Observers and Statistics

Strategies running inside the backtrader do mostly deal with data feeds

and indicators.

Data feeds are added to Cerebro instances and end up being part of the input of strategies (parsed and served as attributes of the instance) whereas Indicators are declared and managed by the Strategy itself.

All backtrader sample charts have so far had 3 things plotted which seem to

be taken for granted because they are not declared anywhere:

-

Cash and Value (what’s happening with the money in the broker)

-

Trades (aka Operations)

-

Buy/Sell Orders

They are Observers and exist within the submodule

backtrader.observers. They are there because Cerebro supports a

parameter to automatically add (or not) them to the Strategy:

stdstats(default:True)

If the default is respected Cerebro executes the following equivalent user code:

import backtrader as bt

...

cerebro = bt.Cerebro() # default kwarg: stdstats=True

cerebro.addobserver(bt.observers.Broker)

cerebro.addobserver(bt.observers.Trades)

cerebro.addobserver(bt.observers.BuySell)

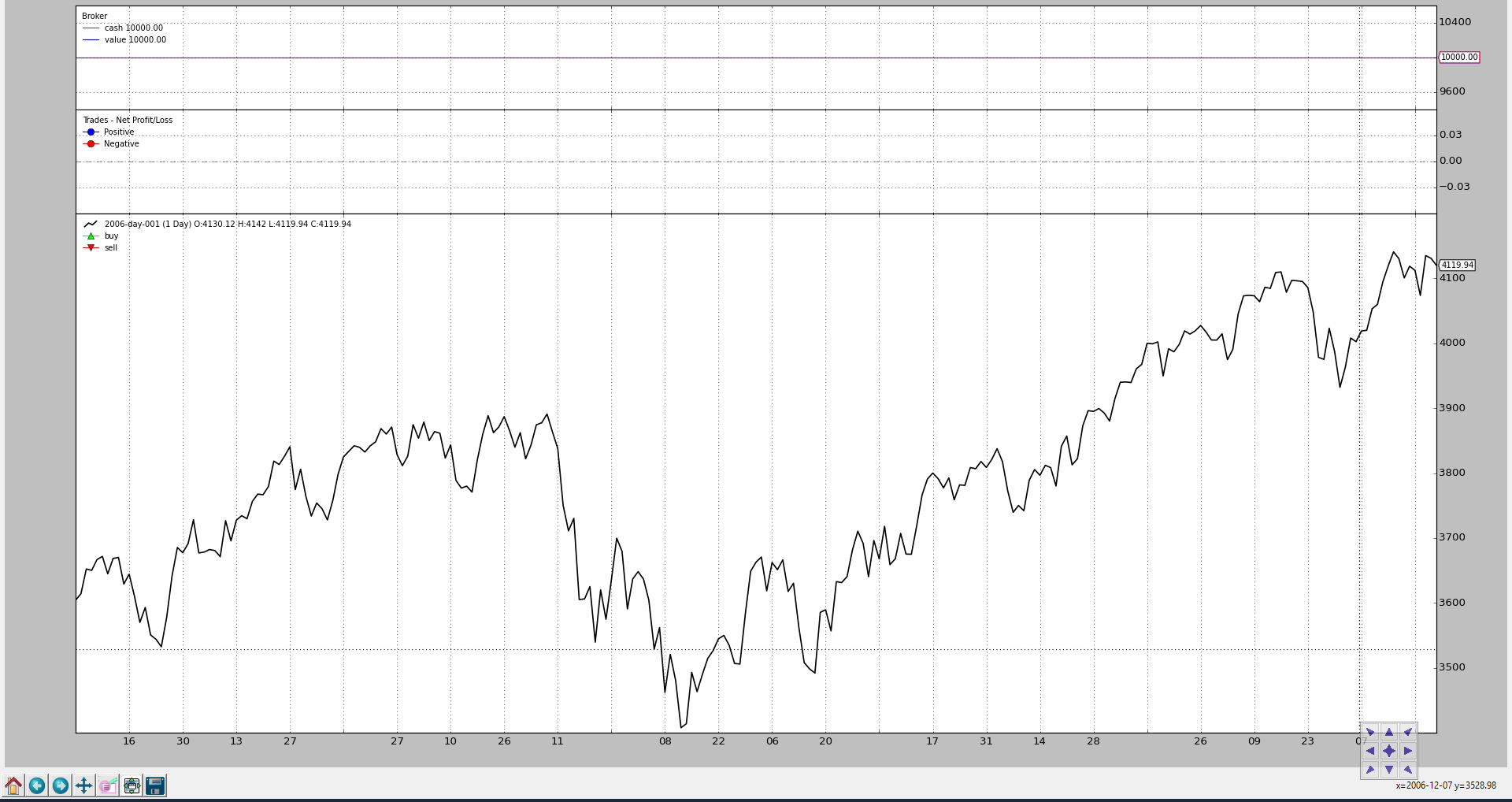

Let’s see the usual chart with those 3 default observers (even if no order is issued and therefore no trade happens and there is no change to the cash and portfolio value)

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import backtrader as bt

import backtrader.feeds as btfeeds

if __name__ == '__main__':

cerebro = bt.Cerebro(stdstats=False)

cerebro.addstrategy(bt.Strategy)

data = bt.feeds.BacktraderCSVData(dataname='../../datas/2006-day-001.txt')

cerebro.adddata(data)

cerebro.run()

cerebro.plot()

Now let’s change the value of stdstats to False when creating the

Cerebro instance (can also be done when invoking run):

cerebro = bt.Cerebro(stdstats=False)

The chart is different now.

Accesing the Observers

The Observers as seen above are already there in the default case and collecting information which can be used for statistical purposes and that’s why acess to the observers can be done through an attribute of the strategy called:

stats

It is simply a placeholder. If we recall the addition of one of the default Observers as laid out above:

...

cerebro.addobserver(backtrader.observers.Broker)

...

The obvious question would be how to access the Broker observer. Here for

example how it’s done from the next method of a strategy:

class MyStrategy(bt.Strategy):

def next(self):

if self.stats.broker.value[0] < 1000.0:

print('WHITE FLAG ... I LOST TOO MUCH')

elif self.stats.broker.value[0] > 10000000.0:

print('TIME FOR THE VIRGIN ISLANDS ....!!!')

The Broker observer just like a Data, an Indicator and the Strategy itself

is also a Lines objects. In this case the Broker has 2 lines:

-

cash -

value

Observer Implementation

The implementation is very similar to that of an Indicator:

class Broker(Observer):

alias = ('CashValue',)

lines = ('cash', 'value')

plotinfo = dict(plot=True, subplot=True)

def next(self):

self.lines.cash[0] = self._owner.broker.getcash()

self.lines.value[0] = value = self._owner.broker.getvalue()

Steps:

-

Derive from

Observer(and not fromIndicator) -

Declare lines and params as needed (

Brokerhas 2 lines but no params) -

There will be an automatic attribute

_ownerwhich is the strategy holding the observer

Observers come in action:

-

After all Indicators have been calculated

-

After the Strategy

nextmethod has been executed -

That means: at the end of the cycle … they observe what has happened

In the Broker case it’s simply blindly recording the broker cash and

portfolio values at each point in time.

Adding Observers to the Strategy

As already pointed out above, Cerebro is using the stdstats parameter to

decide whether to add 3 default Observers, alleviating the work of the end

user.

Adding other Observers to the mix is possible, be it along the stdstats or

removing those.

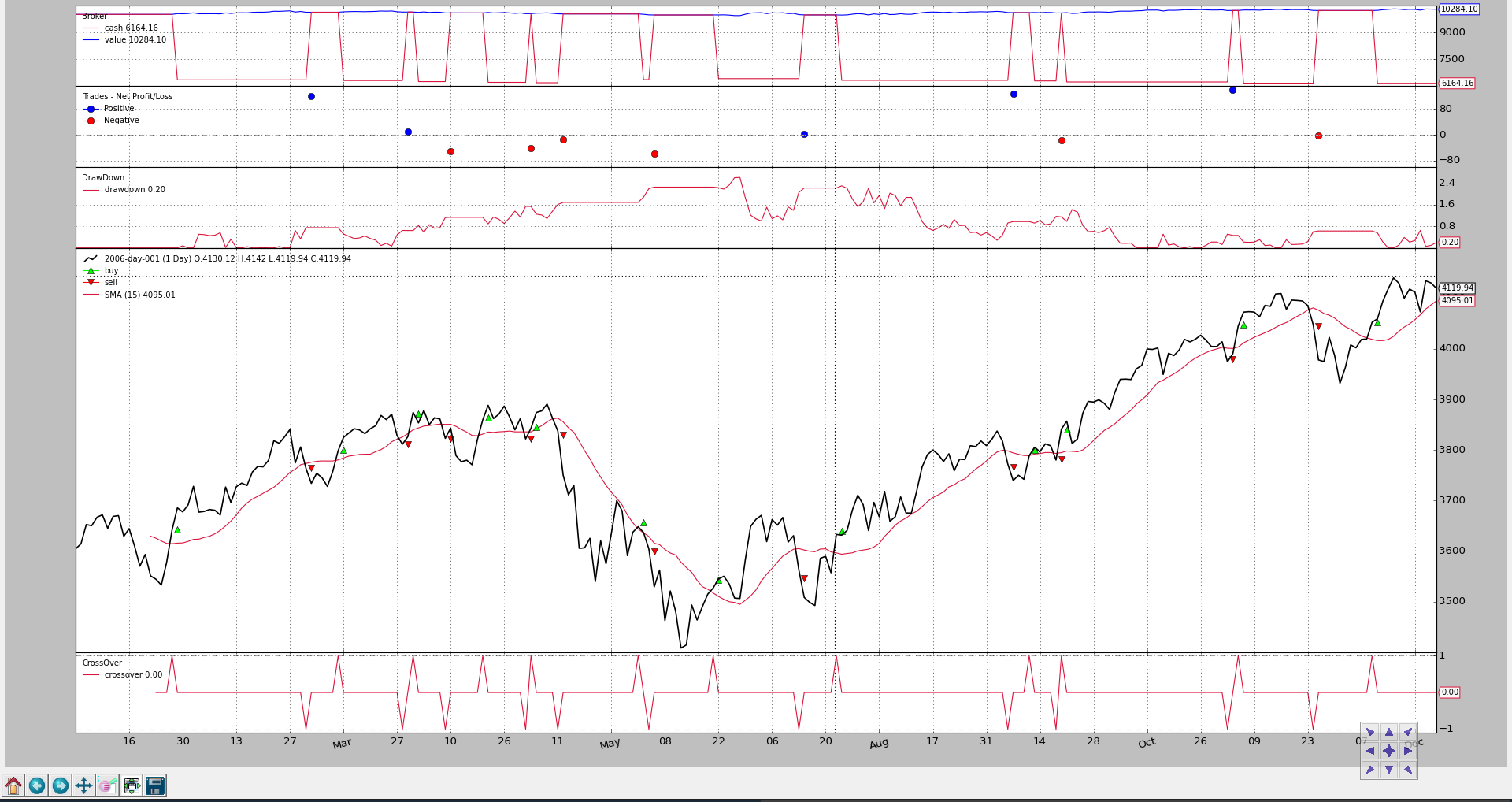

Let’s go for the usual strategy which buys when the close price goes above a

SimpleMovingAverage and sells if the opposite is true.

With one “addition”:

- DrawDown which is an already existing observer in the

backtraderecosystem

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import os.path

import time

import sys

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

class MyStrategy(bt.Strategy):

params = (('smaperiod', 15),)

def log(self, txt, dt=None):

''' Logging function fot this strategy'''

dt = dt or self.data.datetime[0]

if isinstance(dt, float):

dt = bt.num2date(dt)

print('%s, %s' % (dt.isoformat(), txt))

def __init__(self):

# SimpleMovingAverage on main data

# Equivalent to -> sma = btind.SMA(self.data, period=self.p.smaperiod)

sma = btind.SMA(period=self.p.smaperiod)

# CrossOver (1: up, -1: down) close / sma

self.buysell = btind.CrossOver(self.data.close, sma, plot=True)

# Sentinel to None: new ordersa allowed

self.order = None

def next(self):

# Access -1, because drawdown[0] will be calculated after "next"

self.log('DrawDown: %.2f' % self.stats.drawdown.drawdown[-1])

self.log('MaxDrawDown: %.2f' % self.stats.drawdown.maxdrawdown[-1])

# Check if we are in the market

if self.position:

if self.buysell < 0:

self.log('SELL CREATE, %.2f' % self.data.close[0])

self.sell()

elif self.buysell > 0:

self.log('BUY CREATE, %.2f' % self.data.close[0])

self.buy()

def runstrat():

cerebro = bt.Cerebro()

data = bt.feeds.BacktraderCSVData(dataname='../../datas/2006-day-001.txt')

cerebro.adddata(data)

cerebro.addobserver(bt.observers.DrawDown)

cerebro.addstrategy(MyStrategy)

cerebro.run()

cerebro.plot()

if __name__ == '__main__':

runstrat()

The visual output shows the evolution of the drawdown

And part of the text output:

...

2006-12-14T23:59:59+00:00, MaxDrawDown: 2.62

2006-12-15T23:59:59+00:00, DrawDown: 0.22

2006-12-15T23:59:59+00:00, MaxDrawDown: 2.62

2006-12-18T23:59:59+00:00, DrawDown: 0.00

2006-12-18T23:59:59+00:00, MaxDrawDown: 2.62

2006-12-19T23:59:59+00:00, DrawDown: 0.00

2006-12-19T23:59:59+00:00, MaxDrawDown: 2.62

2006-12-20T23:59:59+00:00, DrawDown: 0.10

2006-12-20T23:59:59+00:00, MaxDrawDown: 2.62

2006-12-21T23:59:59+00:00, DrawDown: 0.39

2006-12-21T23:59:59+00:00, MaxDrawDown: 2.62

2006-12-22T23:59:59+00:00, DrawDown: 0.21

2006-12-22T23:59:59+00:00, MaxDrawDown: 2.62

2006-12-27T23:59:59+00:00, DrawDown: 0.28

2006-12-27T23:59:59+00:00, MaxDrawDown: 2.62

2006-12-28T23:59:59+00:00, DrawDown: 0.65

2006-12-28T23:59:59+00:00, MaxDrawDown: 2.62

2006-12-29T23:59:59+00:00, DrawDown: 0.06

2006-12-29T23:59:59+00:00, MaxDrawDown: 2.62

Note

As seen in the text output and in the code, the DrawDown observer has

actually 2 lines:

-

drawdown -

maxdrawdown

The choice is not to plot the maxdrawdown line, but make it is still

available to the user.

Actually the last value of maxdrawdown is also available in a direct

attribute (not a line) with the name of maxdd

Developing Observers

The implementation of the Broker observer was shown above. To produce a

meaningful observer, the implementation can use the following information:

-

self._owneris the currently strategy being executedAs such anything within the strategy is available to the observer

-

Default internal things available in the strategy which may be useful:

broker-> attribute giving access to the broker instance the strategy creates order against

As seen in

Broker, cash and portfolio values are collected by invoking the methodsgetcashandgetvalue_orderspending-> list orders created by the strategy and for which the broker has notified an event to the strategy.

The

BuySellobserver traverses the list looking for orders which have executed (totally or partially) to create an average execution price for the given point in time (index 0)_tradespending-> list of trades (a set of completed buy/sell or sell/buy pairs) which is compiled from the buy/sell orders

An Observer can obviously access other observers over the

self._owner.stats path.

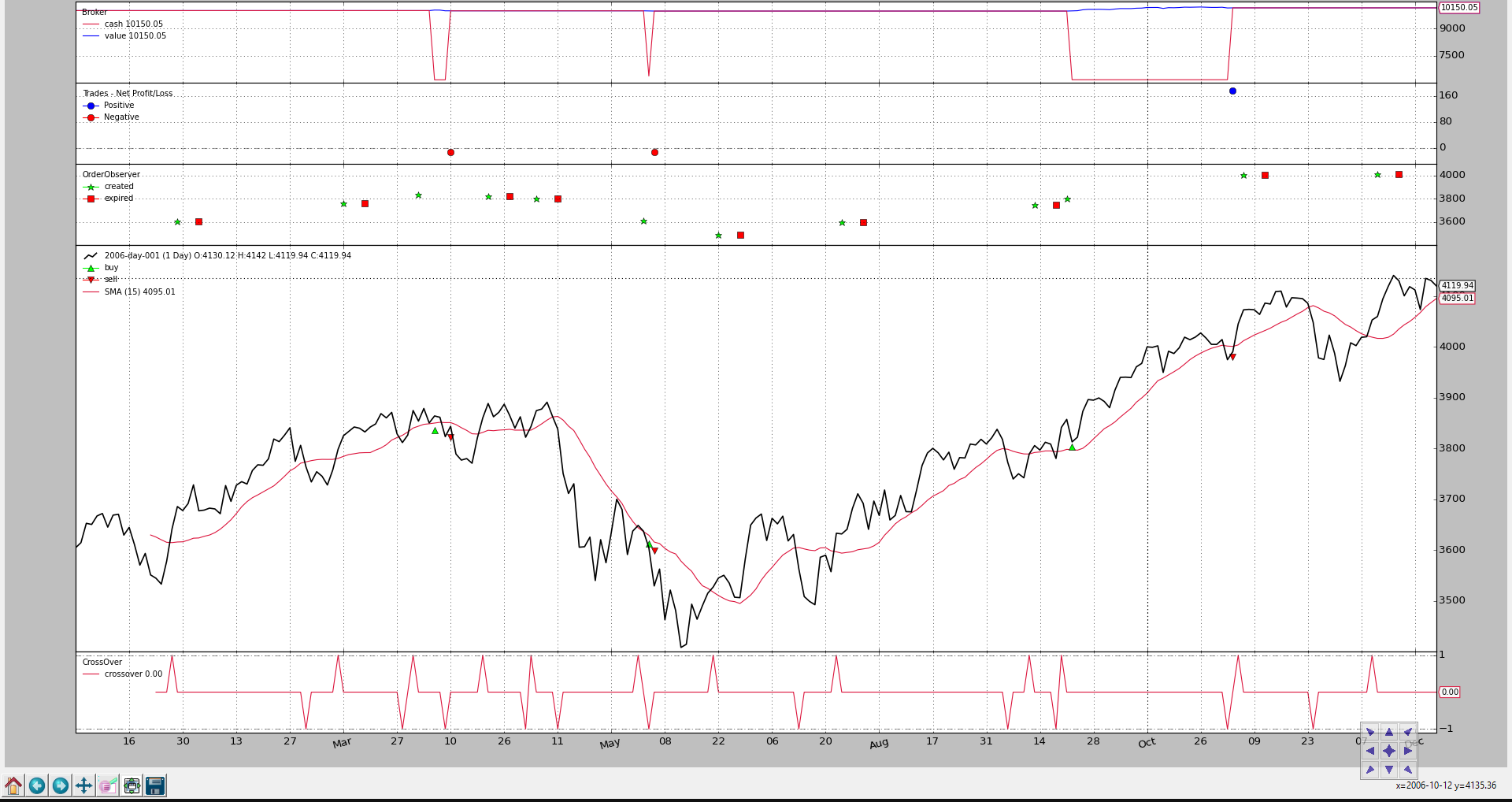

Custom OrderObserver

The standard BuySell observer does only care about operations which have

executed. We can create an observer which shows when orders where created and if

they expired.

For the sake of visibility the display will not be plotted along the price but on a separate axis.

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import math

import backtrader as bt

class OrderObserver(bt.observer.Observer):

lines = ('created', 'expired',)

plotinfo = dict(plot=True, subplot=True, plotlinelabels=True)

plotlines = dict(

created=dict(marker='*', markersize=8.0, color='lime', fillstyle='full'),

expired=dict(marker='s', markersize=8.0, color='red', fillstyle='full')

)

def next(self):

for order in self._owner._orderspending:

if order.data is not self.data:

continue

if not order.isbuy():

continue

# Only interested in "buy" orders, because the sell orders

# in the strategy are Market orders and will be immediately

# executed

if order.status in [bt.Order.Accepted, bt.Order.Submitted]:

self.lines.created[0] = order.created.price

elif order.status in [bt.Order.Expired]:

self.lines.expired[0] = order.created.price

The custom observer only cares about buy orders, because this is a strategy which only buys to try to make a profit. Sell orders are Market orders and will be executed immediately.

The Close-SMA CrossOver strategy is changed to:

-

Create a Limit order with a price below 1.0% the close price at the moment of the signal

-

A validity for the order of 7 (calendar) days

The resulting chart.

Several orders have expired as can be seen in the new subchart (red squares) and we can also appreciate that between “creation” and “execution” several days happen to be.

Finally the code for this strategy which applies the new observer

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import datetime

import backtrader as bt

import backtrader.feeds as btfeeds

import backtrader.indicators as btind

from orderobserver import OrderObserver

class MyStrategy(bt.Strategy):

params = (

('smaperiod', 15),

('limitperc', 1.0),

('valid', 7),

)

def log(self, txt, dt=None):

''' Logging function fot this strategy'''

dt = dt or self.data.datetime[0]

if isinstance(dt, float):

dt = bt.num2date(dt)

print('%s, %s' % (dt.isoformat(), txt))

def notify_order(self, order):

if order.status in [order.Submitted, order.Accepted]:

# Buy/Sell order submitted/accepted to/by broker - Nothing to do

self.log('ORDER ACCEPTED/SUBMITTED', dt=order.created.dt)

self.order = order

return

if order.status in [order.Expired]:

self.log('BUY EXPIRED')

elif order.status in [order.Completed]:

if order.isbuy():

self.log(

'BUY EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

else: # Sell

self.log('SELL EXECUTED, Price: %.2f, Cost: %.2f, Comm %.2f' %

(order.executed.price,

order.executed.value,

order.executed.comm))

# Sentinel to None: new orders allowed

self.order = None

def __init__(self):

# SimpleMovingAverage on main data

# Equivalent to -> sma = btind.SMA(self.data, period=self.p.smaperiod)

sma = btind.SMA(period=self.p.smaperiod)

# CrossOver (1: up, -1: down) close / sma

self.buysell = btind.CrossOver(self.data.close, sma, plot=True)

# Sentinel to None: new ordersa allowed

self.order = None

def next(self):

if self.order:

# pending order ... do nothing

return

# Check if we are in the market

if self.position:

if self.buysell < 0:

self.log('SELL CREATE, %.2f' % self.data.close[0])

self.sell()

elif self.buysell > 0:

plimit = self.data.close[0] * (1.0 - self.p.limitperc / 100.0)

valid = self.data.datetime.date(0) + \

datetime.timedelta(days=self.p.valid)

self.log('BUY CREATE, %.2f' % plimit)

self.buy(exectype=bt.Order.Limit, price=plimit, valid=valid)

def runstrat():

cerebro = bt.Cerebro()

data = bt.feeds.BacktraderCSVData(dataname='../../datas/2006-day-001.txt')

cerebro.adddata(data)

cerebro.addobserver(OrderObserver)

cerebro.addstrategy(MyStrategy)

cerebro.run()

cerebro.plot()

if __name__ == '__main__':

runstrat()

Saving/Keeping the statistics

As of now backtrader has not implemented any mechanism to track the values

of observers storing them into files. The best way to do it:

-

Open a file in the

startmethod of the strategy -

Write the values down in the

nextmethod of the strategy

Considering the DrawDown observer, it could be done like this

class MyStrategy(bt.Strategy):

def start(self):

self.mystats = open('mystats.csv', 'wb')

self.mystats.write('datetime,drawdown, maxdrawdown\n')

def next(self):

self.mystats.write(self.data.datetime.date(0).strftime('%Y-%m-%d'))

self.mystats.write(',%.2f' % self.stats.drawdown.drawdown[-1])

self.mystats.write(',%.2f' % self.stats.drawdown.maxdrawdown-1])

self.mystats.write('\n')

To save the values of index 0, once all observers have been processed a custom observer which writes to a file could be added as the last observer to the system to save values to a csv file.

Note

The Writer functionality can automate this task.