Pyfolio Integration

Note

Feb 2017

pyfolio APIs have changed and create_full_tear_sheet no longer

has a gross_lev as a named argument.

Consequently the sample below doesn’t work

A first look at the tutorial deemed it as difficult, given the tight integration amongst zipline and pyfolio, but the sample test data available with pyfolio for some other uses is actually pretty useful to decode what’s running behind the scenes and hence the wonder of integration.

The integration of a portfolio tool, namely pyfolio, came up with in

Ticket #108.

Most of the pieces were already in-place in backtrader:

-

Analyzer infrastructure

-

Children analyzer

-

A TimeReturn analyzer

Only a main PyFolio analyzer and 3 easy children analyzer are

needed. Plus a method that relies on one of the dependencies already needed by

pyfolio which is pandas.

The most challenging part … “getting all the dependencies right”.

-

Update of

pandas -

Update of

numpy -

Update of

scikit-lean -

Update of

seaborn

Under Unix-like environments with a C compiler it’s all about time. Under Windows and even with the specific Microsoft compiler installed (in this case the chain for Python 2.7) things failed. But a well known site with a collection of up-to-date packages for Windows helped. Visit it if you ever need it:

The integration wouldn’t be complete if it wasn’t tested and that’s why the usual sample is as always present.

No PyFolio

The sample uses random.randint to decide when to buy/sell, so this is

simply a check that things are working:

$ ./pyfoliotest.py --printout --no-pyfolio --plot

Output:

Len,Datetime,Open,High,Low,Close,Volume,OpenInterest

0001,2005-01-03T23:59:59,38.36,38.90,37.65,38.18,25482800.00,0.00

BUY 1000 @%23.58

0002,2005-01-04T23:59:59,38.45,38.54,36.46,36.58,26625300.00,0.00

BUY 1000 @%36.58

SELL 500 @%22.47

0003,2005-01-05T23:59:59,36.69,36.98,36.06,36.13,18469100.00,0.00

...

SELL 500 @%37.51

0502,2006-12-28T23:59:59,25.62,25.72,25.30,25.36,11908400.00,0.00

0503,2006-12-29T23:59:59,25.42,25.82,25.33,25.54,16297800.00,0.00

SELL 250 @%17.14

SELL 250 @%37.01

There a 3 datas and several buy and sell operations are randomly chosen and scattered over the 2 year default life of the test run

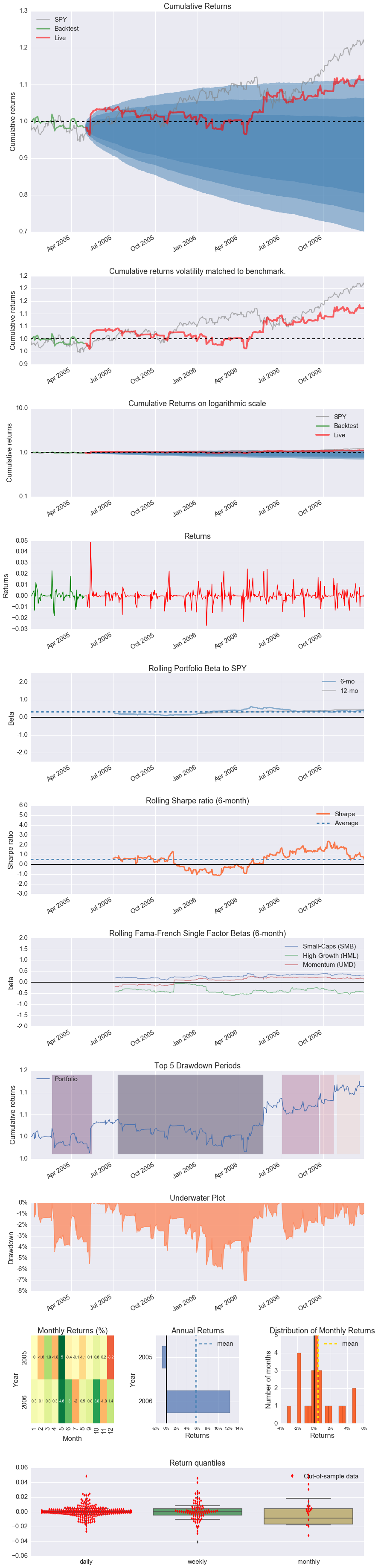

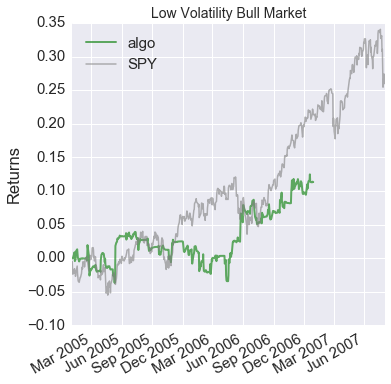

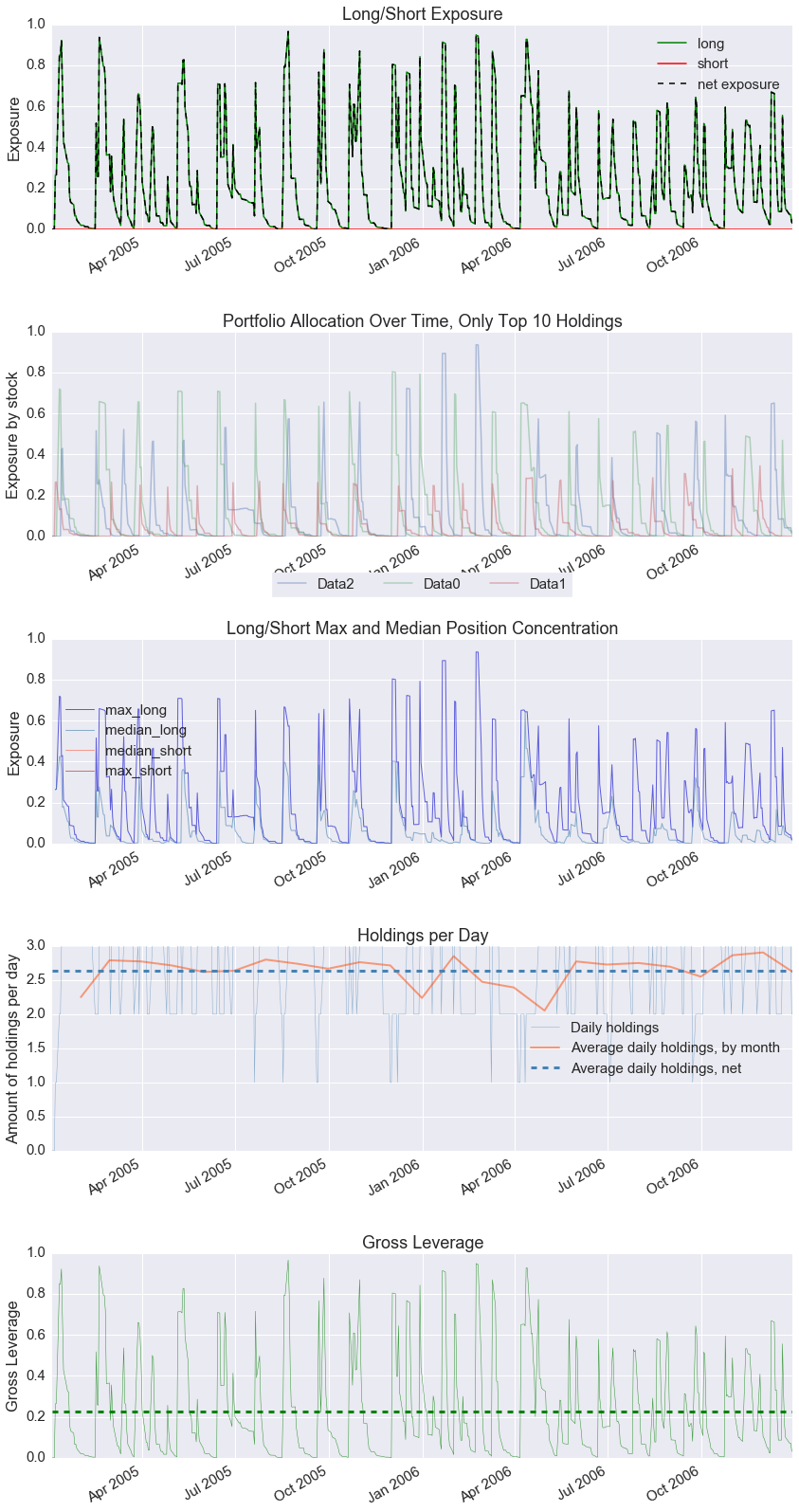

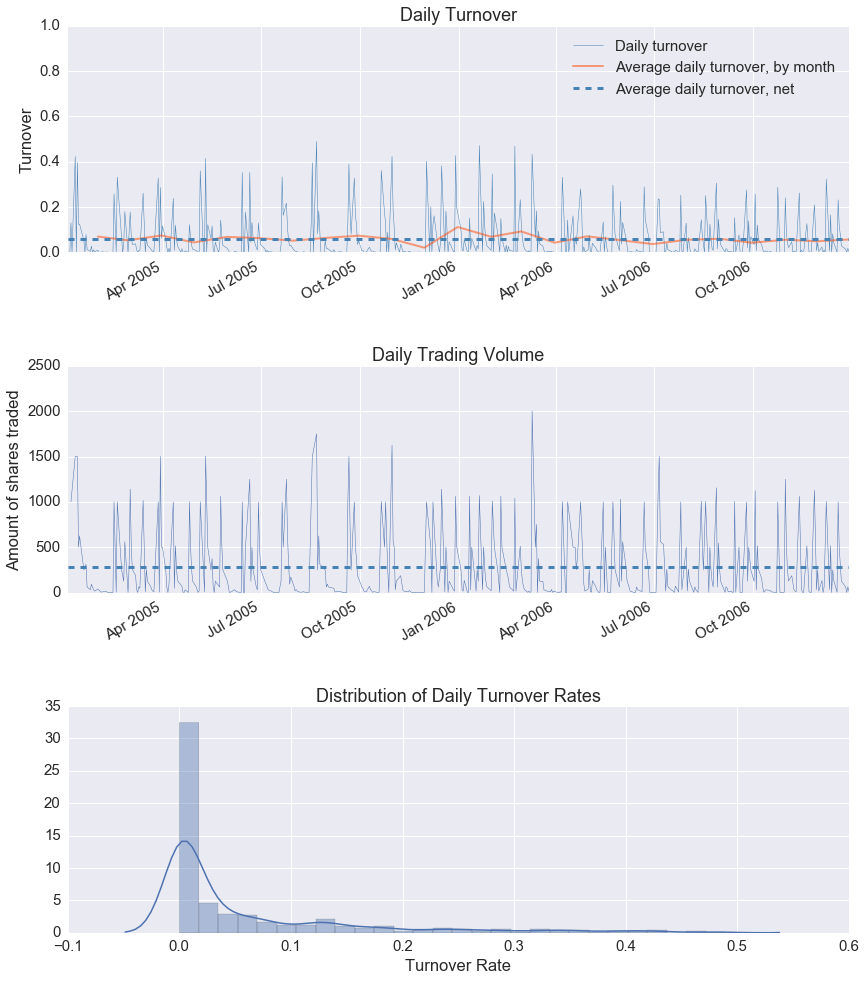

A PyFolio run

pyfolio things work well when running inside a Jupyter Notebook including

inline plotting. Here is the notebook

Note

runstrat gets here [] as argument to run with default arguments

and skip arguments passed by the notebook itself

%matplotlib inline

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import random

import backtrader as bt

class St(bt.Strategy):

params = (

('printout', False),

('stake', 1000),

)

def __init__(self):

pass

def start(self):

if self.p.printout:

txtfields = list()

txtfields.append('Len')

txtfields.append('Datetime')

txtfields.append('Open')

txtfields.append('High')

txtfields.append('Low')

txtfields.append('Close')

txtfields.append('Volume')

txtfields.append('OpenInterest')

print(','.join(txtfields))

def next(self):

if self.p.printout:

# Print only 1st data ... is just a check that things are running

txtfields = list()

txtfields.append('%04d' % len(self))

txtfields.append(self.data.datetime.datetime(0).isoformat())

txtfields.append('%.2f' % self.data0.open[0])

txtfields.append('%.2f' % self.data0.high[0])

txtfields.append('%.2f' % self.data0.low[0])

txtfields.append('%.2f' % self.data0.close[0])

txtfields.append('%.2f' % self.data0.volume[0])

txtfields.append('%.2f' % self.data0.openinterest[0])

print(','.join(txtfields))

# Data 0

for data in self.datas:

toss = random.randint(1, 10)

curpos = self.getposition(data)

if curpos.size:

if toss > 5:

size = curpos.size // 2

self.sell(data=data, size=size)

if self.p.printout:

print('SELL {} @%{}'.format(size, data.close[0]))

elif toss < 5:

self.buy(data=data, size=self.p.stake)

if self.p.printout:

print('BUY {} @%{}'.format(self.p.stake, data.close[0]))

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

cerebro.broker.set_cash(args.cash)

dkwargs = dict()

if args.fromdate:

fromdate = datetime.datetime.strptime(args.fromdate, '%Y-%m-%d')

dkwargs['fromdate'] = fromdate

if args.todate:

todate = datetime.datetime.strptime(args.todate, '%Y-%m-%d')

dkwargs['todate'] = todate

data0 = bt.feeds.BacktraderCSVData(dataname=args.data0, **dkwargs)

cerebro.adddata(data0, name='Data0')

data1 = bt.feeds.BacktraderCSVData(dataname=args.data1, **dkwargs)

cerebro.adddata(data1, name='Data1')

data2 = bt.feeds.BacktraderCSVData(dataname=args.data2, **dkwargs)

cerebro.adddata(data2, name='Data2')

cerebro.addstrategy(St, printout=args.printout)

if not args.no_pyfolio:

cerebro.addanalyzer(bt.analyzers.PyFolio, _name='pyfolio')

results = cerebro.run()

if not args.no_pyfolio:

strat = results[0]

pyfoliozer = strat.analyzers.getbyname('pyfolio')

returns, positions, transactions, gross_lev = pyfoliozer.get_pf_items()

if args.printout:

print('-- RETURNS')

print(returns)

print('-- POSITIONS')

print(positions)

print('-- TRANSACTIONS')

print(transactions)

print('-- GROSS LEVERAGE')

print(gross_lev)

import pyfolio as pf

pf.create_full_tear_sheet(

returns,

positions=positions,

transactions=transactions,

gross_lev=gross_lev,

live_start_date='2005-05-01',

round_trips=True)

if args.plot:

cerebro.plot(style=args.plot_style)

def parse_args(args=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description='Sample for pivot point and cross plotting')

parser.add_argument('--data0', required=False,

default='../../datas/yhoo-1996-2015.txt',

help='Data to be read in')

parser.add_argument('--data1', required=False,

default='../../datas/orcl-1995-2014.txt',

help='Data to be read in')

parser.add_argument('--data2', required=False,

default='../../datas/nvda-1999-2014.txt',

help='Data to be read in')

parser.add_argument('--fromdate', required=False,

default='2005-01-01',

help='Starting date in YYYY-MM-DD format')

parser.add_argument('--todate', required=False,

default='2006-12-31',

help='Ending date in YYYY-MM-DD format')

parser.add_argument('--printout', required=False, action='store_true',

help=('Print data lines'))

parser.add_argument('--cash', required=False, action='store',

type=float, default=50000,

help=('Cash to start with'))

parser.add_argument('--plot', required=False, action='store_true',

help=('Plot the result'))

parser.add_argument('--plot-style', required=False, action='store',

default='bar', choices=['bar', 'candle', 'line'],

help=('Plot style'))

parser.add_argument('--no-pyfolio', required=False, action='store_true',

help=('Do not do pyfolio things'))

import sys

aargs = args if args is not None else sys.argv[1:]

return parser.parse_args(aargs)

runstrat([])

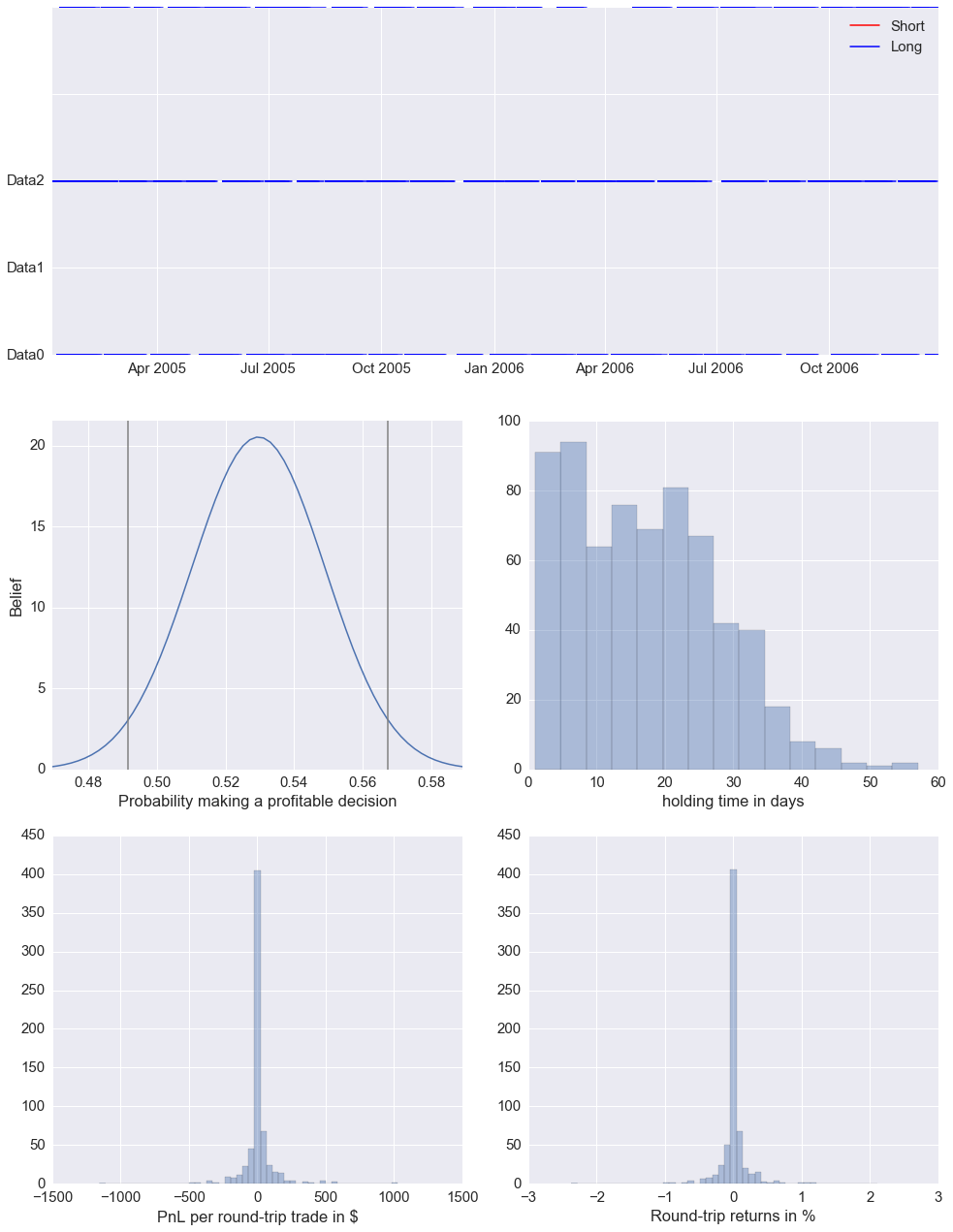

Entire data start date: 2005-01-03

Entire data end date: 2006-12-29

Out-of-Sample Months: 20

Backtest Months: 3

[-0.012 -0.025]

D:drobinWinPython-64bit-2.7.10.3python-2.7.10.amd64libsite-packagespyfolioplotting.py:1210: FutureWarning: .resample() is now a deferred operation

use .resample(...).mean() instead of .resample(...)

**kwargs)

<matplotlib.figure.Figure at 0x23982b70>

Usage of the sample:

$ ./pyfoliotest.py --help

usage: pyfoliotest.py [-h] [--data0 DATA0] [--data1 DATA1] [--data2 DATA2]

[--fromdate FROMDATE] [--todate TODATE] [--printout]

[--cash CASH] [--plot] [--plot-style {bar,candle,line}]

[--no-pyfolio]

Sample for pivot point and cross plotting

optional arguments:

-h, --help show this help message and exit

--data0 DATA0 Data to be read in (default:

../../datas/yhoo-1996-2015.txt)

--data1 DATA1 Data to be read in (default:

../../datas/orcl-1995-2014.txt)

--data2 DATA2 Data to be read in (default:

../../datas/nvda-1999-2014.txt)

--fromdate FROMDATE Starting date in YYYY-MM-DD format (default:

2005-01-01)

--todate TODATE Ending date in YYYY-MM-DD format (default: 2006-12-31)

--printout Print data lines (default: False)

--cash CASH Cash to start with (default: 50000)

--plot Plot the result (default: False)

--plot-style {bar,candle,line}

Plot style (default: bar)

--no-pyfolio Do not do pyfolio things (default: False)