Data Resampling

When data is only available in a single timeframe and the analysis has to be done for a different timeframe, it’s time to do some resampling.

“Resampling” should actually be called “Upsampling” given that one goes from a source timeframe to a larger time frame (for example: days to weeks)

“Downsampling” is not yet possible.

backtrader has built-in support for resampling by passing the original data

through a filter object which has intelligently been named: DataResampler.

The class has two functionalities:

-

Change the timeframe

-

Compress bars

To do so the DataResampler uses standard feed.DataBase parameters during

construction:

-

timeframe(default: bt.TimeFrame.Days)Destination timeframe which to be useful has to be equal or larger than the source

-

compression(default: 1)Compress the selected value “n” to 1 bar

Let’s see an example from Daily to weekly with a handcrafted script:

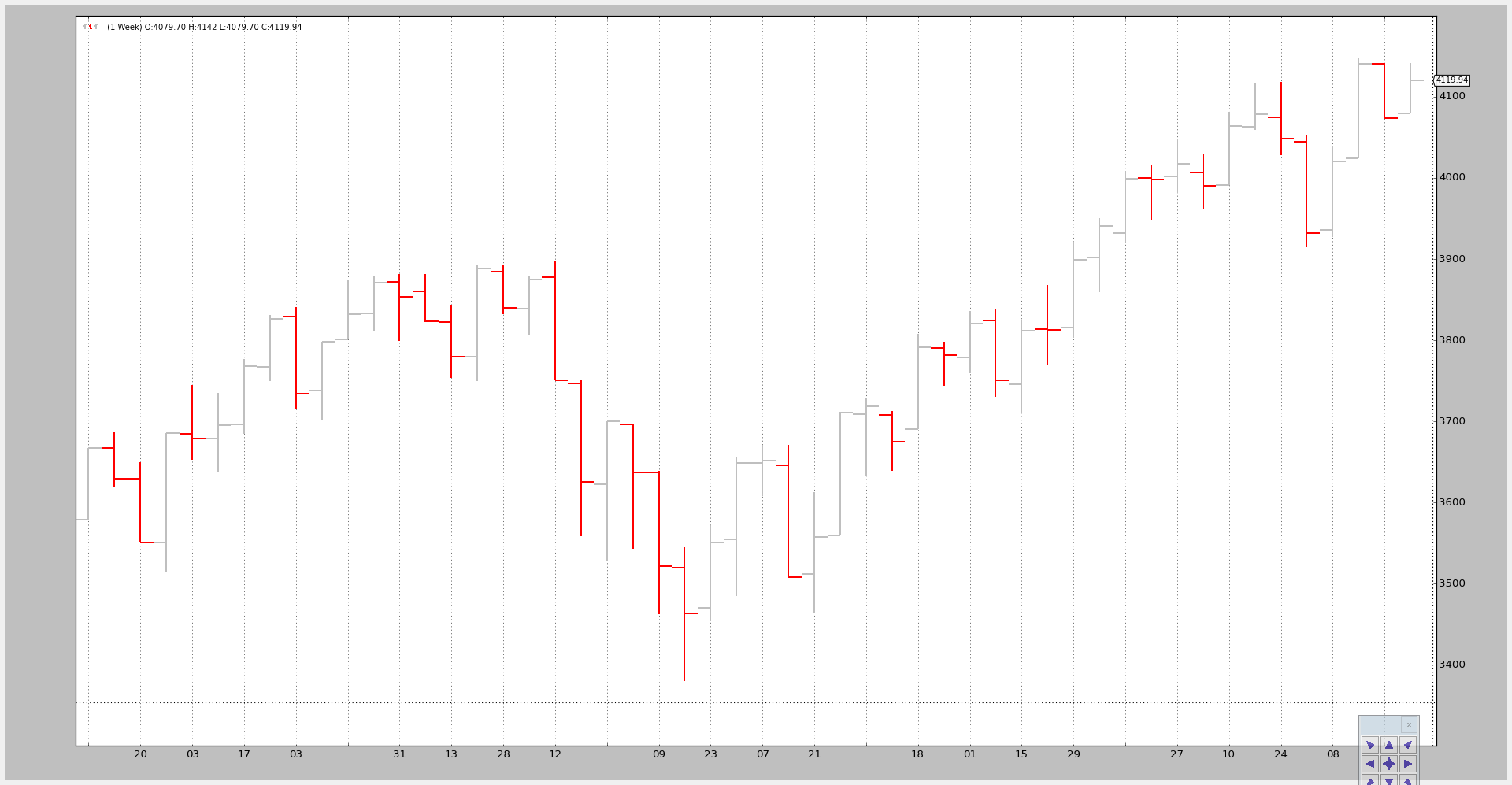

$ ./data-resampling.py --timeframe weekly --compression 1

The output:

We can compare it to the original daily data:

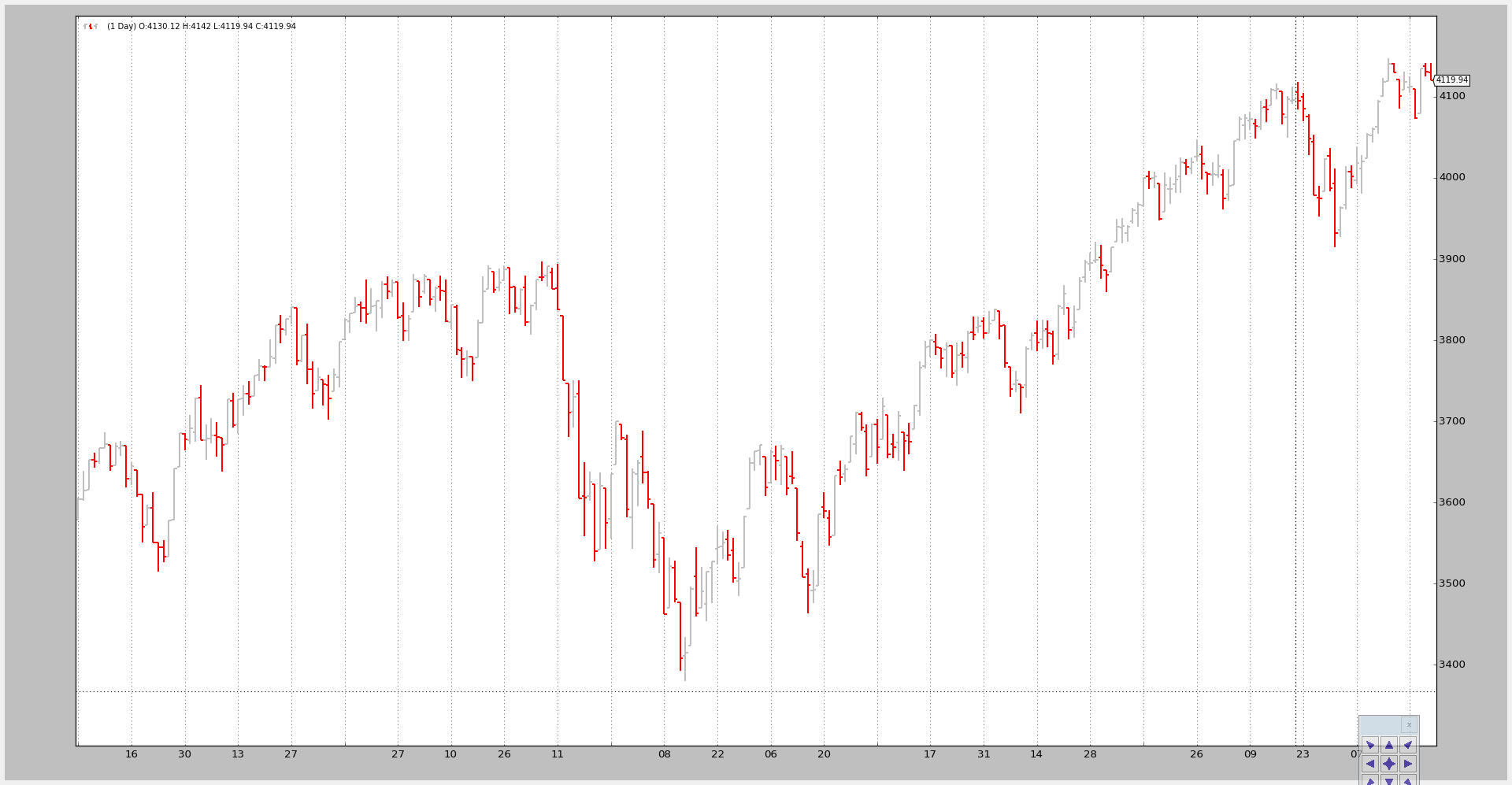

$ ./data-resampling.py --timeframe daily --compression 1

The output:

The magic is done by executing the following steps:

-

Loading the data as usual

-

Feeding the data into a

DataResamplerwith the desired-

timeframe

-

compression

-

The code in the sample (the entire script at the bottom).

# Load the Data

datapath = args.dataname or '../datas/sample/2006-day-001.txt'

data = btfeeds.BacktraderCSVData(

dataname=datapath)

# Handy dictionary for the argument timeframe conversion

tframes = dict(

daily=bt.TimeFrame.Days,

weekly=bt.TimeFrame.Weeks,

monthly=bt.TimeFrame.Months)

# Resample the data

data_resampled = bt.DataResampler(

dataname=data,

timeframe=tframes[args.timeframe],

compression=args.compression)

# Add the resample data instead of the original

cerebro.adddata(data_resampled)

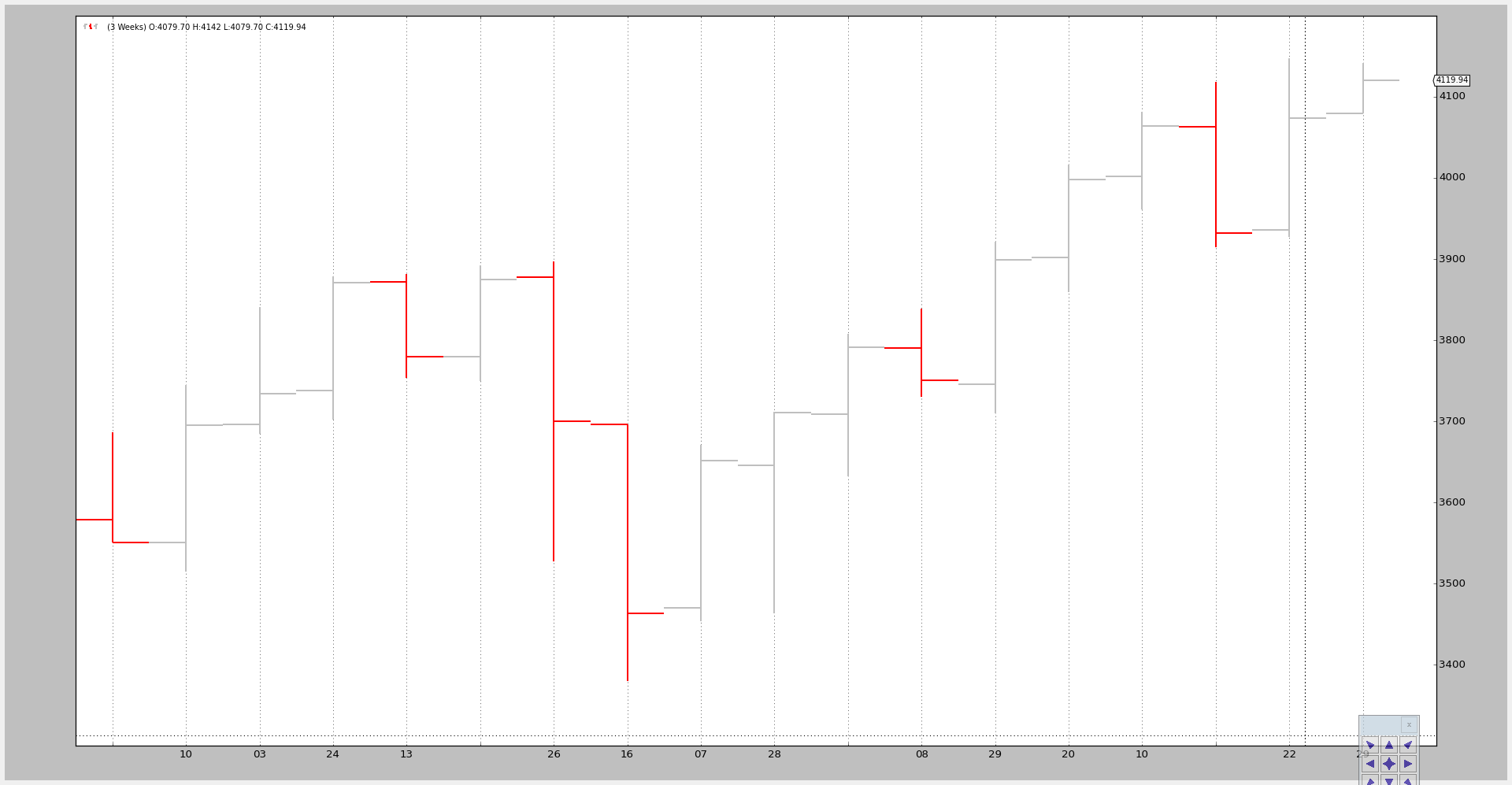

A last example in which we first change the time frame from daily to weekly and then apply a 3 to 1 compression:

$ ./data-resampling.py --timeframe weekly --compression 3

The output:

From the original 256 daily bars we end up with 18 3-week bars. The breakdown:

-

52 weeks

-

52 / 3 = 17.33 and therefore 18 bars

It doesn’t take much more. Of course intraday data can also be resampled.

The sample code for the resampling test script.

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import backtrader as bt

import backtrader.feeds as btfeeds

def runstrat():

args = parse_args()

# Create a cerebro entity

cerebro = bt.Cerebro(stdstats=False)

# Add a strategy

cerebro.addstrategy(bt.Strategy)

# Load the Data

datapath = args.dataname or '../datas/sample/2006-day-001.txt'

data = btfeeds.BacktraderCSVData(

dataname=datapath)

# Handy dictionary for the argument timeframe conversion

tframes = dict(

daily=bt.TimeFrame.Days,

weekly=bt.TimeFrame.Weeks,

monthly=bt.TimeFrame.Months)

# Resample the data

data_resampled = bt.DataResampler(

dataname=data,

timeframe=tframes[args.timeframe],

compression=args.compression)

# Add the resample data instead of the original

cerebro.adddata(data_resampled)

# Run over everything

cerebro.run()

# Plot the result

cerebro.plot(style='bar')

def parse_args():

parser = argparse.ArgumentParser(

description='Pandas test script')

parser.add_argument('--dataname', default='', required=False,

help='File Data to Load')

parser.add_argument('--timeframe', default='weekly', required=False,

choices=['daily', 'weekly', 'monhtly'],

help='Timeframe to resample to')

parser.add_argument('--compression', default=1, required=False, type=int,

help='Compress n bars into 1')

return parser.parse_args()

if __name__ == '__main__':

runstrat()