Extending Commissions

Commissions and asociated functionality were managed by a single class CommissionInfo which was mostly instantiated by calling broker.setcommission.

There were some posts to discuss the behavior.

-

Commissions: Stocks vs Futures

-

Improving Commissions: Stocks vs Futures

The concept was limited to futures with margin and a fixed commission per contract and stocks with a price/size percentage based commission. Not the most flexible of schemes even if it has served its purpose.

There was only 1 thing I didn’t like about my own implementation and that was

that CommissionInfo took the percentage value in absolute terms (0.xx)

rather than in relative terms (xx%)

A request for enhancement on GitHub #29 has led to some rework in order to:

-

Keep

CommissionInfoandbroker.setcommissioncompatible with the original behavior -

Do some clean up of the code

-

Make the Commission scheme flexible to support the enhancement request and further possibilities

The actual work before getting to the sample:

class CommInfoBase(with_metaclass(MetaParams)):

COMM_PERC, COMM_FIXED = range(2)

params = (

('commission', 0.0), ('mult', 1.0), ('margin', None),

('commtype', None),

('stocklike', False),

('percabs', False),

)

A base class for CommissionInfo has been introduced which add new parameters

to the mix:

-

commtype(default: None)This is the key to compatibility. If the value is

None, the behavior of theCommissionInfoobject andbroker.setcommissionwill work as before. Being that:-

If

marginis set then the commission scheme is for futures with a fixed commission per contract -

If

marginis not set, the commission scheme is for stocks with a percentage based approach

If the value is

COMM_PERCorCOMM_FIXED(or any other from derived classes) this obviously decides if the commission if fixed or percent based -

-

stocklike(default: False)As explained above, the actual behavior in the old

CommissionInfoobject is determined by the parametermarginAs above if

commtypeis set to something else thanNone, then this value indicates whether the asset is a futures-like asset (margin will be used and bar based cash adjustment will be performed9 or else this a stocks-like asset -

percabs(default: False)If

Falsethen the percentage must be passed in relative terms (xx%)If

Truethe percentage has to be passed as an absolute value (0.xx)CommissionInfois subclassed fromCommInfoBasechanging the default value of this parameter toTrueto keep the compatible behavior

All these parameters can also be used in broker.setcommission which now

looks like this:

def setcommission(self,

commission=0.0, margin=None, mult=1.0,

commtype=None, percabs=True, stocklike=False,

name=None):

Notice the following:

percabsisTrueto keep the behavior compatible with the old call as mentioned above for theCommissionInfoobject

The old sample to test commissions-schemes has been reworked to support

command line arguments and the new behavior. The usage help:

$ ./commission-schemes.py --help

usage: commission-schemes.py [-h] [--data DATA] [--fromdate FROMDATE]

[--todate TODATE] [--stake STAKE]

[--period PERIOD] [--cash CASH] [--comm COMM]

[--mult MULT] [--margin MARGIN]

[--commtype {none,perc,fixed}] [--stocklike]

[--percrel] [--plot] [--numfigs NUMFIGS]

Commission schemes

optional arguments:

-h, --help show this help message and exit

--data DATA, -d DATA data to add to the system (default:

../../datas/2006-day-001.txt)

--fromdate FROMDATE, -f FROMDATE

Starting date in YYYY-MM-DD format (default:

2006-01-01)

--todate TODATE, -t TODATE

Starting date in YYYY-MM-DD format (default:

2006-12-31)

--stake STAKE Stake to apply in each operation (default: 1)

--period PERIOD Period to apply to the Simple Moving Average (default:

30)

--cash CASH Starting Cash (default: 10000.0)

--comm COMM Commission factor for operation, either apercentage or

a per stake unit absolute value (default: 2.0)

--mult MULT Multiplier for operations calculation (default: 10)

--margin MARGIN Margin for futures-like operations (default: 2000.0)

--commtype {none,perc,fixed}

Commission - choose none for the old CommissionInfo

behavior (default: none)

--stocklike If the operation is for stock-like assets orfuture-

like assets (default: False)

--percrel If perc is expressed in relative xx{'const': True,

'help': u'If perc is expressed in relative xx%

ratherthan absolute value 0.xx', 'option_strings': [u'

--percrel'], 'dest': u'percrel', 'required': False,

'nargs': 0, 'choices': None, 'default': False, 'prog':

'commission-schemes.py', 'container':

<argparse._ArgumentGroup object at

0x0000000007EC9828>, 'type': None, 'metavar':

None}atherthan absolute value 0.xx (default: False)

--plot, -p Plot the read data (default: False)

--numfigs NUMFIGS, -n NUMFIGS

Plot using numfigs figures (default: 1)

Let’s do some runs to recreate the original behavior of the original commission schemes posts.

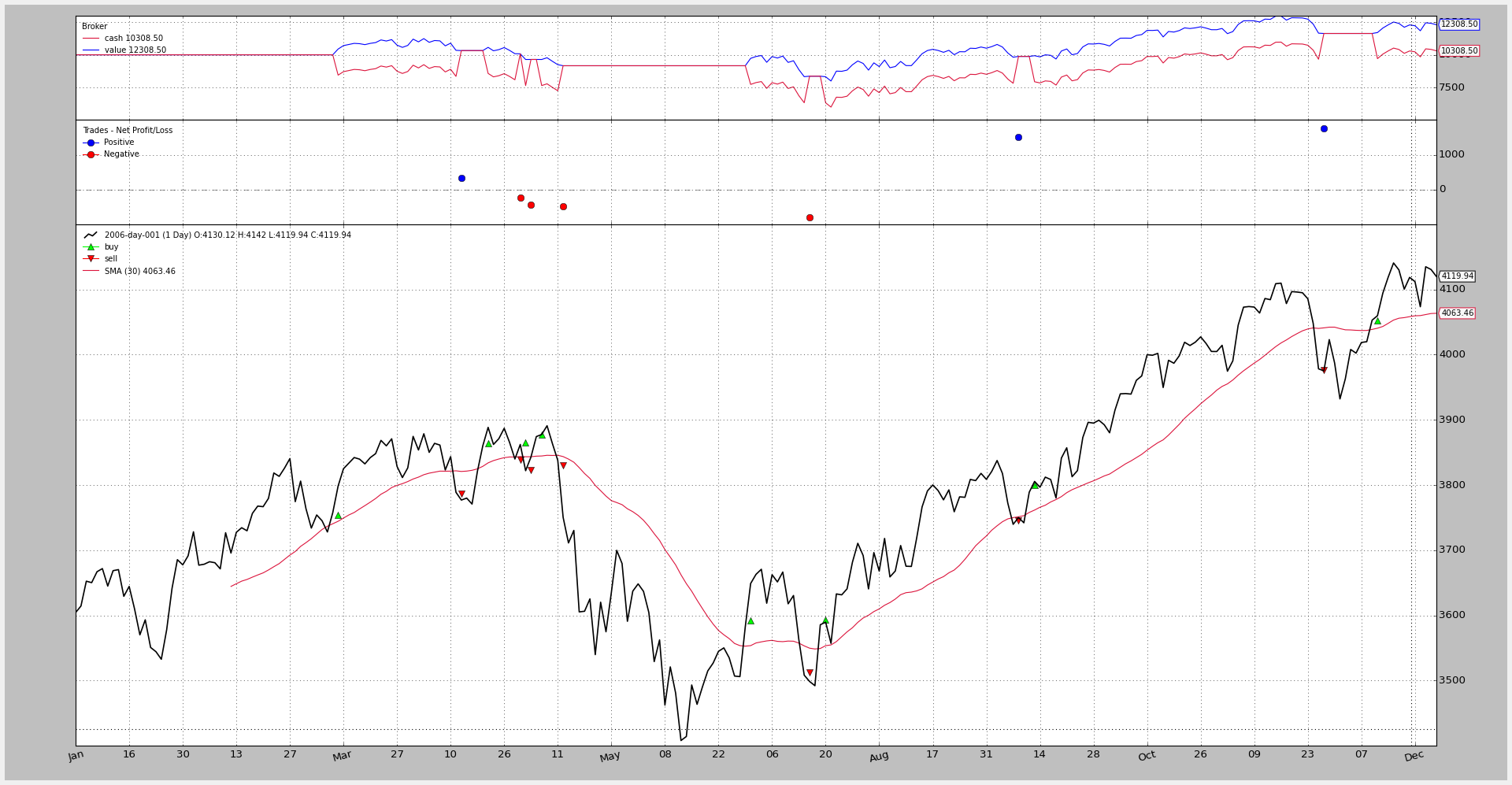

Commissions for futures (fixed and with margin)

The execution and chart:

$ ./commission-schemes.py --comm 2.0 --margin 2000.0 --mult 10 --plot

And the output showing a fixed commission of 2.0 monetary units (default stake is 1):

2006-03-09, BUY CREATE, 3757.59

2006-03-10, BUY EXECUTED, Price: 3754.13, Cost: 2000.00, Comm 2.00

2006-04-11, SELL CREATE, 3788.81

2006-04-12, SELL EXECUTED, Price: 3786.93, Cost: 2000.00, Comm 2.00

2006-04-12, TRADE PROFIT, GROSS 328.00, NET 324.00

...

Commissions for stocks (perc and withoout margin)

The execution and chart:

$ ./commission-schemes.py --comm 0.005 --margin 0 --mult 1 --plot

To improve readability a relative % value can be used:

$ ./commission-schemes.py --percrel --comm 0.5 --margin 0 --mult 1 --plot

Now 0.5 means directly 0.5%

Being the output in both cases:

2006-03-09, BUY CREATE, 3757.59

2006-03-10, BUY EXECUTED, Price: 3754.13, Cost: 3754.13, Comm 18.77

2006-04-11, SELL CREATE, 3788.81

2006-04-12, SELL EXECUTED, Price: 3786.93, Cost: 3754.13, Comm 18.93

2006-04-12, TRADE PROFIT, GROSS 32.80, NET -4.91

...

Commissions for futures (perc and with margin)

Using the new parameters, futures on a perc based scheme:

$ ./commission-schemes.py --commtype perc --percrel --comm 0.5 --margin 2000 --mult 10 --plot

It should come to no surprise that by changing the commission … the final result has changed

The output shows that the commission is variable now:

2006-03-09, BUY CREATE, 3757.59

2006-03-10, BUY EXECUTED, Price: 3754.13, Cost: 2000.00, Comm 18.77

2006-04-11, SELL CREATE, 3788.81

2006-04-12, SELL EXECUTED, Price: 3786.93, Cost: 2000.00, Comm 18.93

2006-04-12, TRADE PROFIT, GROSS 328.00, NET 290.29

...

Being in the previous run set a 2.0 monetary units (for the default stake of 1)

Another post will details the new classes and the implementation of a homme cooked commission scheme.

The code for the sample

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

class SMACrossOver(bt.Strategy):

params = (

('stake', 1),

('period', 30),

)

def log(self, txt, dt=None):

''' Logging function fot this strategy'''

dt = dt or self.datas[0].datetime.date(0)

print('%s, %s' % (dt.isoformat(), txt))

def notify_order(self, order):

if order.status in [order.Submitted, order.Accepted]:

# Buy/Sell order submitted/accepted to/by broker - Nothing to do

return

# Check if an order has been completed

# Attention: broker could reject order if not enougth cash

if order.status in [order.Completed, order.Canceled, order.Margin]:

if order.isbuy():

self.log(

'BUY EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

else: # Sell

self.log('SELL EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

def notify_trade(self, trade):

if trade.isclosed:

self.log('TRADE PROFIT, GROSS %.2f, NET %.2f' %

(trade.pnl, trade.pnlcomm))

def __init__(self):

sma = btind.SMA(self.data, period=self.p.period)

# > 0 crossing up / < 0 crossing down

self.buysell_sig = btind.CrossOver(self.data, sma)

def next(self):

if self.buysell_sig > 0:

self.log('BUY CREATE, %.2f' % self.data.close[0])

self.buy(size=self.p.stake) # keep order ref to avoid 2nd orders

elif self.position and self.buysell_sig < 0:

self.log('SELL CREATE, %.2f' % self.data.close[0])

self.sell(size=self.p.stake)

def runstrategy():

args = parse_args()

# Create a cerebro

cerebro = bt.Cerebro()

# Get the dates from the args

fromdate = datetime.datetime.strptime(args.fromdate, '%Y-%m-%d')

todate = datetime.datetime.strptime(args.todate, '%Y-%m-%d')

# Create the 1st data

data = btfeeds.BacktraderCSVData(

dataname=args.data,

fromdate=fromdate,

todate=todate)

# Add the 1st data to cerebro

cerebro.adddata(data)

# Add a strategy

cerebro.addstrategy(SMACrossOver, period=args.period, stake=args.stake)

# Add the commission - only stocks like a for each operation

cerebro.broker.setcash(args.cash)

commtypes = dict(

none=None,

perc=bt.CommInfoBase.COMM_PERC,

fixed=bt.CommInfoBase.COMM_FIXED)

# Add the commission - only stocks like a for each operation

cerebro.broker.setcommission(commission=args.comm,

mult=args.mult,

margin=args.margin,

percabs=not args.percrel,

commtype=commtypes[args.commtype],

stocklike=args.stocklike)

# And run it

cerebro.run()

# Plot if requested

if args.plot:

cerebro.plot(numfigs=args.numfigs, volume=False)

def parse_args():

parser = argparse.ArgumentParser(

description='Commission schemes',

formatter_class=argparse.ArgumentDefaultsHelpFormatter,)

parser.add_argument('--data', '-d',

default='../../datas/2006-day-001.txt',

help='data to add to the system')

parser.add_argument('--fromdate', '-f',

default='2006-01-01',

help='Starting date in YYYY-MM-DD format')

parser.add_argument('--todate', '-t',

default='2006-12-31',

help='Starting date in YYYY-MM-DD format')

parser.add_argument('--stake', default=1, type=int,

help='Stake to apply in each operation')

parser.add_argument('--period', default=30, type=int,

help='Period to apply to the Simple Moving Average')

parser.add_argument('--cash', default=10000.0, type=float,

help='Starting Cash')

parser.add_argument('--comm', default=2.0, type=float,

help=('Commission factor for operation, either a'

'percentage or a per stake unit absolute value'))

parser.add_argument('--mult', default=10, type=int,

help='Multiplier for operations calculation')

parser.add_argument('--margin', default=2000.0, type=float,

help='Margin for futures-like operations')

parser.add_argument('--commtype', required=False, default='none',

choices=['none', 'perc', 'fixed'],

help=('Commission - choose none for the old'

' CommissionInfo behavior'))

parser.add_argument('--stocklike', required=False, action='store_true',

help=('If the operation is for stock-like assets or'

'future-like assets'))

parser.add_argument('--percrel', required=False, action='store_true',

help=('If perc is expressed in relative xx% rather'

'than absolute value 0.xx'))

parser.add_argument('--plot', '-p', action='store_true',

help='Plot the read data')

parser.add_argument('--numfigs', '-n', default=1,

help='Plot using numfigs figures')

return parser.parse_args()

if __name__ == '__main__':

runstrategy()