MultiTrades

One can now add a unique identifier to each trade, even if running on the same data.

Following a request at Tick Data and Resampling

release 1.1.12.88 of backtrader support “MultiTrades”, ie: the ability to

assign a tradeid to orders. This id is passed on to Trades which makes

it possible to have different categories of trades and have them simultaneously

open.

The tradeid can be specified when:

-

Calling Strategy.buy/sell/close with kwarg

tradeid -

Calling Broker.buy/sell with kwarg

tradeid -

Creating an Order instance with kwarg

tradeid

If not specified the default value is:

tradeid = 0

To test a small script has been implemented, visualizing the result with the

implementation of a custom MTradeObserver which assigns different markers on

the plot according tradeid (for the test values 0, 1 and 2 are used)

The script supports using the three ids (0, 1, 2) or simply use 0 (default)

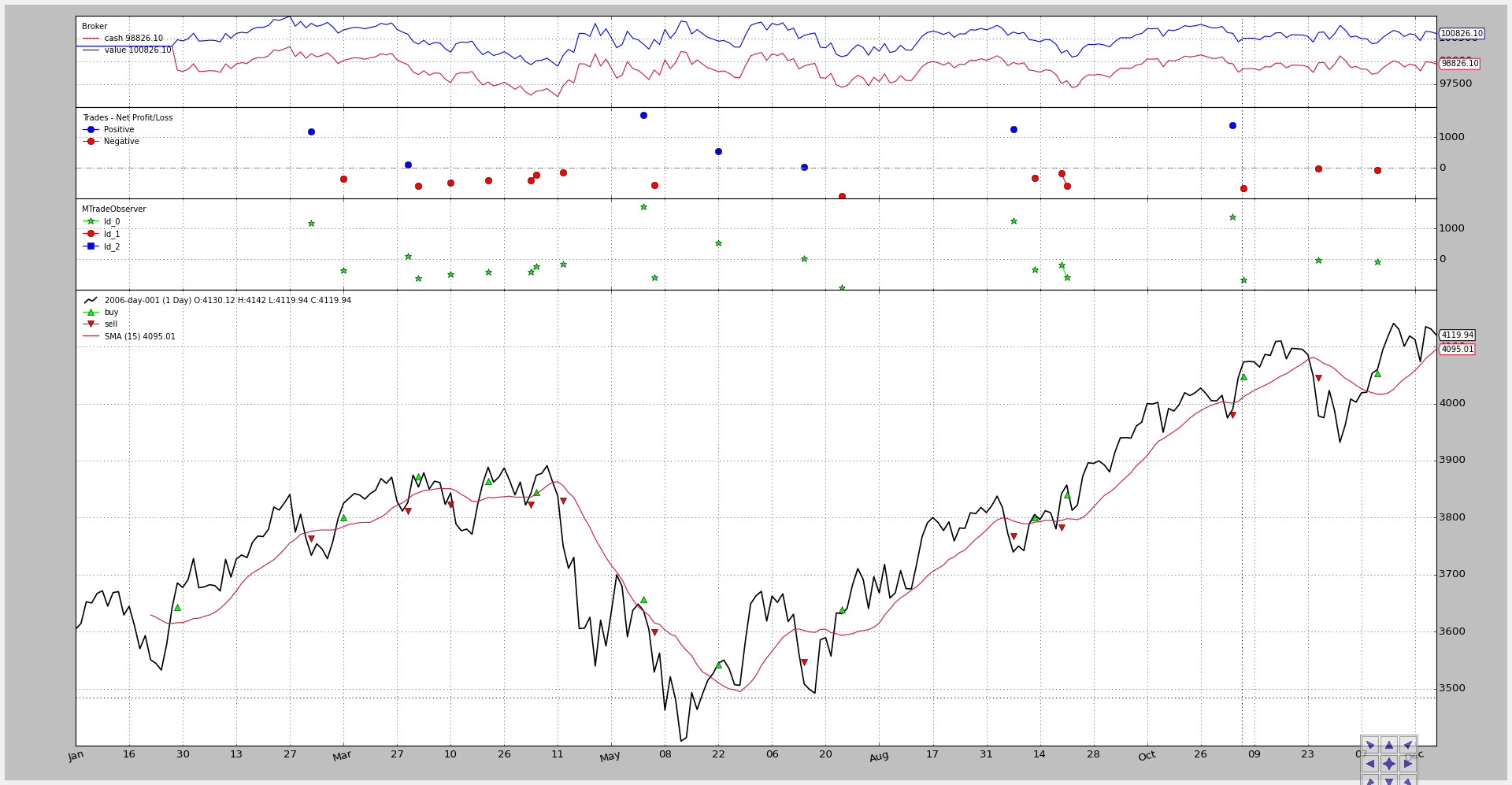

An execution without enabling multiple ids:

$ ./multitrades.py --plot

With the resulting chart showing all Trades carry id 0 and therefore cannot

be diferentiated.

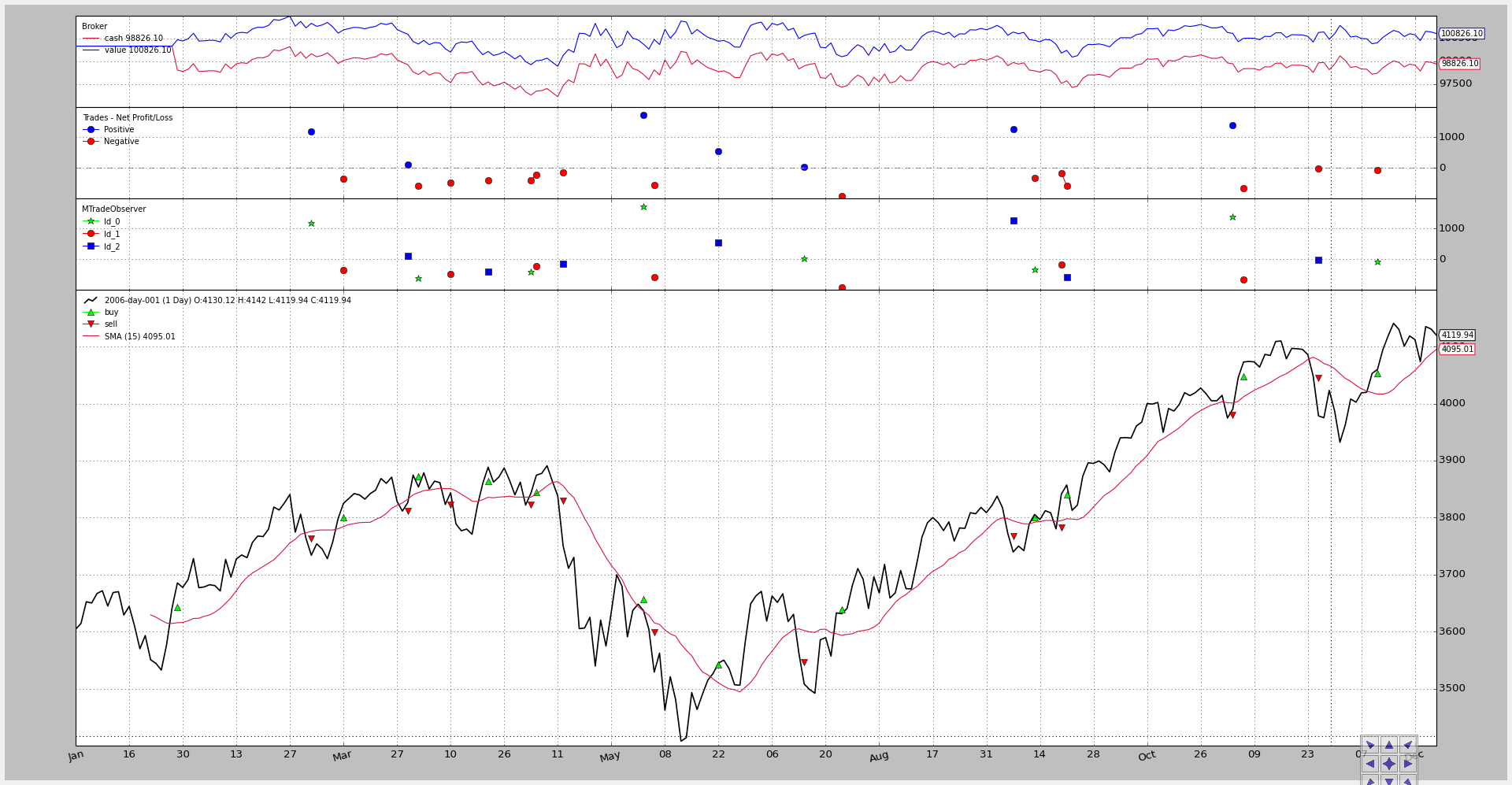

A second execution enables multitrades by cycling amongs 0, 1 and 2:

$ ./multitrades.py --plot --mtrade

And now 3 different markers alternate showing each Trade can be distinguished

using the tradeid member.

Note

backtrader tries to use models which mimic reality. Therefore “trades”

are not calculated by the Broker instance which only takes care of

oders.

Trades are calculated by the Strategy.

And hence tradeid (or something similar) may not be supported by a real

life broker in which case manually keeping track of the unique orde id

assigned by the broker would be needed.

Now, the code for the custom observer

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import math

import backtrader as bt

class MTradeObserver(bt.observer.Observer):

lines = ('Id_0', 'Id_1', 'Id_2')

plotinfo = dict(plot=True, subplot=True, plotlinelabels=True)

plotlines = dict(

Id_0=dict(marker='*', markersize=8.0, color='lime', fillstyle='full'),

Id_1=dict(marker='o', markersize=8.0, color='red', fillstyle='full'),

Id_2=dict(marker='s', markersize=8.0, color='blue', fillstyle='full')

)

def next(self):

for trade in self._owner._tradespending:

if trade.data is not self.data:

continue

if not trade.isclosed:

continue

self.lines[trade.tradeid][0] = trade.pnlcomm

The main script usage:

$ ./multitrades.py --help

usage: multitrades.py [-h] [--data DATA] [--fromdate FROMDATE]

[--todate TODATE] [--mtrade] [--period PERIOD]

[--onlylong] [--cash CASH] [--comm COMM] [--mult MULT]

[--margin MARGIN] [--stake STAKE] [--plot]

[--numfigs NUMFIGS]

MultiTrades

optional arguments:

-h, --help show this help message and exit

--data DATA, -d DATA data to add to the system

--fromdate FROMDATE, -f FROMDATE

Starting date in YYYY-MM-DD format

--todate TODATE, -t TODATE

Starting date in YYYY-MM-DD format

--mtrade Activate MultiTrade Ids

--period PERIOD Period to apply to the Simple Moving Average

--onlylong, -ol Do only long operations

--cash CASH Starting Cash

--comm COMM Commission for operation

--mult MULT Multiplier for futures

--margin MARGIN Margin for each future

--stake STAKE Stake to apply in each operation

--plot, -p Plot the read data

--numfigs NUMFIGS, -n NUMFIGS

Plot using numfigs figures

The code for the script.

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import itertools

# The above could be sent to an independent module

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

import mtradeobserver

class MultiTradeStrategy(bt.Strategy):

'''This strategy buys/sells upong the close price crossing

upwards/downwards a Simple Moving Average.

It can be a long-only strategy by setting the param "onlylong" to True

'''

params = dict(

period=15,

stake=1,

printout=False,

onlylong=False,

mtrade=False,

)

def log(self, txt, dt=None):

if self.p.printout:

dt = dt or self.data.datetime[0]

dt = bt.num2date(dt)

print('%s, %s' % (dt.isoformat(), txt))

def __init__(self):

# To control operation entries

self.order = None

# Create SMA on 2nd data

sma = btind.MovAv.SMA(self.data, period=self.p.period)

# Create a CrossOver Signal from close an moving average

self.signal = btind.CrossOver(self.data.close, sma)

# To alternate amongst different tradeids

if self.p.mtrade:

self.tradeid = itertools.cycle([0, 1, 2])

else:

self.tradeid = itertools.cycle([0])

def next(self):

if self.order:

return # if an order is active, no new orders are allowed

if self.signal > 0.0: # cross upwards

if self.position:

self.log('CLOSE SHORT , %.2f' % self.data.close[0])

self.close(tradeid=self.curtradeid)

self.log('BUY CREATE , %.2f' % self.data.close[0])

self.curtradeid = next(self.tradeid)

self.buy(size=self.p.stake, tradeid=self.curtradeid)

elif self.signal < 0.0:

if self.position:

self.log('CLOSE LONG , %.2f' % self.data.close[0])

self.close(tradeid=self.curtradeid)

if not self.p.onlylong:

self.log('SELL CREATE , %.2f' % self.data.close[0])

self.curtradeid = next(self.tradeid)

self.sell(size=self.p.stake, tradeid=self.curtradeid)

def notify_order(self, order):

if order.status in [bt.Order.Submitted, bt.Order.Accepted]:

return # Await further notifications

if order.status == order.Completed:

if order.isbuy():

buytxt = 'BUY COMPLETE, %.2f' % order.executed.price

self.log(buytxt, order.executed.dt)

else:

selltxt = 'SELL COMPLETE, %.2f' % order.executed.price

self.log(selltxt, order.executed.dt)

elif order.status in [order.Expired, order.Canceled, order.Margin]:

self.log('%s ,' % order.Status[order.status])

pass # Simply log

# Allow new orders

self.order = None

def notify_trade(self, trade):

if trade.isclosed:

self.log('TRADE PROFIT, GROSS %.2f, NET %.2f' %

(trade.pnl, trade.pnlcomm))

elif trade.justopened:

self.log('TRADE OPENED, SIZE %2d' % trade.size)

def runstrategy():

args = parse_args()

# Create a cerebro

cerebro = bt.Cerebro()

# Get the dates from the args

fromdate = datetime.datetime.strptime(args.fromdate, '%Y-%m-%d')

todate = datetime.datetime.strptime(args.todate, '%Y-%m-%d')

# Create the 1st data

data = btfeeds.BacktraderCSVData(

dataname=args.data,

fromdate=fromdate,

todate=todate)

# Add the 1st data to cerebro

cerebro.adddata(data)

# Add the strategy

cerebro.addstrategy(MultiTradeStrategy,

period=args.period,

onlylong=args.onlylong,

stake=args.stake,

mtrade=args.mtrade)

# Add the commission - only stocks like a for each operation

cerebro.broker.setcash(args.cash)

# Add the commission - only stocks like a for each operation

cerebro.broker.setcommission(commission=args.comm,

mult=args.mult,

margin=args.margin)

# Add the MultiTradeObserver

cerebro.addobserver(mtradeobserver.MTradeObserver)

# And run it

cerebro.run()

# Plot if requested

if args.plot:

cerebro.plot(numfigs=args.numfigs, volume=False, zdown=False)

def parse_args():

parser = argparse.ArgumentParser(description='MultiTrades')

parser.add_argument('--data', '-d',

default='../../datas/2006-day-001.txt',

help='data to add to the system')

parser.add_argument('--fromdate', '-f',

default='2006-01-01',

help='Starting date in YYYY-MM-DD format')

parser.add_argument('--todate', '-t',

default='2006-12-31',

help='Starting date in YYYY-MM-DD format')

parser.add_argument('--mtrade', action='store_true',

help='Activate MultiTrade Ids')

parser.add_argument('--period', default=15, type=int,

help='Period to apply to the Simple Moving Average')

parser.add_argument('--onlylong', '-ol', action='store_true',

help='Do only long operations')

parser.add_argument('--cash', default=100000, type=int,

help='Starting Cash')

parser.add_argument('--comm', default=2, type=float,

help='Commission for operation')

parser.add_argument('--mult', default=10, type=int,

help='Multiplier for futures')

parser.add_argument('--margin', default=2000.0, type=float,

help='Margin for each future')

parser.add_argument('--stake', default=1, type=int,

help='Stake to apply in each operation')

parser.add_argument('--plot', '-p', action='store_true',

help='Plot the read data')

parser.add_argument('--numfigs', '-n', default=1,

help='Plot using numfigs figures')

return parser.parse_args()

if __name__ == '__main__':

runstrategy()