Data - Replay

The time is gone and testing a strategy against a fully formed and closed bar is good, but it could be better.

This is where Data Replay comes in to help. If:

- The strategy operates on data with a timeframe X (example: daily)

and

- Data for a smaller timeframe Y (example: 1 minute) is available

Data replay does exactly what the name implies:

Replay a daily bar using the 1 minute data

This is of course not exactly how the market developed, but it is far better than looking at the daily fully formed and closed bar in isolation:

If the strategy operates in realtime during the formation of the daily bar,

the approximation of the formation of the bar gives a chance to replicate the

actual behavior of the strategy under real conditions

Putting Data Replay into action follows the regular usage patterns of

backtrader

-

Load a data feed

-

Pass the data to

DataReplayerwhich is yet another data feed that will work on the loaded data feed -

Pass the new data feed to cerebro

-

Add a strategy

-

And run … WITH PRELOAD DISABLED*

Note

Preloading cannot be supported when data is being replayed because each bar is actually built in real-time.

For the sake of working with a example the standard 2006 daily data will be replayed on a weekly basis. Which means:

-

There will finally be 52 bars, one for each week

-

Cerebro will call

prenextandnexta total of 255 times, which is the original count of daily bars

The trick:

-

When a weekly bar is forming, the length (

len(self)) of the strategy will remain unchanged. -

With each new week the length will increase by one

Some examples below, but first the sauce of the test script in which the data is

loaded and passed to a replayer … and run with preload=False to

disable preloading (COMPULSORY)

dataname=datapath)

tframes = dict(

daily=bt.TimeFrame.Days,

weekly=bt.TimeFrame.Weeks,

monthly=bt.TimeFrame.Months)

# Handy dictionary for the argument timeframe conversion

# Resample the data

data_replayed = bt.DataReplayer(

dataname=data,

timeframe=tframes[args.timeframe],

compression=args.compression)

# First add the original data - smaller timeframe

cerebro.adddata(data_replayed)

# Run over everything

cerebro.run(preload=False)

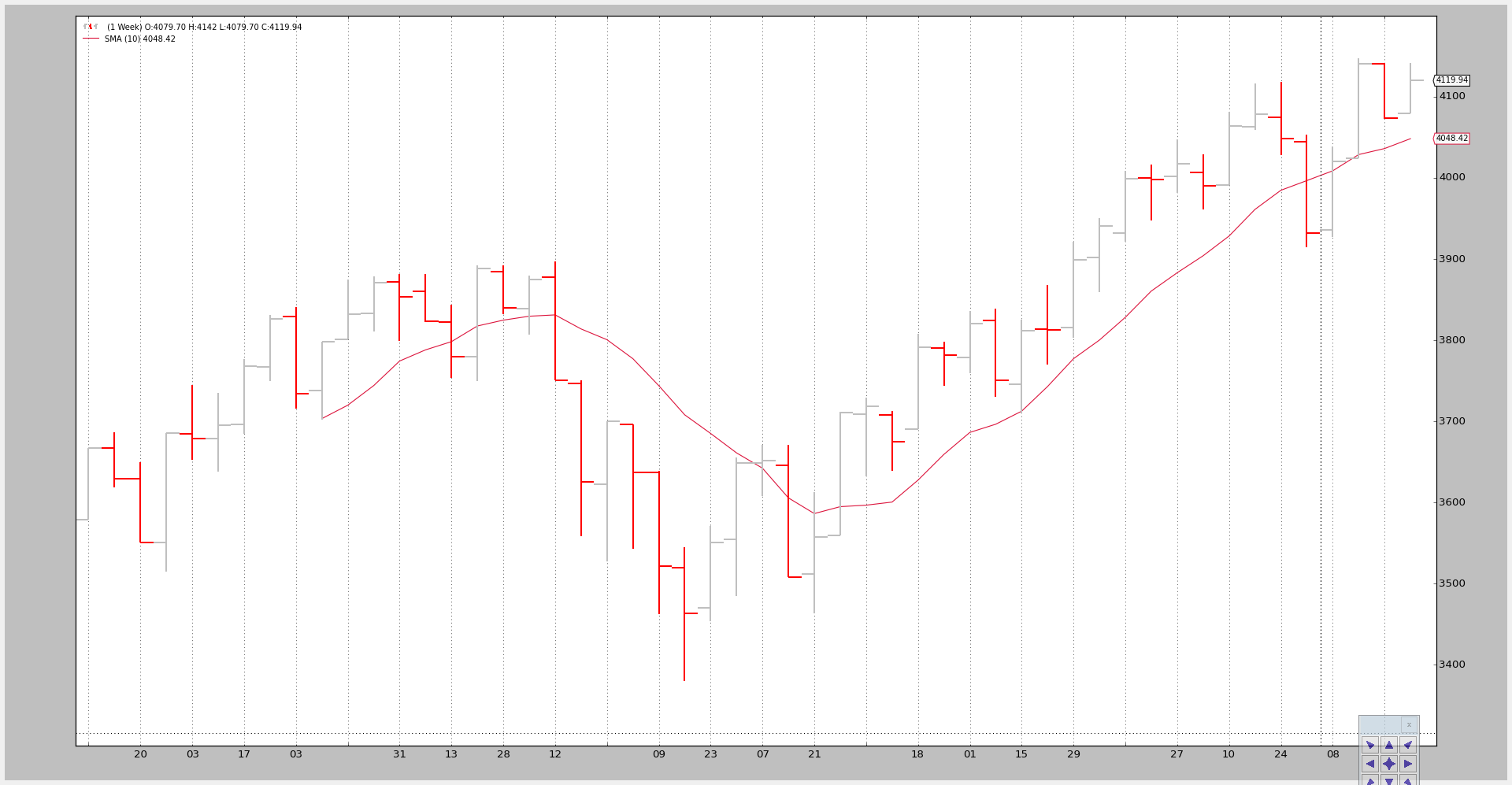

Example - Replay Daily to Weekly

The invocation of the script:

$ ./data-replay.py --timeframe weekly --compression 1

The chart cannot unfortunately show us the real thing happening in the background, so let’s have a look at the console output:

prenext len 1 - counter 1

prenext len 1 - counter 2

prenext len 1 - counter 3

prenext len 1 - counter 4

prenext len 1 - counter 5

prenext len 2 - counter 6

...

...

prenext len 9 - counter 44

prenext len 9 - counter 45

---next len 10 - counter 46

---next len 10 - counter 47

---next len 10 - counter 48

---next len 10 - counter 49

---next len 10 - counter 50

---next len 11 - counter 51

---next len 11 - counter 52

---next len 11 - counter 53

...

...

---next len 51 - counter 248

---next len 51 - counter 249

---next len 51 - counter 250

---next len 51 - counter 251

---next len 51 - counter 252

---next len 52 - counter 253

---next len 52 - counter 254

---next len 52 - counter 255

As we see the internal self.counter variable is keeping track of each call

to either prenext or next. The former being called before the applied

Simple Moving Average produces a value. The latter called when the Simple Moving

Average is producing values.

The key:

- The length (len(self)) of the strategy changes every 5 bars (5 trading days in the week)

The strategy is effectively seeing:

-

How the weekly bar developed in 5 shots.

This, again, doesn’t replicate the actual tick-by-tick (and not even minute, hour) development of the market, but it is better than actually seeing a bar.

The visual output is that of the weekly chart which is the final outcome the system is being tested again.

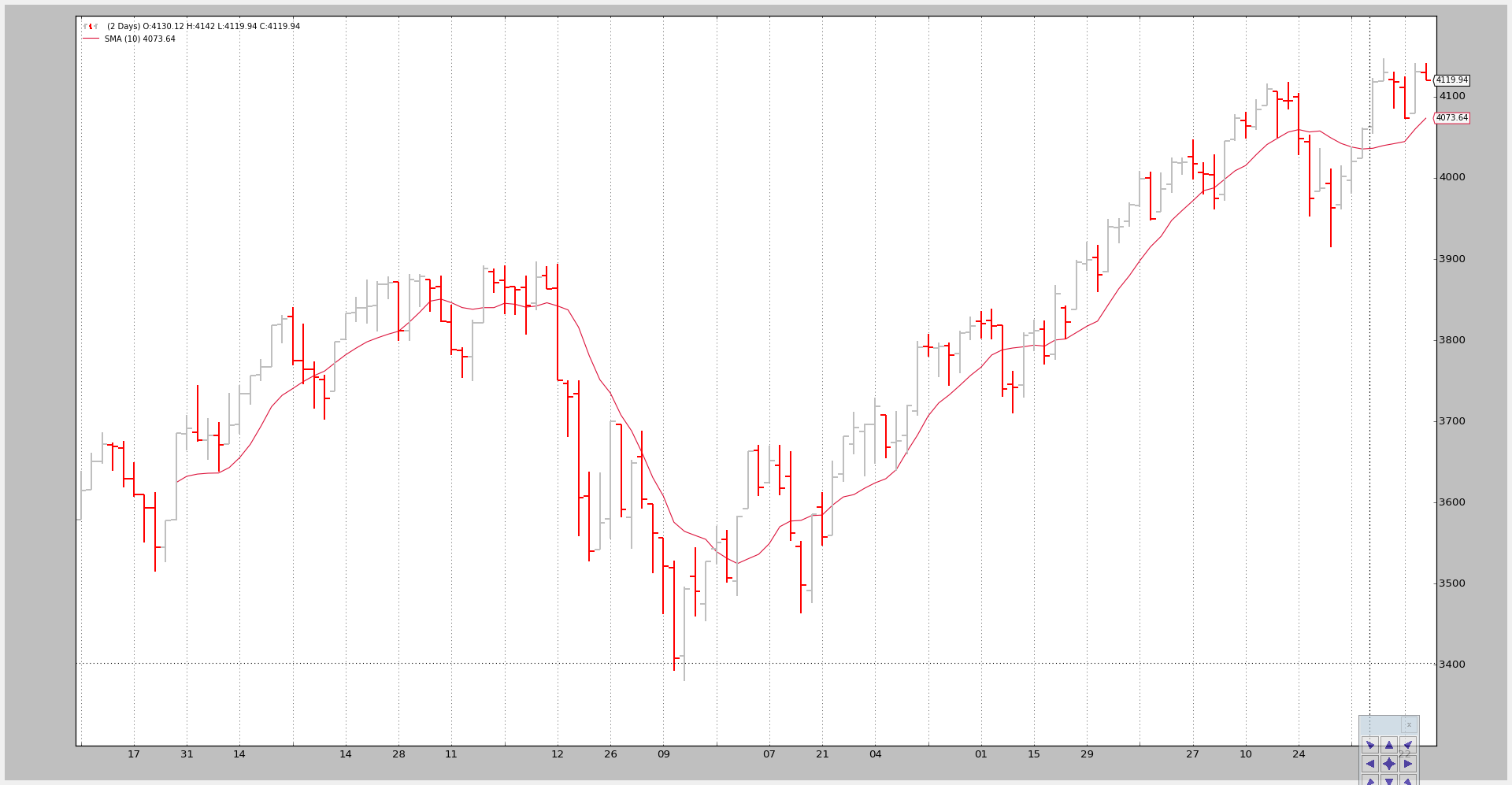

Example 2 - Daily to Daily with Compression

Of course “Replaying” can be applied to the same timeframe but with a compression.

The console:

$ ./data-replay.py --timeframe daily --compression 2

prenext len 1 - counter 1

prenext len 1 - counter 2

prenext len 2 - counter 3

prenext len 2 - counter 4

prenext len 3 - counter 5

prenext len 3 - counter 6

prenext len 4 - counter 7

...

...

---next len 125 - counter 250

---next len 126 - counter 251

---next len 126 - counter 252

---next len 127 - counter 253

---next len 127 - counter 254

---next len 128 - counter 255

This time we got half the bars as expected because of the factor 2 requested compression.

The chart:

Conclusion

A reconstruction of the market development is possible. Usually a smaller timeframe set of data is available and can be used to discretely replay the timeframe which the system operates on.

The test script.

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

class SMAStrategy(bt.Strategy):

params = (

('period', 10),

('onlydaily', False),

)

def __init__(self):

self.sma = btind.SMA(self.data, period=self.p.period)

def start(self):

self.counter = 0

def prenext(self):

self.counter += 1

print('prenext len %d - counter %d' % (len(self), self.counter))

def next(self):

self.counter += 1

print('---next len %d - counter %d' % (len(self), self.counter))

def runstrat():

args = parse_args()

# Create a cerebro entity

cerebro = bt.Cerebro(stdstats=False)

cerebro.addstrategy(

SMAStrategy,

# args for the strategy

period=args.period,

)

# Load the Data

datapath = args.dataname or '../datas/sample/2006-day-001.txt'

data = btfeeds.BacktraderCSVData(

dataname=datapath)

tframes = dict(

daily=bt.TimeFrame.Days,

weekly=bt.TimeFrame.Weeks,

monthly=bt.TimeFrame.Months)

# Handy dictionary for the argument timeframe conversion

# Resample the data

data_replayed = bt.DataReplayer(

dataname=data,

timeframe=tframes[args.timeframe],

compression=args.compression)

# First add the original data - smaller timeframe

cerebro.adddata(data_replayed)

# Run over everything

cerebro.run(preload=False)

# Plot the result

cerebro.plot(style='bar')

def parse_args():

parser = argparse.ArgumentParser(

description='Pandas test script')

parser.add_argument('--dataname', default='', required=False,

help='File Data to Load')

parser.add_argument('--timeframe', default='weekly', required=False,

choices=['daily', 'weekly', 'monhtly'],

help='Timeframe to resample to')

parser.add_argument('--compression', default=1, required=False, type=int,

help='Compress n bars into 1')

parser.add_argument('--period', default=10, required=False, type=int,

help='Period to apply to indicator')

return parser.parse_args()

if __name__ == '__main__':

runstrat()