Ultimate Oscillator

One of the goals when the development of backtrader was kickstarted was to make it very easy (at least for the author himself) to develop new Indicators to test ideas both mathematically and visually.

Ticket #102 is about adding the UltimateOscillator to the arsenal of backtrader

Note

It will be added in the next release, meanwhile it can be used, using the code below.

The reference as indicated in the ticket:

and also at:

No need to repeat it here.

Quoting from the reference:

BP = Close - Minimum(Low or Prior Close)

TR = Maximum(High or Prior Close) - Minimum(Low or Prior Close)

Average7 = (7-period BP Sum) / (7-period TR Sum)

Average14 = (14-period BP Sum) / (14-period TR Sum)

Average28 = (28-period BP Sum) / (28-period TR Sum)

UO = 100 x [(4 x Average7)+(2 x Average14)+Average28]/(4+2+1)

Summary:

-

First subclass from

bt.Indicatorto make sure the entire machinery works:class UltimateOscillator(bt.Indicator): -

It has 1 output line: we’ll name it

uo:lines = ('uo',) -

It has 3 parameters which define 3 periods with default values

7,14and28. To be namedp1,p2andp3:params = (('p1', 7), ('p2', 14), ('p3', 28), ) -

The calculations use some things already built-in backtrader

Minimum(Low or Prior Close): this isTrueLowas defined by Welles Wilder for theRSIindicator. As such theBPor Buying Pressure can be calculated:

bp = self.data.close - TrueLow(self.data)Maximum(Low or Prior Close) - Minimum(Low or Prior Close): this isTrueRangeas defined by Welles Wilder for theRSIindicator (which can be expressed asTrueHigh - TrueLow. The next calculation is therefore as easy as:

tr = TrueRange(self.data)- The rest are pure math operations, using

SumNto add up the latestp1,p2,p3periods ofbpandtr, plus the weighted calculation:

av7 = SumN(bp, period=self.p.p1) / SumN(tr, period=self.p.p1) av14 = SumN(bp, period=self.p.p2) / SumN(tr, period=self.p.p2) av28 = SumN(bp, period=self.p.p3) / SumN(tr, period=self.p.p3) uo = 100.0 * (4.0 * av7 + 2.0 * av14 + av28) / (4.0 + 2.0 + 1.0)- Finally the assignment of the calculation to the defined

uoline:

self.lines.uo = uo

It seems longer than it actually is (the full code, including imports) at the bottom.

Since we want not only the values but also a nice looking plot, like the ones provided by Stockcharts, we’ll be adding 2 extra touches:

-

2 parameters which determine where to place the horizontal lines that delimit the overbought and oversold areas (ala

RSIorStochastic):('upperband', 70.0), ('lowerband', 30.0), -

And plot initialization code to use the parameters. Ticks at

10,50and90like in the Stockcharts plots will be added:def _plotinit(self): baseticks = [10.0, 50.0, 90.0] hlines = [self.p.upperband, self.p.lowerband] self.plotinfo.plotyhlines = hlines self.plotinfo.plotyticks = baseticks + hlines

To test and to further use existing facilities provided by backtrader, the

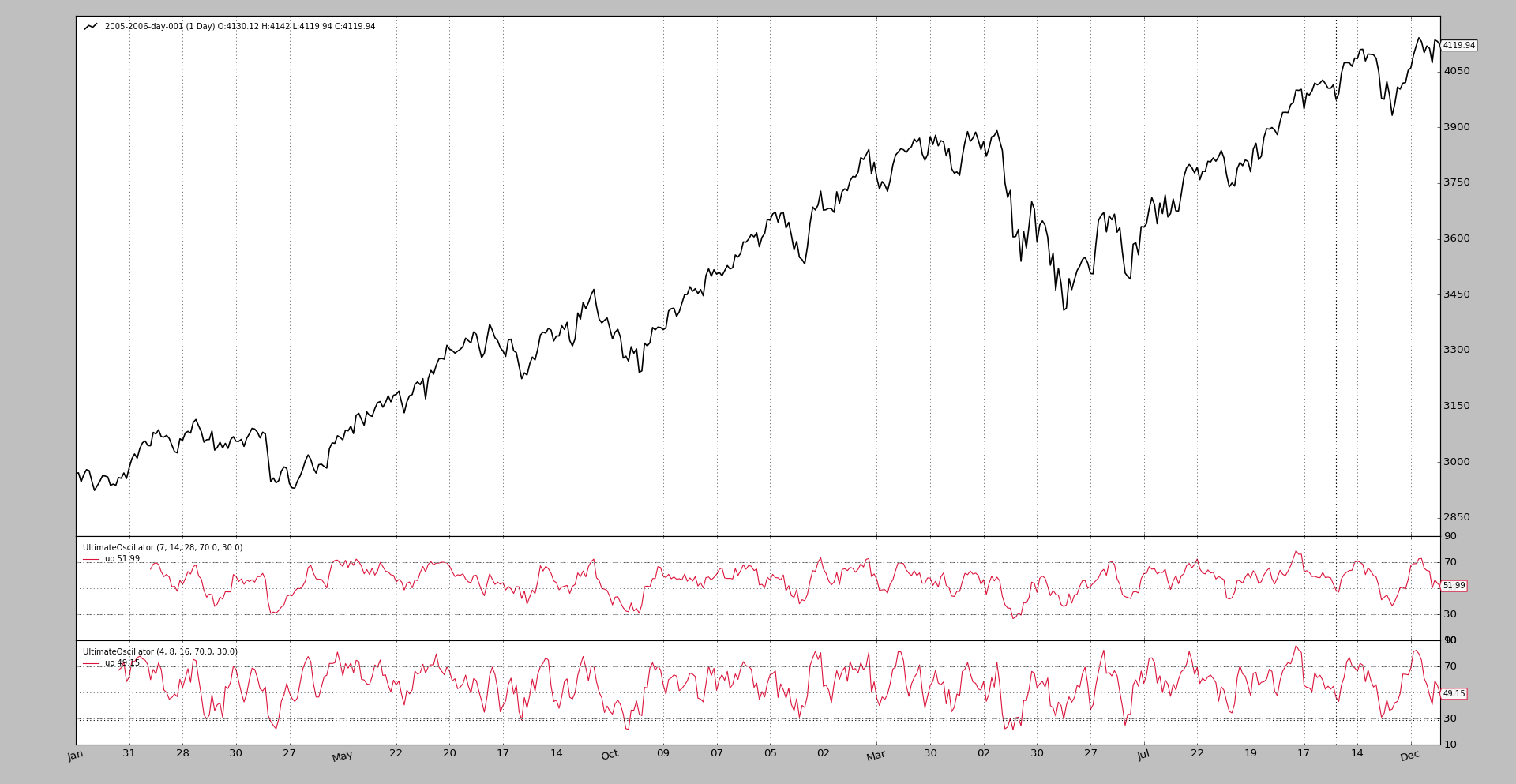

btrun executable installed along with backtrader will be used.

-

The indicator is stored in a file named

ultimateoscillator.py -

The data used is one of the data samples available in the sources of backtrader

-

The indicator will be added twice with the default parameters and with shorter term parameters

Execution:

btrun \

--nostdstats \

--data 2005-2006-day-001.txt \

--indicator ultimateoscillator:UltimateOscillator \

--indicator ultimateoscillator:UltimateOscillator:p1=4,p2=8,p3=16 \

--plot

Note

Using –nostdstats to remove some observers from the chart. No need to track cash and value in this case

The output is simply a chart showing the evolution of the

UltimateOscillator.

The UltimateOscillator code:

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import backtrader as bt

from backtrader.indicators import SumN, TrueLow, TrueRange

class UltimateOscillator(bt.Indicator):

'''

Formula:

# Buying Pressure = Close - TrueLow

BP = Close - Minimum(Low or Prior Close)

# TrueRange = TrueHigh - TrueLow

TR = Maximum(High or Prior Close) - Minimum(Low or Prior Close)

Average7 = (7-period BP Sum) / (7-period TR Sum)

Average14 = (14-period BP Sum) / (14-period TR Sum)

Average28 = (28-period BP Sum) / (28-period TR Sum)

UO = 100 x [(4 x Average7)+(2 x Average14)+Average28]/(4+2+1)

See:

- https://en.wikipedia.org/wiki/Ultimate_oscillator

- http://stockcharts.com/school/doku.php?id=chart_school:technical_indicators:ultimate_oscillator

'''

lines = ('uo',)

params = (('p1', 7),

('p2', 14),

('p3', 28),

('upperband', 70.0),

('lowerband', 30.0),

)

def _plotinit(self):

baseticks = [10.0, 50.0, 90.0]

hlines = [self.p.upperband, self.p.lowerband]

self.plotinfo.plotyhlines = hlines

self.plotinfo.plotyticks = baseticks + hlines

def __init__(self):

bp = self.data.close - TrueLow(self.data)

tr = TrueRange(self.data)

av7 = SumN(bp, period=self.p.p1) / SumN(tr, period=self.p.p1)

av14 = SumN(bp, period=self.p.p2) / SumN(tr, period=self.p.p2)

av28 = SumN(bp, period=self.p.p3) / SumN(tr, period=self.p.p3)

uo = 100.0 * (4.0 * av7 + 2.0 * av14 + av28) / (4.0 + 2.0 + 1.0)

self.lines.uo = uo