Target Orders

Until version 1.8.10.96 smart staking was possible with backtrader over

the Strategy methods: buy and sell. It was all about adding a

Sizer to the equation which is responsible for the size of the stake.

What a Sizer cannot do is decide if the operation has to be a buy or a sell. And that means that a new concept is needed in which a small intelligence layer is added to make such decision.

Here is where the family of order_target_xxx methods in the Strategy come

into play. Inspired by the ones in zipline, the methods offer the chance to

simply specify the final target, be the target:

-

size-> amount of shares, contracts in the portfolio of a specific asset -

value-> value in monetary units of the asset in the portfolio -

percent-> percentage (from current portfolio) value of the asset in the current portfolio

Note

The reference for the methods can be found in Strategy. The

summary is that the methods use the same signature as buy and

sell except for the parameter size which is replaced by the

parameter target

In this case it is all about specifying the final target and the method

decides if an operation will be a buy or a sell. The same logic applies to

the 3 methods. Let’s tart with order_target_size

-

If the target is greater than the position a buy is issued, with the difference

target - position_sizeExamples:

-

Pos:

0, target:7-> buy(size=7 - 0) -> buy(size=7) -

Pos:

3, target:7-> buy(size=7 - 3) -> buy(size=4) -

Pos:

-3, target:7-> buy(size=7 - -3) -> buy(size=10) -

Pos:

-3, target:-2-> buy(size=-2 - -3) -> buy(size=1)

-

-

If the target is smaller than the position a sell is issued with the difference

position_size - targetExamples:

-

Pos:

0, target:-7-> sell(size=0 - -7) -> sell(size=7) -

Pos:

3, target:-7-> sell(size=3 - -7) -> sell(size=10) -

Pos:

-3, target:-7-> sell(size=-3 - -7) -> sell(size=4) -

Pos:

3, target:2-> sell(size=3 - 2) -> sell(size=1)

-

When targetting a value with order_target_value, the current value of the

asset in the portfolio and the position size are both taken into account to

decide what the final underlying operation will be. The reasoning:

- If position size is negative (short) and the target value has to be greater than the current value, this means: sell more

As such the logic works as follows:

-

If

target > valueandsize >=0-> buy -

If

target > valueandsize < 0-> sell -

If

target < valueandsize >= 0-> sell -

If

target < valueandsize < 0-> buy

The logic for order_target_percent is the same as that of

order_target_value. This method simply takes into account the current total

value of the portfolio to determine the target value for the asset.

The Sample

backtrader tries to have a sample for each new functionality and this is no

exception. No bells and whistles, just something to test the results are as

expected. This one is under the order_target directory in the samples.

The logic in the sample is rather dumb and only meaant for testing:

-

During odd months (Jan, Mar, …), use the day as target (in the case of

order_target_valuemultiplying the day by1000)This mimics an increasing target

-

During even months (Feb, Apr, …) use

31 - dayas the targetThis mimics an decreasing target

order_target_size

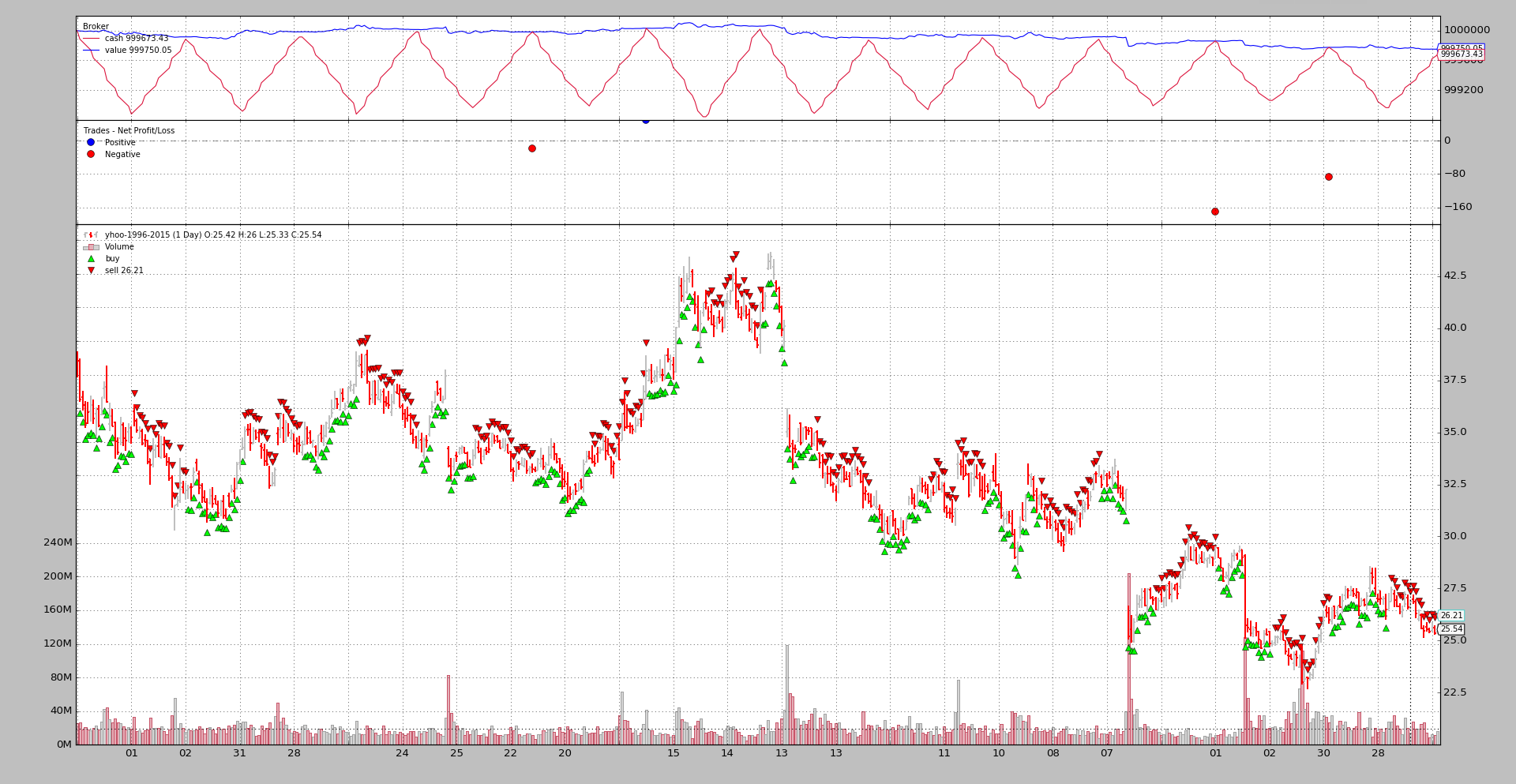

Let’s see what happens in Jan and Feb.

$ ./order_target.py --target-size -- plot

0001 - 2005-01-03 - Position Size: 00 - Value 1000000.00

0001 - 2005-01-03 - Order Target Size: 03

0002 - 2005-01-04 - Position Size: 03 - Value 999994.39

0002 - 2005-01-04 - Order Target Size: 04

0003 - 2005-01-05 - Position Size: 04 - Value 999992.48

0003 - 2005-01-05 - Order Target Size: 05

0004 - 2005-01-06 - Position Size: 05 - Value 999988.79

...

0020 - 2005-01-31 - Position Size: 28 - Value 999968.70

0020 - 2005-01-31 - Order Target Size: 31

0021 - 2005-02-01 - Position Size: 31 - Value 999954.68

0021 - 2005-02-01 - Order Target Size: 30

0022 - 2005-02-02 - Position Size: 30 - Value 999979.65

0022 - 2005-02-02 - Order Target Size: 29

0023 - 2005-02-03 - Position Size: 29 - Value 999966.33

0023 - 2005-02-03 - Order Target Size: 28

...

In Jan the target starts at 3 with the 1st trading day of the year and

increases. And the position size moves initially from 0 to 3 and then

in increments of 1.

Finishing Jan the last order_target is for 31 and that position size

is reported when entering the 1st day of Feb, when the new target side is

requested to be 30 and goes changing along with the position in decrements

of ´1`.

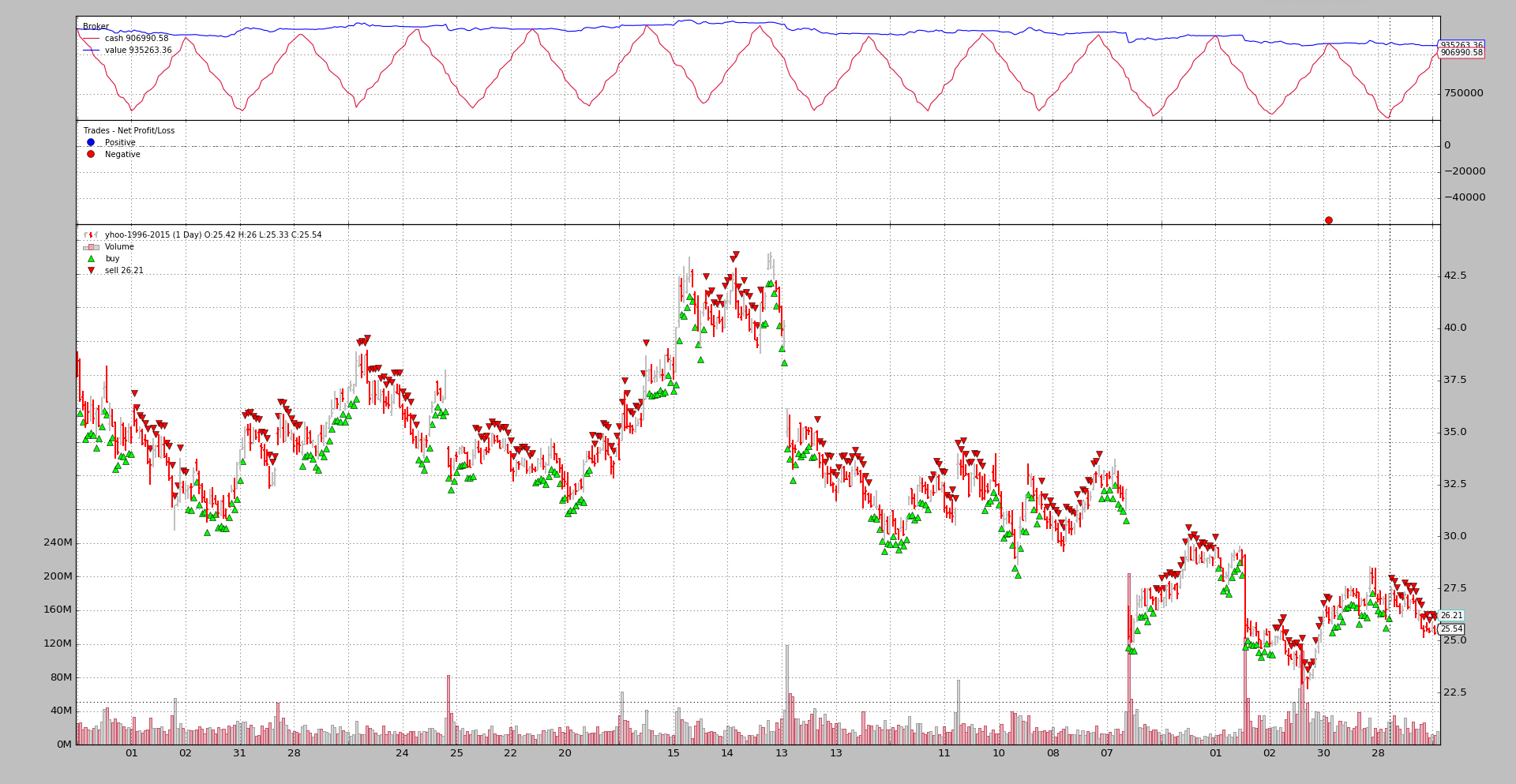

order_target_value

A similar behavior is expected from target values

$ ./order_target.py --target-value --plot

0001 - 2005-01-03 - Position Size: 00 - Value 1000000.00

0001 - 2005-01-03 - data value 0.00

0001 - 2005-01-03 - Order Target Value: 3000.00

0002 - 2005-01-04 - Position Size: 78 - Value 999854.14

0002 - 2005-01-04 - data value 2853.24

0002 - 2005-01-04 - Order Target Value: 4000.00

0003 - 2005-01-05 - Position Size: 109 - Value 999801.68

0003 - 2005-01-05 - data value 3938.17

0003 - 2005-01-05 - Order Target Value: 5000.00

0004 - 2005-01-06 - Position Size: 138 - Value 999699.57

...

0020 - 2005-01-31 - Position Size: 808 - Value 999206.37

0020 - 2005-01-31 - data value 28449.68

0020 - 2005-01-31 - Order Target Value: 31000.00

0021 - 2005-02-01 - Position Size: 880 - Value 998807.33

0021 - 2005-02-01 - data value 30580.00

0021 - 2005-02-01 - Order Target Value: 30000.00

0022 - 2005-02-02 - Position Size: 864 - Value 999510.21

0022 - 2005-02-02 - data value 30706.56

0022 - 2005-02-02 - Order Target Value: 29000.00

0023 - 2005-02-03 - Position Size: 816 - Value 999130.05

0023 - 2005-02-03 - data value 28633.44

0023 - 2005-02-03 - Order Target Value: 28000.00

...

There is an extra line of information telling what the actual data value (in the portfolio) is. This helps in finding out if the target value has been reachec.

The initial target is 3000.0 and the reported initial value is

2853.24. The question here is whether this is close enough. And the

answer is Yes

-

The sample uses a

Marketorder at the end of a daily bar and the last available price to calculate a target size which meets the target value -

The execution uses then the

openprice of the next day and this is unlikely to be the previousclose

Doing it in any other way would mean one is cheating him/herfself.

The next target value and final value are much closer: 4000 and

3938.17.

When changing into Feb the target value starts decreasing from 31000 to

30000 and 29000. So does the data value with from 30580.00 to

30706.56 and then to 28633.44. Wait:

-

30580->30706.56is a positive changeIndeed. In this case the calculated size for the target value met an opening price which bumped the value to

30706.56

How this effect can be avoided:

-

The sample uses a

Markettype execution for the orders and this effect cannot be avoided -

The methods

order_target_xxxallow specifying the execution type and price.One could specify

Limitas the execution order and let the price be the close price (chosen by the method if nothing else be provided) or even provide specific pricing

order_target_percent

In this case it is simply a percentage of the current portfolio value.

$ ./order_target.py --target-percent --plot

0001 - 2005-01-03 - Position Size: 00 - Value 1000000.00

0001 - 2005-01-03 - data percent 0.00

0001 - 2005-01-03 - Order Target Percent: 0.03

0002 - 2005-01-04 - Position Size: 785 - Value 998532.05

0002 - 2005-01-04 - data percent 0.03

0002 - 2005-01-04 - Order Target Percent: 0.04

0003 - 2005-01-05 - Position Size: 1091 - Value 998007.44

0003 - 2005-01-05 - data percent 0.04

0003 - 2005-01-05 - Order Target Percent: 0.05

0004 - 2005-01-06 - Position Size: 1381 - Value 996985.64

...

0020 - 2005-01-31 - Position Size: 7985 - Value 991966.28

0020 - 2005-01-31 - data percent 0.28

0020 - 2005-01-31 - Order Target Percent: 0.31

0021 - 2005-02-01 - Position Size: 8733 - Value 988008.94

0021 - 2005-02-01 - data percent 0.31

0021 - 2005-02-01 - Order Target Percent: 0.30

0022 - 2005-02-02 - Position Size: 8530 - Value 995005.45

0022 - 2005-02-02 - data percent 0.30

0022 - 2005-02-02 - Order Target Percent: 0.29

0023 - 2005-02-03 - Position Size: 8120 - Value 991240.75

0023 - 2005-02-03 - data percent 0.29

0023 - 2005-02-03 - Order Target Percent: 0.28

...

And the information has been changed to see the % the data represents in

the portfolio.

Sample Usage

$ ./order_target.py --help

usage: order_target.py [-h] [--data DATA] [--fromdate FROMDATE]

[--todate TODATE] [--cash CASH]

(--target-size | --target-value | --target-percent)

[--plot [kwargs]]

Sample for Order Target

optional arguments:

-h, --help show this help message and exit

--data DATA Specific data to be read in (default:

../../datas/yhoo-1996-2015.txt)

--fromdate FROMDATE Starting date in YYYY-MM-DD format (default:

2005-01-01)

--todate TODATE Ending date in YYYY-MM-DD format (default: 2006-12-31)

--cash CASH Ending date in YYYY-MM-DD format (default: 1000000)

--target-size Use order_target_size (default: False)

--target-value Use order_target_value (default: False)

--target-percent Use order_target_percent (default: False)

--plot [kwargs], -p [kwargs]

Plot the read data applying any kwargs passed For

example: --plot style="candle" (to plot candles)

(default: None)

Sample Code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

from datetime import datetime

import backtrader as bt

class TheStrategy(bt.Strategy):

'''

This strategy is loosely based on some of the examples from the Van

K. Tharp book: *Trade Your Way To Financial Freedom*. The logic:

- Enter the market if:

- The MACD.macd line crosses the MACD.signal line to the upside

- The Simple Moving Average has a negative direction in the last x

periods (actual value below value x periods ago)

- Set a stop price x times the ATR value away from the close

- If in the market:

- Check if the current close has gone below the stop price. If yes,

exit.

- If not, update the stop price if the new stop price would be higher

than the current

'''

params = (

('use_target_size', False),

('use_target_value', False),

('use_target_percent', False),

)

def notify_order(self, order):

if order.status == order.Completed:

pass

if not order.alive():

self.order = None # indicate no order is pending

def start(self):

self.order = None # sentinel to avoid operrations on pending order

def next(self):

dt = self.data.datetime.date()

portfolio_value = self.broker.get_value()

print('%04d - %s - Position Size: %02d - Value %.2f' %

(len(self), dt.isoformat(), self.position.size, portfolio_value))

data_value = self.broker.get_value([self.data])

if self.p.use_target_value:

print('%04d - %s - data value %.2f' %

(len(self), dt.isoformat(), data_value))

elif self.p.use_target_percent:

port_perc = data_value / portfolio_value

print('%04d - %s - data percent %.2f' %

(len(self), dt.isoformat(), port_perc))

if self.order:

return # pending order execution

size = dt.day

if (dt.month % 2) == 0:

size = 31 - size

if self.p.use_target_size:

target = size

print('%04d - %s - Order Target Size: %02d' %

(len(self), dt.isoformat(), size))

self.order = self.order_target_size(target=size)

elif self.p.use_target_value:

value = size * 1000

print('%04d - %s - Order Target Value: %.2f' %

(len(self), dt.isoformat(), value))

self.order = self.order_target_value(target=value)

elif self.p.use_target_percent:

percent = size / 100.0

print('%04d - %s - Order Target Percent: %.2f' %

(len(self), dt.isoformat(), percent))

self.order = self.order_target_percent(target=percent)

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

cerebro.broker.setcash(args.cash)

dkwargs = dict()

if args.fromdate is not None:

dkwargs['fromdate'] = datetime.strptime(args.fromdate, '%Y-%m-%d')

if args.todate is not None:

dkwargs['todate'] = datetime.strptime(args.todate, '%Y-%m-%d')

# data

data = bt.feeds.YahooFinanceCSVData(dataname=args.data, **dkwargs)

cerebro.adddata(data)

# strategy

cerebro.addstrategy(TheStrategy,

use_target_size=args.target_size,

use_target_value=args.target_value,

use_target_percent=args.target_percent)

cerebro.run()

if args.plot:

pkwargs = dict(style='bar')

if args.plot is not True: # evals to True but is not True

npkwargs = eval('dict(' + args.plot + ')') # args were passed

pkwargs.update(npkwargs)

cerebro.plot(**pkwargs)

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description='Sample for Order Target')

parser.add_argument('--data', required=False,

default='../../datas/yhoo-1996-2015.txt',

help='Specific data to be read in')

parser.add_argument('--fromdate', required=False,

default='2005-01-01',

help='Starting date in YYYY-MM-DD format')

parser.add_argument('--todate', required=False,

default='2006-12-31',

help='Ending date in YYYY-MM-DD format')

parser.add_argument('--cash', required=False, action='store',

type=float, default=1000000,

help='Ending date in YYYY-MM-DD format')

pgroup = parser.add_mutually_exclusive_group(required=True)

pgroup.add_argument('--target-size', required=False, action='store_true',

help=('Use order_target_size'))

pgroup.add_argument('--target-value', required=False, action='store_true',

help=('Use order_target_value'))

pgroup.add_argument('--target-percent', required=False,

action='store_true',

help=('Use order_target_percent'))

# Plot options

parser.add_argument('--plot', '-p', nargs='?', required=False,

metavar='kwargs', const=True,

help=('Plot the read data applying any kwargs passed\n'

'\n'

'For example:\n'

'\n'

' --plot style="candle" (to plot candles)\n'))

if pargs is not None:

return parser.parse_args(pargs)

return parser.parse_args()

if __name__ == '__main__':

runstrat()