BTFD - Reality Bites

The previous post managed to replicate the BTFD strategy, finding out that

the real gains were 16x rather than 31x.

But as pointed out during the replication:

-

No commission was charged

-

No interest was charged for using a

2xleverage

And that raises the obvious question:

- How much of that 16x will be there when commission and interest are charged?

Luckily the previous sample is flexible enough to experiment with it. To have some visual feedback and verification, the following code will be added to the strategy

def start(self):

print(','.join(['TRADE', 'STATUS', 'Value', 'PNL', 'COMMISSION']))

def notify_order(self, order):

if order.status in [order.Margin]:

print('ORDER FAILED with status:', order.getstatusname())

def notify_trade(self, trade):

if trade.isclosed:

print(','.join(map(str, [

'TRADE', 'CLOSE',

self.data.num2date(trade.dtclose).date().isoformat(),

trade.value,

trade.pnl,

trade.commission,

]

)))

elif trade.justopened:

print(','.join(map(str, [

'TRADE', 'OPEN',

self.data.num2date(trade.dtopen).date().isoformat(),

trade.value,

trade.pnl,

trade.commission,

]

)))

It’s all about the following:

-

Seeing how trades are opened and closed (value, profit and loss, value and commission)

-

Providing feedback if an order is being rejected with

Margindue to insufficient fundsNote

Because there will be an adjustment of the amount of money to invest, to leave room for commission, some orders could not be accepted by the broker. This visual feedback allows identifying the situation

Verification

First a quick test to see that some orders are not accepted.

$ ./btfd.py --comminfo commission=0.001,leverage=2.0 --strat target=1.0

TRADE,STATUS,Value,PNL,COMMISSION

ORDER FAILED with status: Margin

ORDER FAILED with status: Margin

TRADE,OPEN,1990-01-08,199345.2,0.0,199.3452

TRADE,CLOSE,1990-01-10,0.0,-1460.28,397.23012

Notice:

-

We apply

target=1.0which means: try to invest 100% of the capital. This is the default, but it is there as a reference. -

commission=0.001or0.1%to ensure we will sometimes meet the margin -

The 1st two orders are rejected with

Margin -

The 3rd order is accepted. This is not an error. The system tries to invest

100%of the capital, but the asset has a price and this is used to calculate the size of the stake. Size is rounded down from the actual result of calculating the potential size from the actual available cash. This rounding down has left room enough for the commission with this 3rd order. -

The trade notifications (

OPENandCLOSE) show the opening commission and the final total commission an the value which is close to200k, showing the2xleverage in action.The opening commission is

199.3452which is0.1%of the leveraged value which is:199,345.2

The remaining tests will be made with target=0.99x where x will ensure

room enough for the selected commission.

Reality Bites

Let’s go for some real examples

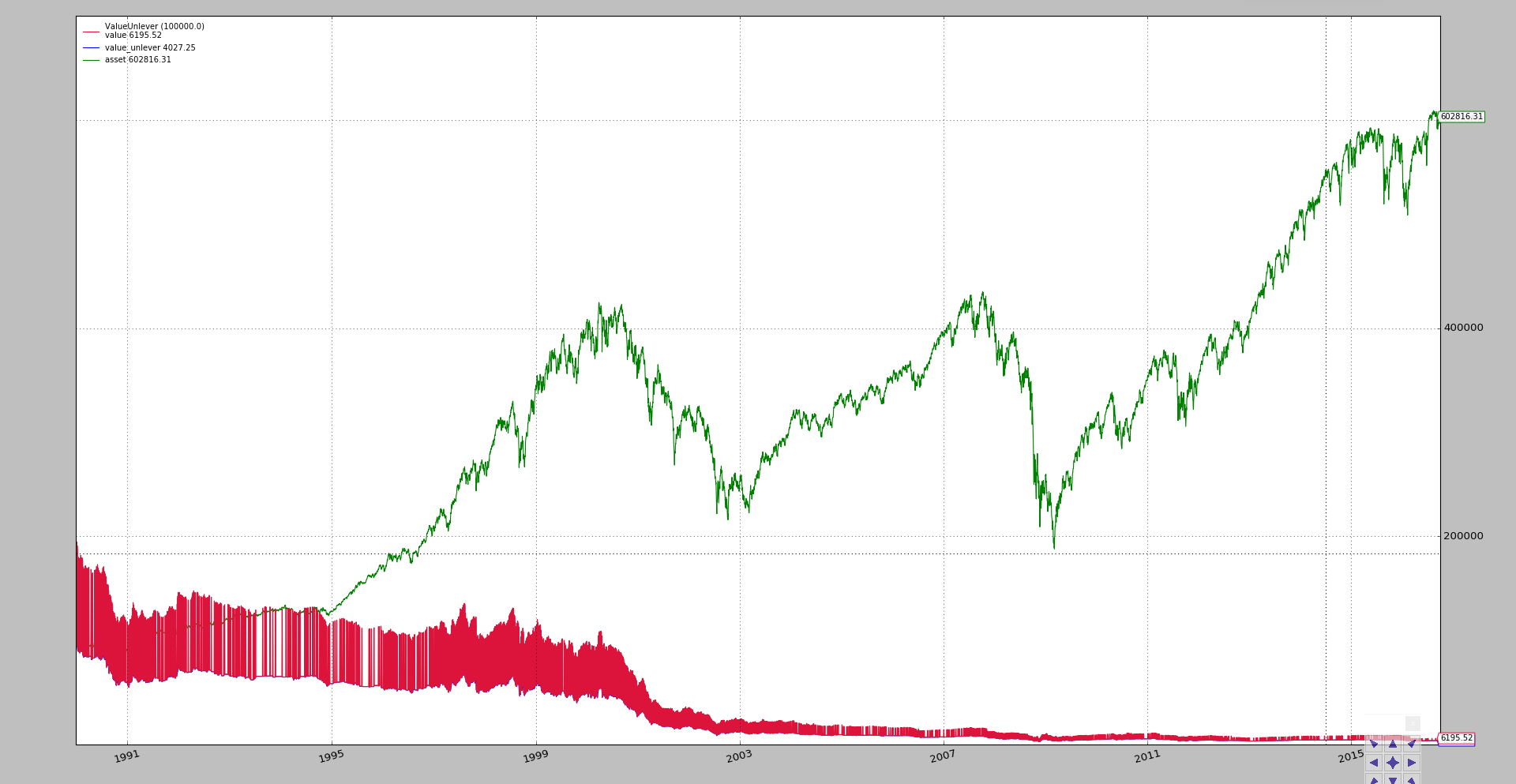

Target 99.8% - Commission 0.1%

./btfd.py --comminfo commission=0.001,leverage=2.0 --strat target=0.998 --plot

Blistering Barnacles!!! Not only is the BTFD strategy by no means close to

the 16x gains: IT LOSES MOST OF THE MONEY.

- From

100,000down to roughly4,027

Note

The down to value is the non-leveraged value, because this is the approximate value that will be back in the system when the position is closed

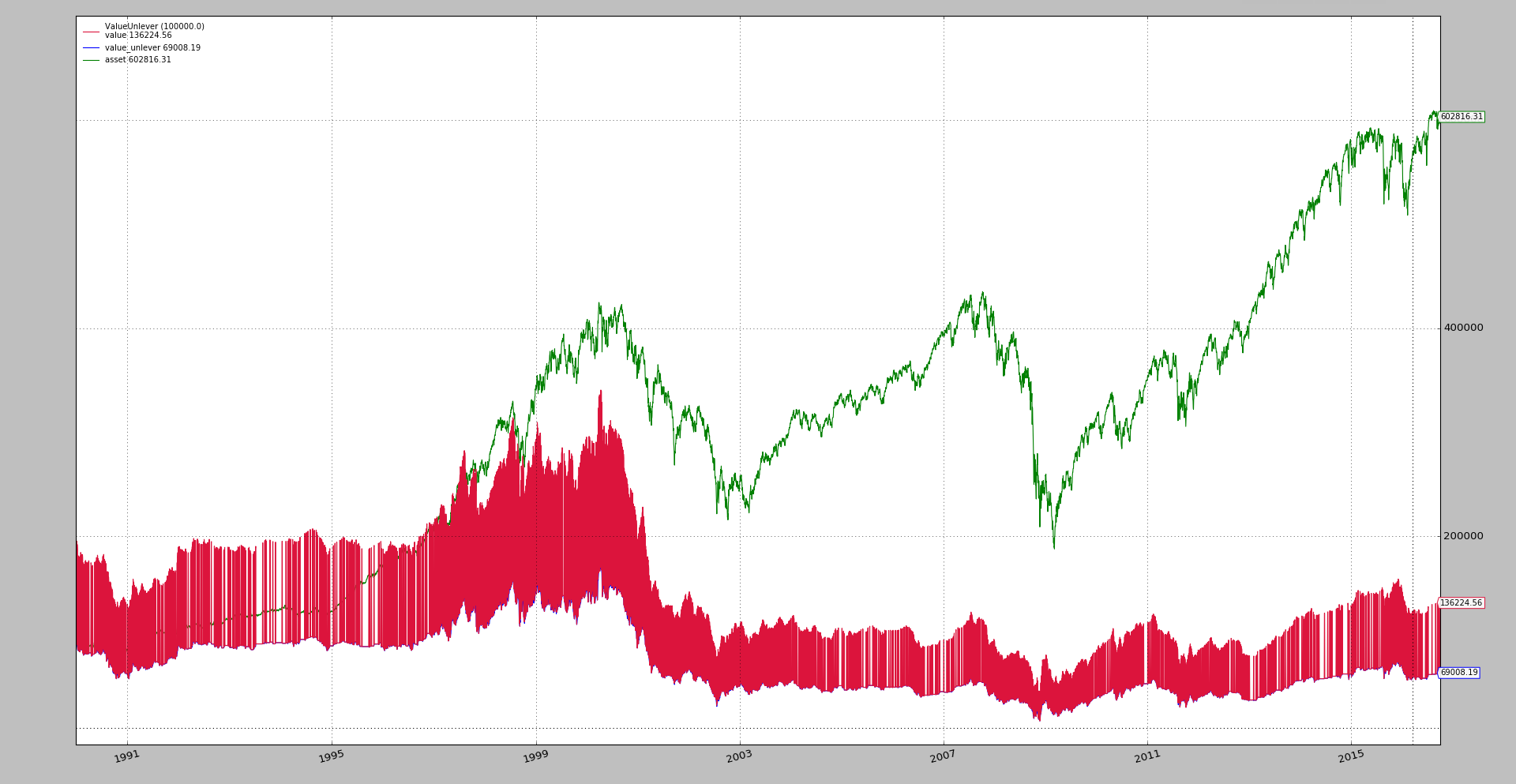

Target 99.9% - Commission 0.05%

It may well have been that the commission is too aggressive. Let’s go for half of it

./btfd.py --comminfo commission=0.0005,leverage=2.0 --strat target=0.999 --plot

NO, NO. The commission was not that aggressive, because the system still

loses money, going down from 100,000 down to around 69,000 (the

non-leverage value)

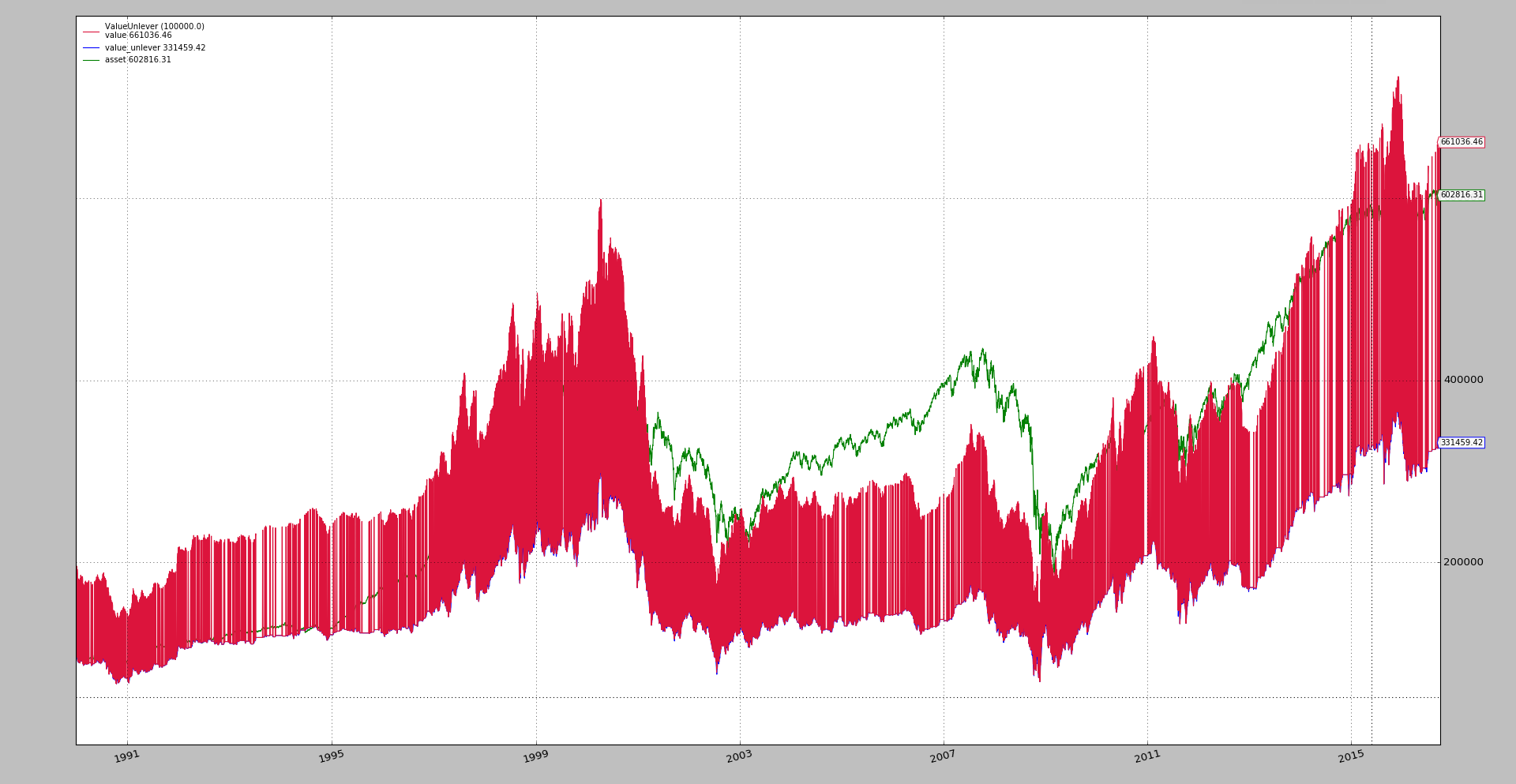

Target 99.95% - Commission 0.025%

Commission is divided by two again

./btfd.py --comminfo commission=0.00025,leverage=2.0 --strat target=0.9995 --plot

Finally the system makes money:

-

The initial

100,000are taken up to331,459for3xgains. -

But this doesn’t match the performance of the asset which has gone up to over

600k

Note

The sample accepts --fromdate YYYY-MM-DD and --todate YYYY-MM-DD to

select to which period the strategy has to be applied. This would allow

testing similar scenarios for different date ranges.

Conclusion

The 16x gains do not hold when confronted with commission. For the

commission offered by some brokers (no cap and %-based) one would need a very

good deal to make sure the system makes money.

And in this case in which the strategy is applied to the S&P500, the

BTFD strategy doesn’t match the performance of the index.

No interest rate has been applied. Using commissions is enough to see how far

away is 16x from any potential profits. In any case, a run with a 2%

interest rate would be executed like this

./btfd.py --comminfo commission=0.00025,leverage=2.0,interest=0.02,interest_long=True --strat target=0.9995 --plot

interest_long=True is needed, because the default behavior for charging

interest is to do it only for short positions

Sample usage

$ ./btfd.py --help

usage: btfd.py [-h] [--offline] [--data TICKER]

[--fromdate YYYY-MM-DD[THH:MM:SS]]

[--todate YYYY-MM-DD[THH:MM:SS]] [--cerebro kwargs]

[--broker kwargs] [--valobserver kwargs] [--strat kwargs]

[--comminfo kwargs] [--plot [kwargs]]

BTFD - http://dark-bid.com/BTFD-only-strategy-that-matters.html - https://www.

reddit.com/r/algotrading/comments/5jez2b/can_anyone_replicate_this_strategy/

optional arguments:

-h, --help show this help message and exit

--offline Use offline file with ticker name (default: False)

--data TICKER Yahoo ticker to download (default: ^GSPC)

--fromdate YYYY-MM-DD[THH:MM:SS]

Starting date[time] (default: 1990-01-01)

--todate YYYY-MM-DD[THH:MM:SS]

Ending date[time] (default: 2016-10-01)

--cerebro kwargs kwargs in key=value format (default: stdstats=False)

--broker kwargs kwargs in key=value format (default: cash=100000.0,

coc=True)

--valobserver kwargs kwargs in key=value format (default:

assetstart=100000.0)

--strat kwargs kwargs in key=value format (default:

approach="highlow")

--comminfo kwargs kwargs in key=value format (default: leverage=2.0)

--plot [kwargs] kwargs in key=value format (default: )

Sample Code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

# References:

# - https://www.reddit.com/r/algotrading/comments/5jez2b/can_anyone_replicate_this_strategy/

# - http://dark-bid.com/BTFD-only-strategy-that-matters.html

import argparse

import datetime

import backtrader as bt

class ValueUnlever(bt.observers.Value):

'''Extension of regular Value observer to add leveraged view'''

lines = ('value_lever', 'asset')

params = (('assetstart', 100000.0), ('lever', True),)

def next(self):

super(ValueUnlever, self).next()

if self.p.lever:

self.lines.value_lever[0] = self._owner.broker._valuelever

if len(self) == 1:

self.lines.asset[0] = self.p.assetstart

else:

change = self.data[0] / self.data[-1]

self.lines.asset[0] = change * self.lines.asset[-1]

class St(bt.Strategy):

params = (

('fall', -0.01),

('hold', 2),

('approach', 'highlow'),

('target', 1.0)

)

def __init__(self):

if self.p.approach == 'closeclose':

self.pctdown = self.data.close / self.data.close(-1) - 1.0

elif self.p.approach == 'openclose':

self.pctdown = self.data.close / self.data.open - 1.0

elif self.p.approach == 'highclose':

self.pctdown = self.data.close / self.data.high - 1.0

elif self.p.approach == 'highlow':

self.pctdown = self.data.low / self.data.high - 1.0

def next(self):

if self.position:

if len(self) == self.barexit:

self.close()

else:

if self.pctdown <= self.p.fall:

self.order_target_percent(target=self.p.target)

self.barexit = len(self) + self.p.hold

def start(self):

print(','.join(['TRADE', 'STATUS', 'Value', 'PNL', 'COMMISSION']))

def notify_order(self, order):

if order.status in [order.Margin, order.Rejected, order.Canceled]:

print('ORDER FAILED with status:', order.getstatusname())

def notify_trade(self, trade):

if trade.isclosed:

print(','.join(map(str, [

'TRADE', 'CLOSE',

self.data.num2date(trade.dtclose).date().isoformat(),

trade.value,

trade.pnl,

trade.commission,

]

)))

elif trade.justopened:

print(','.join(map(str, [

'TRADE', 'OPEN',

self.data.num2date(trade.dtopen).date().isoformat(),

trade.value,

trade.pnl,

trade.commission,

]

)))

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

# Data feed kwargs

kwargs = dict()

# Parse from/to-date

dtfmt, tmfmt = '%Y-%m-%d', 'T%H:%M:%S'

for a, d in ((getattr(args, x), x) for x in ['fromdate', 'todate']):

kwargs[d] = datetime.datetime.strptime(a, dtfmt + tmfmt * ('T' in a))

if not args.offline:

YahooData = bt.feeds.YahooFinanceData

else:

YahooData = bt.feeds.YahooFinanceCSVData

# Data feed - no plot - observer will do the job

data = YahooData(dataname=args.data, plot=False, **kwargs)

cerebro.adddata(data)

# Broker

cerebro.broker = bt.brokers.BackBroker(**eval('dict(' + args.broker + ')'))

# Add a commission

cerebro.broker.setcommission(**eval('dict(' + args.comminfo + ')'))

# Strategy

cerebro.addstrategy(St, **eval('dict(' + args.strat + ')'))

# Add specific observer

cerebro.addobserver(ValueUnlever, **eval('dict(' + args.valobserver + ')'))

# Execute

cerebro.run(**eval('dict(' + args.cerebro + ')'))

if args.plot: # Plot if requested to

cerebro.plot(**eval('dict(' + args.plot + ')'))

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description=(' - '.join([

'BTFD',

'http://dark-bid.com/BTFD-only-strategy-that-matters.html',

('https://www.reddit.com/r/algotrading/comments/5jez2b/'

'can_anyone_replicate_this_strategy/')]))

)

parser.add_argument('--offline', required=False, action='store_true',

help='Use offline file with ticker name')

parser.add_argument('--data', required=False, default='^GSPC',

metavar='TICKER', help='Yahoo ticker to download')

parser.add_argument('--fromdate', required=False, default='1990-01-01',

metavar='YYYY-MM-DD[THH:MM:SS]',

help='Starting date[time]')

parser.add_argument('--todate', required=False, default='2016-10-01',

metavar='YYYY-MM-DD[THH:MM:SS]',

help='Ending date[time]')

parser.add_argument('--cerebro', required=False, default='stdstats=False',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--broker', required=False,

default='cash=100000.0, coc=True',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--valobserver', required=False,

default='assetstart=100000.0',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--strat', required=False,

default='approach="highlow"',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--comminfo', required=False, default='leverage=2.0',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--plot', required=False, default='',

nargs='?', const='volume=False',

metavar='kwargs', help='kwargs in key=value format')

return parser.parse_args(pargs)

if __name__ == '__main__':

runstrat()