Automating BackTesting

So far all backtrader examples and working samples have started from scratch

creating a main Python module which loads datas, strategies, observers and

prepares cash and commission schemes.

One of the goals of algorithmic trading is the automation of trading and given that backtrader is a backtesting platform intented to check trading algorithms (hence is an algotrading platform), automating the use of backtrader was an obvious goal.

When installed backtrader provides 2 entry points in the form of

scripts/executables which which automates most tasks:

bt-run-pya script which uses the codebase from the next item

and

-

btrun(executable)Entry point created by

setuptoolsduring packaging. The executable offers advantages under Windows where in theory no errors about “path/file not found” will happen.

The description below applies equally to both tools.

btrun allows the end user to:

-

Say which data feeds have to be loaded

-

Set the format to load the datas

-

Specify the date range for the datas

-

Pass parameters to Cerebro

- Disable standard observers

This was an original extra switch before the “Cerebro” parameters were implemented. As such and if a parameter to cerebro with regards to Standard Observers is passed, this will be ignored (parameter

stdstatsto Cerebro) -

Load one or more observers (example:

DrawDown) from the built-in ones or from a python module -

Set the cash and commission scheme parameters for the broker (commission, margin, mult)

-

Enable plotting, controlling the amount of charts and style to present the data

-

Add a parametrized writer to the system

And finally what should be the core competence:

-

Load a strategy (a built-in one or from a Python module)

-

Pass parameters to the loaded strategy

See below for the Usage of the script.

Applying a User Defined Strategy

Let’s consider the following strategy which:

-

Simply loads a SimpleMovingAverage (default period 15)

-

Prints outs

-

Is in a file named

mymod.py

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import backtrader as bt

import backtrader.indicators as btind

class MyTest(bt.Strategy):

params = (('period', 15),)

def log(self, txt, dt=None):

''' Logging function fot this strategy'''

dt = dt or self.data.datetime[0]

if isinstance(dt, float):

dt = bt.num2date(dt)

print('%s, %s' % (dt.isoformat(), txt))

def __init__(self):

sma = btind.SMA(period=self.p.period)

def next(self):

ltxt = '%d, %.2f, %.2f, %.2f, %.2f, %.2f, %.2f'

self.log(ltxt %

(len(self),

self.data.open[0], self.data.high[0],

self.data.low[0], self.data.close[0],

self.data.volume[0], self.data.openinterest[0]))

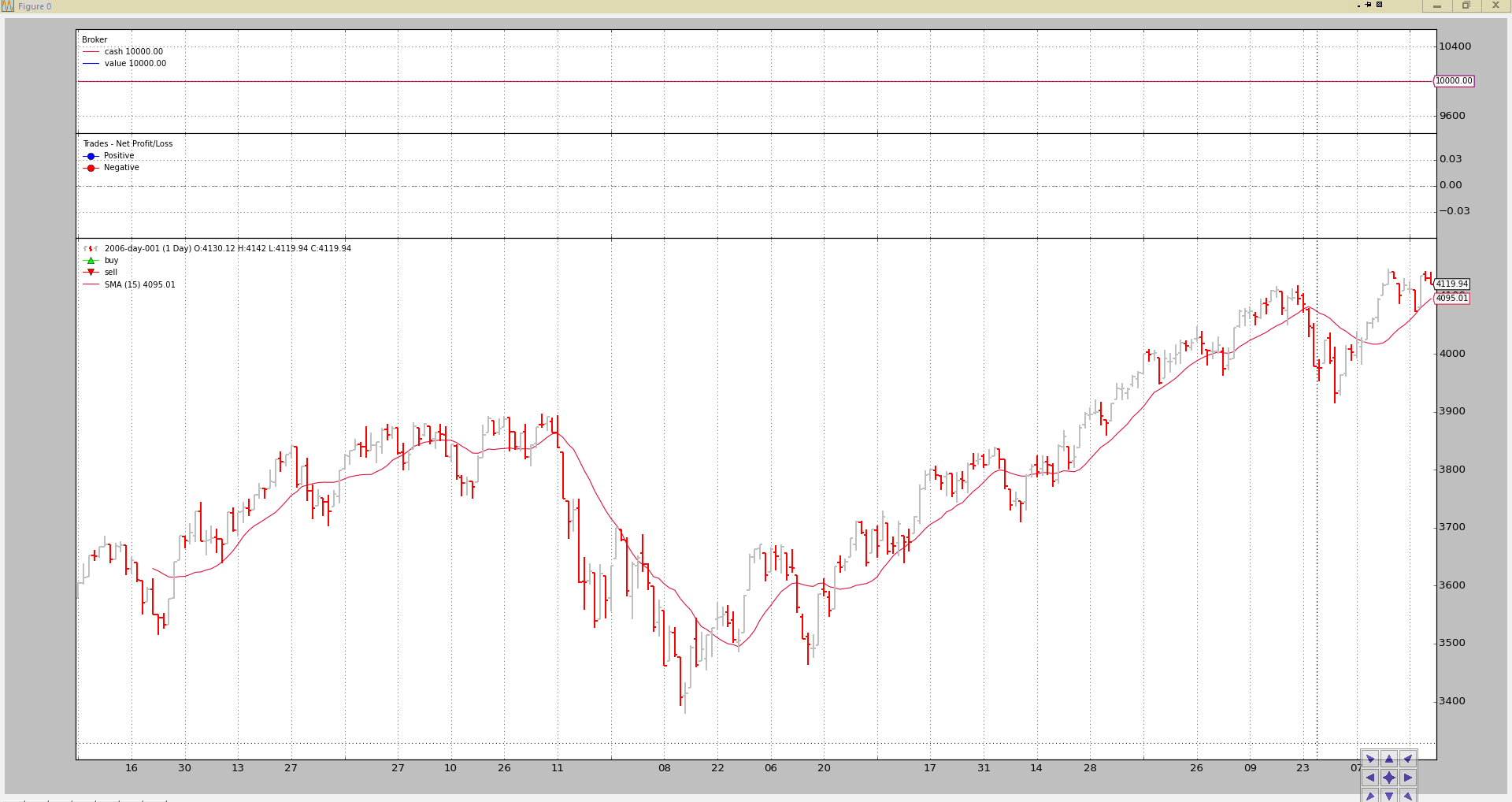

Executing the strategy with the usual testing sample is easy: easy:

btrun --csvformat btcsv \

--data ../../datas/2006-day-001.txt \

--strategy mymod.py

The chart output

The console output:

2006-01-20T23:59:59+00:00, 15, 3593.16, 3612.37, 3550.80, 3550.80, 0.00, 0.00

2006-01-23T23:59:59+00:00, 16, 3550.24, 3550.24, 3515.07, 3544.31, 0.00, 0.00

2006-01-24T23:59:59+00:00, 17, 3544.78, 3553.16, 3526.37, 3532.68, 0.00, 0.00

2006-01-25T23:59:59+00:00, 18, 3532.72, 3578.00, 3532.72, 3578.00, 0.00, 0.00

...

...

2006-12-22T23:59:59+00:00, 252, 4109.86, 4109.86, 4072.62, 4073.50, 0.00, 0.00

2006-12-27T23:59:59+00:00, 253, 4079.70, 4134.86, 4079.70, 4134.86, 0.00, 0.00

2006-12-28T23:59:59+00:00, 254, 4137.44, 4142.06, 4125.14, 4130.66, 0.00, 0.00

2006-12-29T23:59:59+00:00, 255, 4130.12, 4142.01, 4119.94, 4119.94, 0.00, 0.00

Same strategy but:

- Setting the parameter

periodto 50

The command line:

btrun --csvformat btcsv \

--data ../../datas/2006-day-001.txt \

--plot \

--strategy mymod.py:period=50

The chart output.

Note

if no .py extension is given, bt-run will add it.

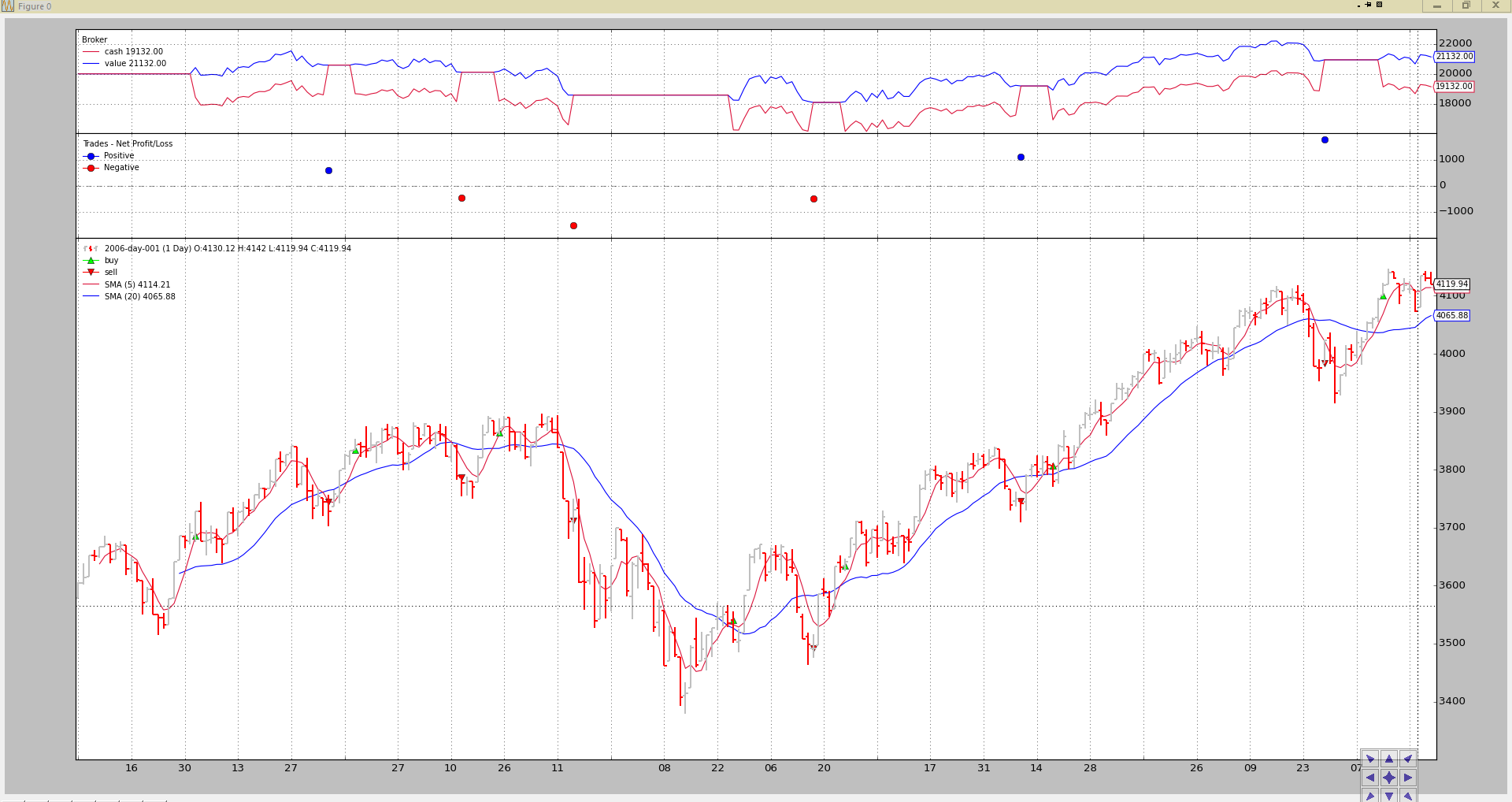

Using a built-in Strategy

backtrader will slowly be including sample (textbook) strategies. Along with

the bt-run.py script a standard Simple Moving Average CrossOver strategy

is included. The name:

-

SMA_CrossOver -

Parameters

-

fast(default10) period of the fast moving average -

slow(default30) period of the slow moving average

-

The strategy buys if the fast moving average crosses up the fast and sells (only if it has bought before) upon the fast moving average crossing down the slow moving average.

The code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import backtrader as bt

import backtrader.indicators as btind

class SMA_CrossOver(bt.Strategy):

params = (('fast', 10), ('slow', 30))

def __init__(self):

sma_fast = btind.SMA(period=self.p.fast)

sma_slow = btind.SMA(period=self.p.slow)

self.buysig = btind.CrossOver(sma_fast, sma_slow)

def next(self):

if self.position.size:

if self.buysig < 0:

self.sell()

elif self.buysig > 0:

self.buy()

Standard execution:

btrun --csvformat btcsv \

--data ../../datas/2006-day-001.txt \

--plot \

--strategy :SMA_CrossOver

Notice the :. The standard notation (see below) to load a strategy is:

module:stragegy:kwargs

With the following rules:

-

If module is there and strategy is specified, then that strategy will be used

-

If module is there but no strategy is specified, the 1st strategy found in the module will be returned

-

If no module is specified, “strategy” is assumed to refer to a strategy in the

backtraderpackage -

If module and/or strategy are there, if kwargs are present they will be passed to the corresponding strategy

Note

The same notation and rules apply to --observer, --analyzer and

--indicator options

Obviously for the corresponding object types

The output

One last example adding commission schemes, cash and changing the parameters:

btrun --csvformat btcsv \

--data ../../datas/2006-day-001.txt \

--plot \

--cash 20000 \

--commission 2.0 \

--mult 10 \

--margin 2000 \

--strategy :SMA_CrossOver:fast=5,slow=20

The output

We have backtested the strategy:

-

Changing the moving average periods

-

Setting a new starting cash

-

Putting a commission scheme in place for a futures-like instrument

See the continuous variations in cash with each bar, as cash is adjusted for the futures-like instrument daily changes

Using no Strategy

This is a an over-statement. A strategy will be applied, but you can ommit any kind of strategy and a default backtrader.Strategy will be added.

Analyzers, Observers and Indicators will be automatically injected in the strategy.

An example:

btrun --csvformat btcsv \

--data ../../datas/2006-day-001.txt \

--cash 20000 \

--commission 2.0 \

--mult 10 \

--margin 2000 \

--nostdstats \

--observer :Broker

This will do not much but serves the purpose:

-

A default backtrader.Strategy is added in the background

-

Cerebro will not instantiate the regular

stdstatsobservers (Broker, BuySell, Trades) -

A

Brokerobserver is added manually

As mentioned above, the nostdstats is a legacy parameter. Newer versions of

btrun can pass parameters directly to Cerebro. An equivalent invocation

would be:

btrun --csvformat btcsv \

--data ../../datas/2006-day-001.txt \

--cash 20000 \

--commission 2.0 \

--mult 10 \

--margin 2000 \

--cerebro stdstats=False \

--observer :Broker

Adding Analyzers

btrun also supports adding Analyzers with the same syntax used for the

strategies to choose between internal/external analyzers.

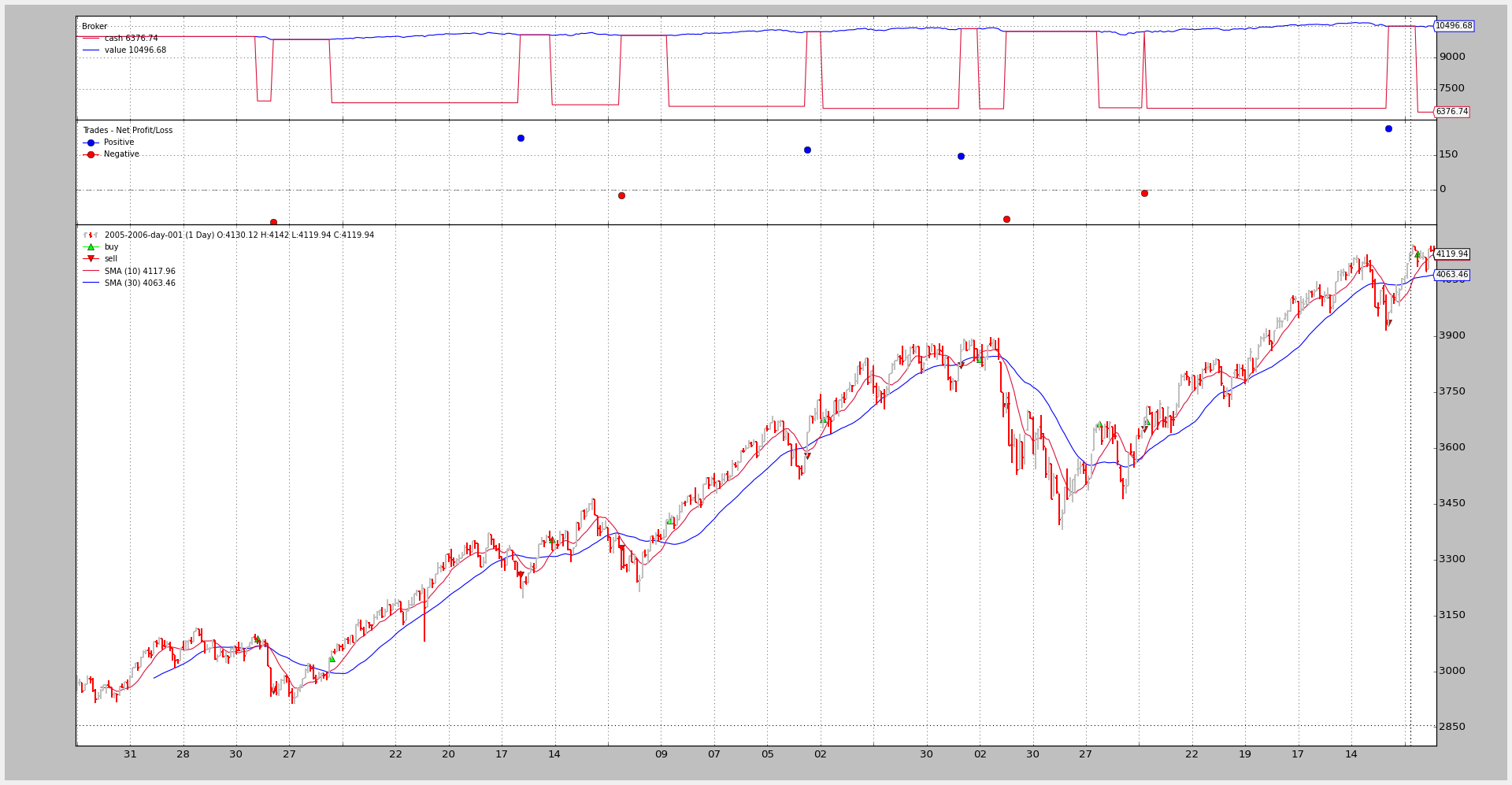

Example with a SharpeRatio analysis for the years 2005-2006:

btrun --csvformat btcsv \

--data ../../datas/2005-2006-day-001.txt \

--strategy :SMA_CrossOver \

--analyzer :SharpeRatio

The console output is nothing.

If a printout of the Analyzer results is wished, it must be specified with:

-

--pranalyzerwhich defaults to calling the next one (unless the Analyzer has overriden the proper method) -

--ppranalyzerwhich uses thepprintmodule to print the results

Note

The two printing options were implemented before writers were part of

backtrader. Adding a writer without csv output will achieve the same (and

the output has been improved)

Extending the example from above:

btrun --csvformat btcsv \

--data ../../datas/2005-2006-day-001.txt \

--strategy :SMA_CrossOver \

--analyzer :SharpeRatio \

--plot \

--pranalyzer

====================

== Analyzers

====================

##########

sharperatio

##########

{'sharperatio': 11.647332609673256}

Good strategy!!! (Pure luck for the example actually which also bears no commissions)

The chart (which simply shows the Analyzer is not in the plot, because Analyzers cannot be plotted, they aren’t lines objects)

The same example but using a writer argument:

btrun --csvformat btcsv \

--data ../../datas/2005-2006-day-001.txt \

--strategy :SMA_CrossOver \

--analyzer :SharpeRatio \

--plot \

--writer

===============================================================================

Cerebro:

-----------------------------------------------------------------------------

- Datas:

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

- Data0:

- Name: 2005-2006-day-001

- Timeframe: Days

- Compression: 1

-----------------------------------------------------------------------------

- Strategies:

+++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

- SMA_CrossOver:

*************************************************************************

- Params:

- fast: 10

- slow: 30

- _movav: SMA

*************************************************************************

- Indicators:

.......................................................................

- SMA:

- Lines: sma

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

- Params:

- period: 30

.......................................................................

- CrossOver:

- Lines: crossover

- Params: None

*************************************************************************

- Observers:

.......................................................................

- Broker:

- Lines: cash, value

- Params: None

.......................................................................

- BuySell:

- Lines: buy, sell

- Params: None

.......................................................................

- Trades:

- Lines: pnlplus, pnlminus

- Params: None

*************************************************************************

- Analyzers:

.......................................................................

- Value:

- Begin: 10000.0

- End: 10496.68

.......................................................................

- SharpeRatio:

- Params: None

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

- Analysis:

- sharperatio: 11.6473326097

Adding Indicators and Observers

As with Strategies and Analyzers btrun can also add:

Indicators

and

Observers

The syntax is exactly the same as seen above when adding a Broker observer.

Let’s repeat the example but adding a Stochastic, the Broker and having

a look at the plot (we’ll change some parameters):

btrun --csvformat btcsv \

--data ../../datas/2006-day-001.txt \

--nostdstats \

--observer :Broker \

--indicator :Stochastic:period_dslow=5 \

--plot

The chart

Plotting Control

Most of the above examples have used the following option:

--plotwhich has activated the creation a default plot

More control can be achieved by adding kwargs to the --plot

option

--plot style="candle"for example to plot with candlesticks instead of plotting with aLineOnClosestyle (which is the plotting default)

The invocation:

btrun --csvformat btcsv \

--data ../../datas/2006-day-001.txt \

--nostdstats \

--observer :Broker \

--indicator :Stochastic:period_dslow=5 \

--plot style=\"candle\"

Note

The quotes around candle are quoted with backslashed \\ because the

example is being run in a bash shell which removes that before passing the

arguments to the script.

Backslash quoting is needed in this case to ensure “bar” makes it to the script and can be evaluated as a string

The chart

Usage of the script

Directly from the script:

$ btrun --help

usage: btrun-script.py [-h] --data DATA [--cerebro [kwargs]] [--nostdstats]

[--format {yahoocsv_unreversed,vchart,vchartcsv,yahoo,mt4csv,ibdata,sierracsv,yahoocsv,btcsv,vcdata}]

[--fromdate FROMDATE] [--todate TODATE]

[--timeframe {microseconds,seconds,weeks,months,minutes,days,years}]

[--compression COMPRESSION]

[--resample RESAMPLE | --replay REPLAY]

[--strategy module:name:kwargs]

[--signal module:signaltype:name:kwargs]

[--observer module:name:kwargs]

[--analyzer module:name:kwargs]

[--pranalyzer | --ppranalyzer]

[--indicator module:name:kwargs] [--writer [kwargs]]

[--cash CASH] [--commission COMMISSION]

[--margin MARGIN] [--mult MULT] [--interest INTEREST]

[--interest_long] [--slip_perc SLIP_PERC]

[--slip_fixed SLIP_FIXED] [--slip_open]

[--no-slip_match] [--slip_out] [--flush]

[--plot [kwargs]]

Backtrader Run Script

optional arguments:

-h, --help show this help message and exit

--resample RESAMPLE, -rs RESAMPLE

resample with timeframe:compression values

--replay REPLAY, -rp REPLAY

replay with timeframe:compression values

--pranalyzer, -pralyzer

Automatically print analyzers

--ppranalyzer, -ppralyzer

Automatically PRETTY print analyzers

--plot [kwargs], -p [kwargs]

Plot the read data applying any kwargs passed

For example:

--plot style="candle" (to plot candlesticks)

Data options:

--data DATA, -d DATA Data files to be added to the system

Cerebro options:

--cerebro [kwargs], -cer [kwargs]

The argument can be specified with the following form:

- kwargs

Example: "preload=True" which set its to True

The passed kwargs will be passed directly to the cerebro

instance created for the execution

The available kwargs to cerebro are:

- preload (default: True)

- runonce (default: True)

- maxcpus (default: None)

- stdstats (default: True)

- live (default: False)

- exactbars (default: False)

- preload (default: True)

- writer (default False)

- oldbuysell (default False)

- tradehistory (default False)

--nostdstats Disable the standard statistics observers

--format {yahoocsv_unreversed,vchart,vchartcsv,yahoo,mt4csv,ibdata,sierracsv,yahoocsv,btcsv,vcdata}, --csvformat {yahoocsv_unreversed,vchart,vchartcsv,yahoo,mt4csv,ibdata,sierracsv,yahoocsv,btcsv,vcdata}, -c {yahoocsv_unreversed,vchart,vchartcsv,yahoo,mt4csv,ibdata,sierracsv,yahoocsv,btcsv,vcdata}

CSV Format

--fromdate FROMDATE, -f FROMDATE

Starting date in YYYY-MM-DD[THH:MM:SS] format

--todate TODATE, -t TODATE

Ending date in YYYY-MM-DD[THH:MM:SS] format

--timeframe {microseconds,seconds,weeks,months,minutes,days,years}, -tf {microseconds,seconds,weeks,months,minutes,days,years}

Ending date in YYYY-MM-DD[THH:MM:SS] format

--compression COMPRESSION, -cp COMPRESSION

Ending date in YYYY-MM-DD[THH:MM:SS] format

Strategy options:

--strategy module:name:kwargs, -st module:name:kwargs

This option can be specified multiple times.

The argument can be specified with the following form:

- module:classname:kwargs

Example: mymod:myclass:a=1,b=2

kwargs is optional

If module is omitted then class name will be sought in

the built-in strategies module. Such as in:

- :name:kwargs or :name

If name is omitted, then the 1st strategy found in the mod

will be used. Such as in:

- module or module::kwargs

Signals:

--signal module:signaltype:name:kwargs, -sig module:signaltype:name:kwargs

This option can be specified multiple times.

The argument can be specified with the following form:

- signaltype:module:signaltype:classname:kwargs

Example: longshort+mymod:myclass:a=1,b=2

signaltype may be ommited: longshort will be used

Example: mymod:myclass:a=1,b=2

kwargs is optional

signaltype will be uppercased to match the defintions

fromt the backtrader.signal module

If module is omitted then class name will be sought in

the built-in signals module. Such as in:

- LONGSHORT::name:kwargs or :name

If name is omitted, then the 1st signal found in the mod

will be used. Such as in:

- module or module:::kwargs

Observers and statistics:

--observer module:name:kwargs, -ob module:name:kwargs

This option can be specified multiple times.

The argument can be specified with the following form:

- module:classname:kwargs

Example: mymod:myclass:a=1,b=2

kwargs is optional

If module is omitted then class name will be sought in

the built-in observers module. Such as in:

- :name:kwargs or :name

If name is omitted, then the 1st observer found in the

will be used. Such as in:

- module or module::kwargs

Analyzers:

--analyzer module:name:kwargs, -an module:name:kwargs

This option can be specified multiple times.

The argument can be specified with the following form:

- module:classname:kwargs

Example: mymod:myclass:a=1,b=2

kwargs is optional

If module is omitted then class name will be sought in

the built-in analyzers module. Such as in:

- :name:kwargs or :name

If name is omitted, then the 1st analyzer found in the

will be used. Such as in:

- module or module::kwargs

Indicators:

--indicator module:name:kwargs, -ind module:name:kwargs

This option can be specified multiple times.

The argument can be specified with the following form:

- module:classname:kwargs

Example: mymod:myclass:a=1,b=2

kwargs is optional

If module is omitted then class name will be sought in

the built-in analyzers module. Such as in:

- :name:kwargs or :name

If name is omitted, then the 1st analyzer found in the

will be used. Such as in:

- module or module::kwargs

Writers:

--writer [kwargs], -wr [kwargs]

This option can be specified multiple times.

The argument can be specified with the following form:

- kwargs

Example: a=1,b=2

kwargs is optional

It creates a system wide writer which outputs run data

Please see the documentation for the available kwargs

Cash and Commission Scheme Args:

--cash CASH, -cash CASH

Cash to set to the broker

--commission COMMISSION, -comm COMMISSION

Commission value to set

--margin MARGIN, -marg MARGIN

Margin type to set

--mult MULT, -mul MULT

Multiplier to use

--interest INTEREST Credit Interest rate to apply (0.0x)

--interest_long Apply credit interest to long positions

--slip_perc SLIP_PERC

Enable slippage with a percentage value

--slip_fixed SLIP_FIXED

Enable slippage with a fixed point value

--slip_open enable slippage for when matching opening prices

--no-slip_match Disable slip_match, ie: matching capped at

high-low if slippage goes over those limits

--slip_out with slip_match enabled, match outside high-low

--flush flush the output - useful under win32 systems