reveals some resistance/support areas, which is one of the main advantages of the Renko Bricks. It should also be obvious that the temporal evolution in the X-Axis is no longer constant and is stretched or compressed, depending on whether the price action was more static during the period or moved several bricks.

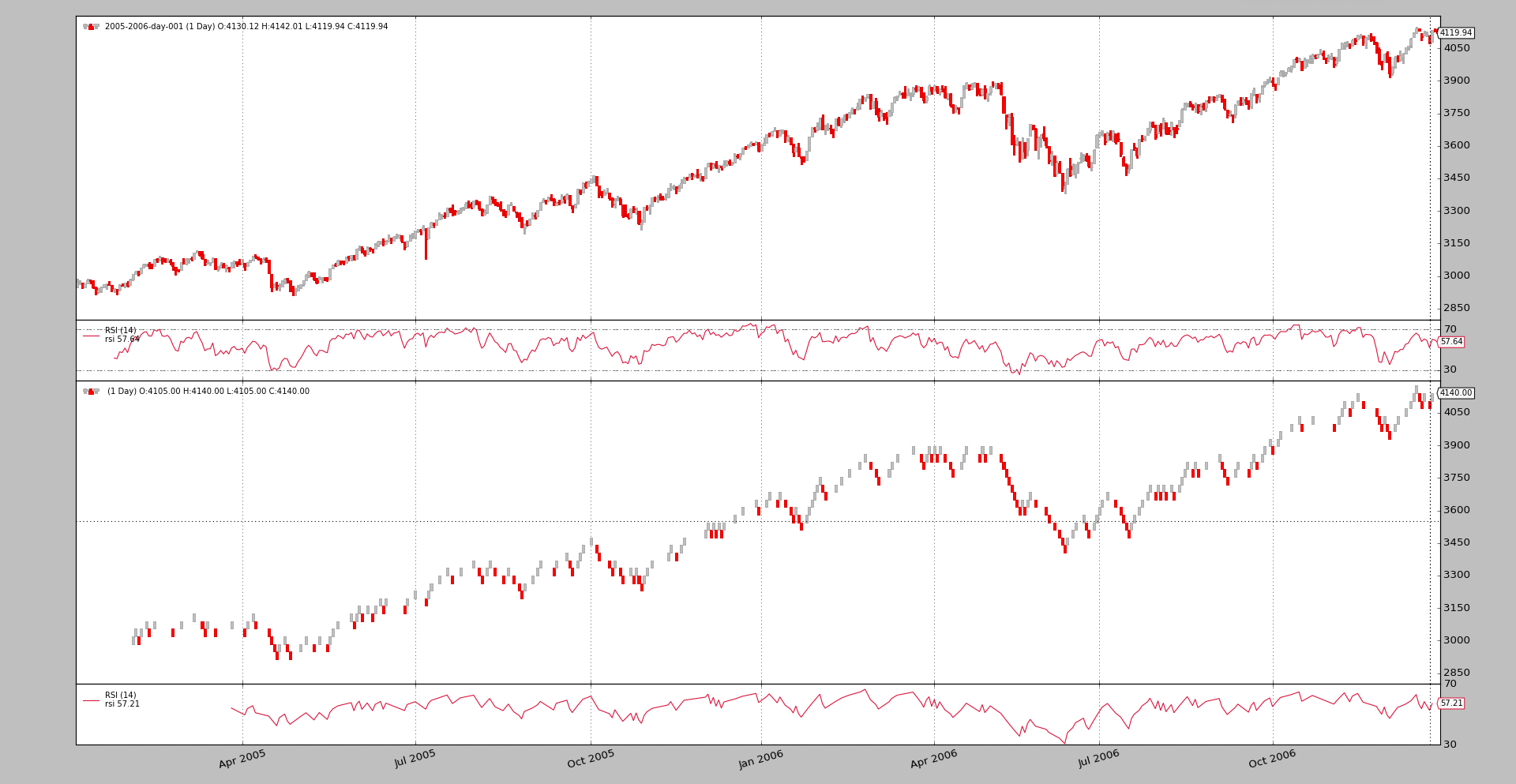

To better see and appreciate the effects, let’s put the normal price bars and the Renko Bricks together on a chart:

$ ./renko.py --renko size=35,align=10.0 --plot --dual

The output

The strechting and compression of time periods is now a lot more obvious. One

other factor to consider is how the focus on the price action also has an

effect on the indicators which are applied, as shown by the two RSI

indicators which have been placed on the chart.

Sample Usage

$ ./renko.py --help

usage: renko.py [-h] [--data0 DATA0] [--fromdate FROMDATE] [--todate TODATE]

[--cerebro kwargs] [--broker kwargs] [--sizer kwargs]

[--strat kwargs] [--plot [kwargs]] [--renko kwargs] [--dual]

Renko bricks sample

optional arguments:

-h, --help show this help message and exit

--data0 DATA0 Data to read in (default:

../../datas/2005-2006-day-001.txt)

--fromdate FROMDATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default: )

--todate TODATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default: )

--cerebro kwargs kwargs in key=value format (default: )

--broker kwargs kwargs in key=value format (default: )

--sizer kwargs kwargs in key=value format (default: )

--strat kwargs kwargs in key=value format (default: )

--plot [kwargs] kwargs in key=value format (default: )

--renko kwargs kwargs in key=value format (default: )

--dual put the filter on a second version of the data

(default: False)

Sample Code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import backtrader as bt

class St(bt.Strategy):

params = dict(

)

def __init__(self):

for d in self.datas:

bt.ind.RSI(d)

def next(self):

pass

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

# Data feed kwargs

kwargs = dict()

# Parse from/to-date

dtfmt, tmfmt = '%Y-%m-%d', 'T%H:%M:%S'

for a, d in ((getattr(args, x), x) for x in ['fromdate', 'todate']):

if a:

strpfmt = dtfmt + tmfmt * ('T' in a)

kwargs[d] = datetime.datetime.strptime(a, strpfmt)

data0 = bt.feeds.BacktraderCSVData(dataname=args.data0, **kwargs)

fkwargs = dict()

fkwargs.update(**eval('dict(' + args.renko + ')'))

if not args.dual:

data0.addfilter(bt.filters.Renko, **fkwargs)

cerebro.adddata(data0)

else:

cerebro.adddata(data0)

data1 = data0.clone()

data1.addfilter(bt.filters.Renko, **fkwargs)

cerebro.adddata(data1)

# Broker

cerebro.broker = bt.brokers.BackBroker(**eval('dict(' + args.broker + ')'))

# Sizer

cerebro.addsizer(bt.sizers.FixedSize, **eval('dict(' + args.sizer + ')'))

# Strategy

cerebro.addstrategy(St, **eval('dict(' + args.strat + ')'))

# Execute

kwargs = dict(stdstats=False)

kwargs.update(**eval('dict(' + args.cerebro + ')'))

cerebro.run(**kwargs)

if args.plot: # Plot if requested to

kwargs = dict(style='candle')

kwargs.update(**eval('dict(' + args.plot + ')'))

cerebro.plot(**kwargs)

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description=(

'Renko bricks sample'

)

)

parser.add_argument('--data0', default='../../datas/2005-2006-day-001.txt',

required=False, help='Data to read in')

# Defaults for dates

parser.add_argument('--fromdate', required=False, default='',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--todate', required=False, default='',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--cerebro', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--broker', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--sizer', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--strat', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--plot', required=False, default='',

nargs='?', const='{}',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--renko', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--dual', required=False, action='store_true',

help='put the filter on a second version of the data')

return parser.parse_args(pargs)

if __name__ == '__main__':

runstrat()