Canonical vs Non-Canonical Indicators

The question has shown up several times more or less like this:

- How is this or that best/canonically implemented with backtrader?

Being one of the goals of backtrader to be flexible to support as many situations and use cases as possible, the answer is easy: "In at least a couple of ways". Summarized for indicators, for which the question most often happens:

-

100% declarative in the

__init__method -

100% step-by-step in the

nextmethod -

Mixing both of the above for complex scenarios in which the declarative part cannot cover all needed calculations

A quick view of the built-in indicators in backtrader reveals that all of them are implemented in a declarative manner. The reasons

-

Easier to do

-

Easier to read

-

More elegant

-

Vectorized and even-based implementations are automatically managed

What ?!?! Auto-implemented Vectorization??

Yes. If an indicator is implemented entirely inside the __init_ method, the

magic of metaclasses and operator overloading in Python will deliver the

following

-

A vectorized implementation (default setting when running a backtest)

-

An event-based implementation (for example for live trading)

On the other hand and if any part of an indicator which is implemented in the

next method:

-

This is the code directly used for an event-based run.

-

Vectorization will be simulated by calling the

nextmethod in the background for each data pointNote

This means that even if a particular indicator does not have a vectorized implementation, all others which have it, will still run vectorized

Money Flow Index: an Example

Community User @Rodrigo

Brito posted a

version of the "Money Flow Index" indicator which used the next method for

the implementation.

The code

class MFI(bt.Indicator):

lines = ('mfi', 'money_flow_raw', 'typical', 'money_flow_pos', 'money_flow_neg')

plotlines = dict(

money_flow_raw=dict(_plotskip=True),

money_flow_pos=dict(_plotskip=True),

money_flow_neg=dict(_plotskip=True),

typical=dict(_plotskip=True),

)

params = (

('period', 14),

)

def next(self):

typical_price = (self.data.close[0] + self.data.low[0] + self.data.high[0]) / 3

money_flow_raw = typical_price * self.data.volume[0]

self.lines.typical[0] = typical_price

self.lines.money_flow_raw[0] = money_flow_raw

self.lines.money_flow_pos[0] = money_flow_raw if self.lines.typical[0] >= self.lines.typical[-1] else 0

self.lines.money_flow_neg[0] = money_flow_raw if self.lines.typical[0] <= self.lines.typical[-1] else 0

pos_period = math.fsum(self.lines.money_flow_pos.get(size=self.p.period))

neg_period = math.fsum(self.lines.money_flow_neg.get(size=self.p.period))

if neg_period == 0:

self.lines.mfi[0] = 100

return

self.lines.mfi[0] = 100 - 100 / (1 + pos_period / neg_period)

Note

Kept as originally posted including the long lines for which one has to scroll horizontally

@Rodrigo Brito already

notices that the usage of temporary lines is (all lines except mfi) is

something which probably admits optimization. Indeed, but in the humble opinion

of the author*, actually everything does admit a bit of optimization.

To have common working grounds, one can use the "Money Flow Index" definition by StockCharts and see that the implementation above is good. Here is the link:

With that in the hand, a quick Canonical implementation of the MFI

indicator

class MFI_Canonical(bt.Indicator):

lines = ('mfi',)

params = dict(period=14)

def __init__(self):

tprice = (self.data.close + self.data.low + self.data.high) / 3.0

mfraw = tprice * self.data.volume

flowpos = bt.ind.SumN(mfraw * (tprice > tprice(-1)), period=self.p.period)

flowneg = bt.ind.SumN(mfraw * (tprice < tprice(-1)), period=self.p.period)

mfiratio = bt.ind.DivByZero(flowpos, flowneg, zero=100.0)

self.l.mfi = 100.0 - 100.0 / (1.0 + mfiratio)

One should be able to immediately notice

-

A single line

mfiis defined. No temporaries are there. -

Things seem cleaner with no need for

[0]array indexing -

No single

ifhere or there -

More compact whilst more readable

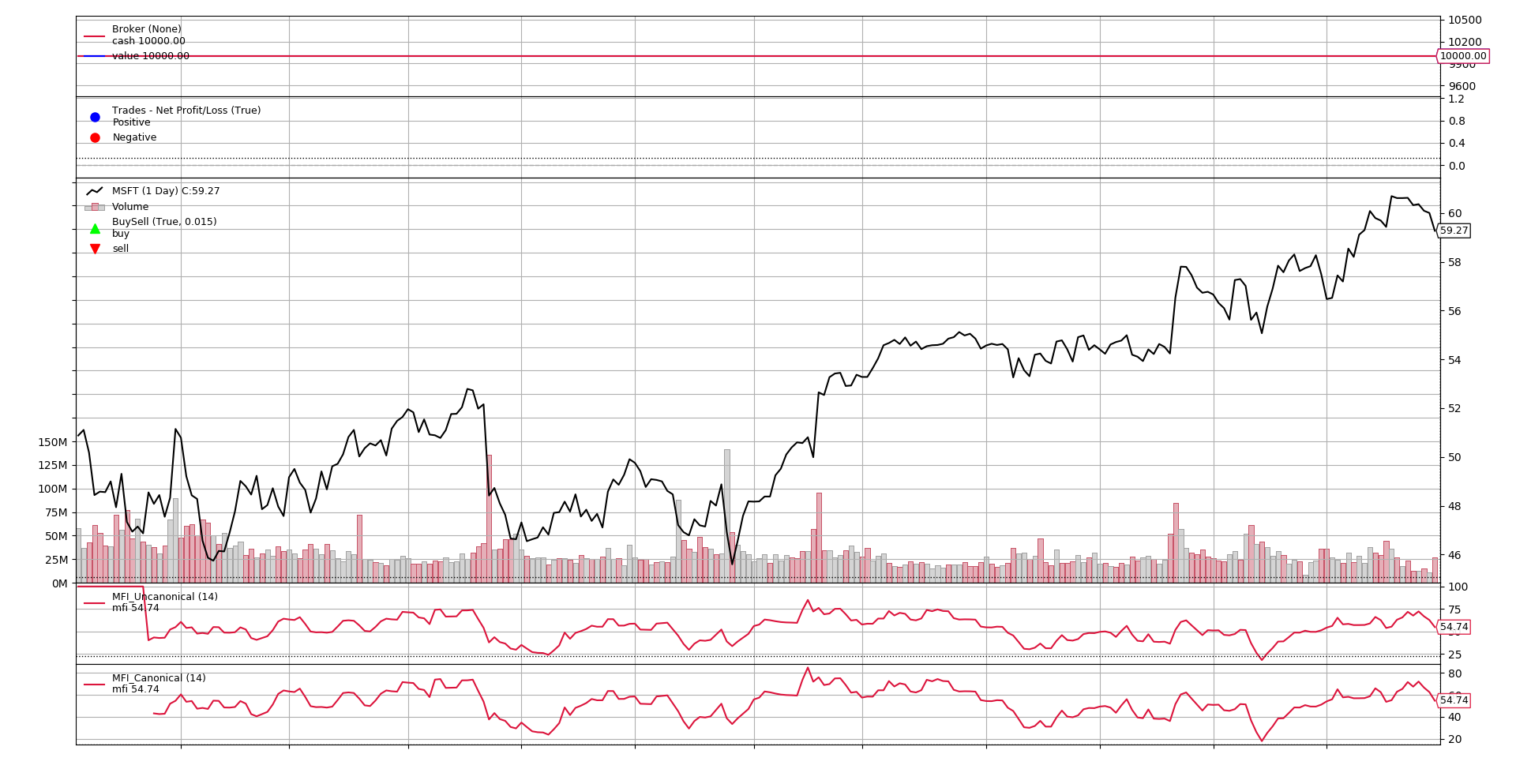

Should one plot a graph of both run against the same data set, it would look like this

The chart shows that both the Canonical and Non-Canonical versions show the same values and development, except at the beginning.

-

The Non-Canonical version is delivering values from the very start

-

It is delivering non-meaningful values (100.0 until it deliver 1 extra value which is also not good) because it cannot properly deliver

In contrast:

-

The Canonical version automatically starts delivering values after the minimum warm-up period has been reached.

-

No human intervention has been needed (it must for sure be "Articifial Intelligence" or "Machine Learning", ... pun intended)

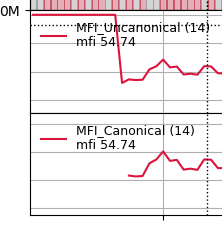

See a close-up picture of the affected area

Note

One could of course try to alleviate this situation in the Non-Canonical version by doing this:

- Subclassing from

bt.ind.PeriodNwhich already has aperiodparam and knows what to do with it (and callingsuperduring__init__)

Notice also that the Canonical version does also account, like the

step-by-step next code for a possible division-by-zero situation in the

formula.

if neg_period == 0:

self.lines.mfi[0] = 100

return

self.lines.mfi[0] = 100 - 100 / (1 + pos_period / neg_period)

whereas this is the other way to do it

mfiratio = bt.ind.DivByZero(flowpos, flowneg, zero=100.0)

self.l.mfi = 100.0 - 100.0 / (1.0 + mfiratio)

Instead of having many lines, a return statement and different assignments to

the output line, there is s single declaration of the mfiratio calculation

and a single assignment (following the StockCharts formula) to the output

line mfi.

Conclusion

Hopefully, this sheds some light as to what the differences can be when

implementing something in the Canonical (i.e.: declarative in __init_) or

Non-Canonical way (step by step with array indexing in next)