Kalman et al.

Note

The support for the directives below starts with commit

1146c83d9f9832630e97daab3ec7359705dc2c77 in the development branch

Release 1.9.30.x will be the 1st to include it.

One of the original goals of backtrader was to be pure python, i.e.: to only

use packages available in the standard distribution. A single exception was

made with matplotlib to have plotting without reinventing the

wheel. Although is imported at the latest possible moment to avoid disrupting

standard operations which may not require plotting at all (and avoiding errors

if not installed and not wished)

A 2nd exception was partially made with pytz when adding support for

timezones with the advent of live data feeds which may reside outside of the

local timezone. Again the import action happens in the background and only if

pytz is available (the user may choose to pass pytz instances)

But the moment has come to make a full exception, because backtraders are

using well known packages like numpy, pandas, statsmodel and some

more modest ones like pykalman. Or else inclusion in the platform of things

which use those packages.

Some examples from the community:

This wish was added to the quick roadmap sketched here:

The declarative approach

Key in keeping the original spirit of backtrader and at the same allowing the use of those packages is to not force pure python users to have to install those packages.

Although this may seem challenging and prone to multiple conditional statements here and there, together with exception handling, the approach both internally in the platform and externally for users is to rely on the same principles already used to develop other concepts, like for example parameters (named params) for most objects.

Let’s recall how one defines an Indicator accepting params and defining

lines:

class MyIndicator(bt.Indicator):

lines = ('myline',)

params = (

('period', 50),

)

With the parameter period later being addressable as

self.params.period or self.p.period as in:

def __init__(self):

print('my period is:', self.p.period)

and the current value in the line as self.lines.myline or self.l.myline

as in:

def next(self):

print('mylines[0]:', self.lines.myline[0])

This not being particularly useful, just showing the declarative approach of the params background machinery which also features proper support for inheritance (including multiple inheritance)

Introducing packages

Using the same declarative technique (some would call it metaprogramming) the support for foreign packages is available as:

class MyIndicator(bt.Indicator):

packages = ('pandas',)

lines = ('myline',)

params = (

('period', 50),

)

Blistering barnacles!!! It seems just another declaration. The first question for the implementer of the indicator would be:

- Do I have to manually import ``pandas``?

And the answer is a straightforward: No. The background machinery will

import pandas and make it available in the module in which MyIndicator

is defined. One could now do the following in next:

def next(self):

print('mylines[0]:', pandas.SomeFunction(self.lines.myline[0]))

The packages directive can be used also to:

-

Import multiple packages in one single declaration

-

Assign the import to an alias ala

import pandas as pd

Let’s say that statsmodel is also wished as sm to complete

pandas.SomeFunction:

class MyIndicator(bt.Indicator):

packages = ('pandas', ('statsmodel', 'sm'),)

lines = ('myline',)

params = (

('period', 50),

)

def next(self):

print('mylines[0]:', sm.XX(pandas.SomeFunction(self.lines.myline[0])))

statsmodel has been imported as sm and is available. It simply takes

passing an iterable (a tuple is the backtrader convention) with the name

of the package and the wished alias.

Adding frompackages

Python is well known for the constant lookup for things which is one of the reasons for the language to be fantastic with regards to dynamism, introspection facilities and metaprogramming. At the same time is also one of the causes for not being able to deliver the same performance.

One of the usual speed ups is to remove lookup into modules by directly

importing symbols from the modules, to have local lookups. With our

SomeFunction from pandas this would look like:

from pandas import SomeFunction

or with an alias:

from pandas import SomeFunction as SomeFunc

backtrader offers support for both with the frompackages

directive. Let’s rework MyIndicator:

class MyIndicator(bt.Indicator):

frompackages = (('pandas', 'SomeFunction'),)

lines = ('myline',)

params = (

('period', 50),

)

def next(self):

print('mylines[0]:', SomeFunction(self.lines.myline[0]))

Of course, this starts adding more parenthesis. For example if two (2) things

are going to be imported from pandas, it would seem like this:

class MyIndicator(bt.Indicator):

frompackages = (('pandas', ['SomeFunction', 'SomeFunction2']),)

lines = ('myline',)

params = (

('period', 50),

)

def next(self):

print('mylines[0]:', SomeFunction2(SomeFunction(self.lines.myline[0])))

Where for the sake of clarity SomeFunction and SomeFunction2 have been

put in in a list instead of a tuple, to have square brackets, []

and be able to read it it a bit better.

One can also alias SomeFunction to for example SFunc. The full example:

class MyIndicator(bt.Indicator):

frompackages = (('pandas', [('SomeFunction', 'SFunc'), 'SomeFunction2']),)

lines = ('myline',)

params = (

('period', 50),

)

def next(self):

print('mylines[0]:', SomeFunction2(SFunc(self.lines.myline[0])))

And importing from different packages is possible at the expense of more parenthesis. Of course line breaks and indentation do help:

class MyIndicator(bt.Indicator):

frompackages = (

('pandas', [('SomeFunction', 'SFunc'), 'SomeFunction2']),

('statsmodel', 'XX'),

)

lines = ('myline',)

params = (

('period', 50),

)

def next(self):

print('mylines[0]:', XX(SomeFunction2(SFunc(self.lines.myline[0]))))

Using inheritance

Both packages and frompackages support (multiple) inheritance. There

could for example be a base class which adds numpy support to all

subclasses:

class NumPySupport(object):

packages = ('numpy',)

class MyIndicator(bt.Indicator, NumPySupport):

packages = ('pandas',)

MyIndicator will require from the background machinery the import of both

numpy and pandas and will be able to use them.

Introducing Kalman and friends

Note

both indicators below would need peer reviewing to confirm the implementations. Use with care.

A sample implementing a KalmanMovingAverage can be found below. This is

modeled after a post here: Quantopian Lecture Series: Kalman Filters

The implementation:

class KalmanMovingAverage(bt.indicators.MovingAverageBase):

packages = ('pykalman',)

frompackages = (('pykalman', [('KalmanFilter', 'KF')]),)

lines = ('kma',)

alias = ('KMA',)

params = (

('initial_state_covariance', 1.0),

('observation_covariance', 1.0),

('transition_covariance', 0.05),

)

plotlines = dict(cov=dict(_plotskip=True))

def __init__(self):

self.addminperiod(self.p.period) # when to deliver values

self._dlast = self.data(-1) # get previous day value

def nextstart(self):

self._k1 = self._dlast[0]

self._c1 = self.p.initial_state_covariance

self._kf = pykalman.KalmanFilter(

transition_matrices=[1],

observation_matrices=[1],

observation_covariance=self.p.observation_covariance,

transition_covariance=self.p.transition_covariance,

initial_state_mean=self._k1,

initial_state_covariance=self._c1,

)

self.next()

def next(self):

k1, self._c1 = self._kf.filter_update(self._k1, self._c1, self.data[0])

self.lines.kma[0] = self._k1 = k1

And a KalmanFilter following a post here: Kalman Filter-Based Pairs

Trading Strategy In QSTrader

class NumPy(object):

packages = (('numpy', 'np'),)

class KalmanFilterInd(bt.Indicator, NumPy):

_mindatas = 2 # needs at least 2 data feeds

packages = ('pandas',)

lines = ('et', 'sqrt_qt')

params = dict(

delta=1e-4,

vt=1e-3,

)

def __init__(self):

self.wt = self.p.delta / (1 - self.p.delta) * np.eye(2)

self.theta = np.zeros(2)

self.P = np.zeros((2, 2))

self.R = None

self.d1_prev = self.data1(-1) # data1 yesterday's price

def next(self):

F = np.asarray([self.data0[0], 1.0]).reshape((1, 2))

y = self.d1_prev[0]

if self.R is not None: # self.R starts as None, self.C set below

self.R = self.C + self.wt

else:

self.R = np.zeros((2, 2))

yhat = F.dot(self.theta)

et = y - yhat

# Q_t is the variance of the prediction of observations and hence

# \sqrt{Q_t} is the standard deviation of the predictions

Qt = F.dot(self.R).dot(F.T) + self.p.vt

sqrt_Qt = np.sqrt(Qt)

# The posterior value of the states \theta_t is distributed as a

# multivariate Gaussian with mean m_t and variance-covariance C_t

At = self.R.dot(F.T) / Qt

self.theta = self.theta + At.flatten() * et

self.C = self.R - At * F.dot(self.R)

# Fill the lines

self.lines.et[0] = et

self.lines.sqrt_qt[0] = sqrt_Qt

Which for the sake of it shows how packages also work with inheritance

(pandas is not really needed)

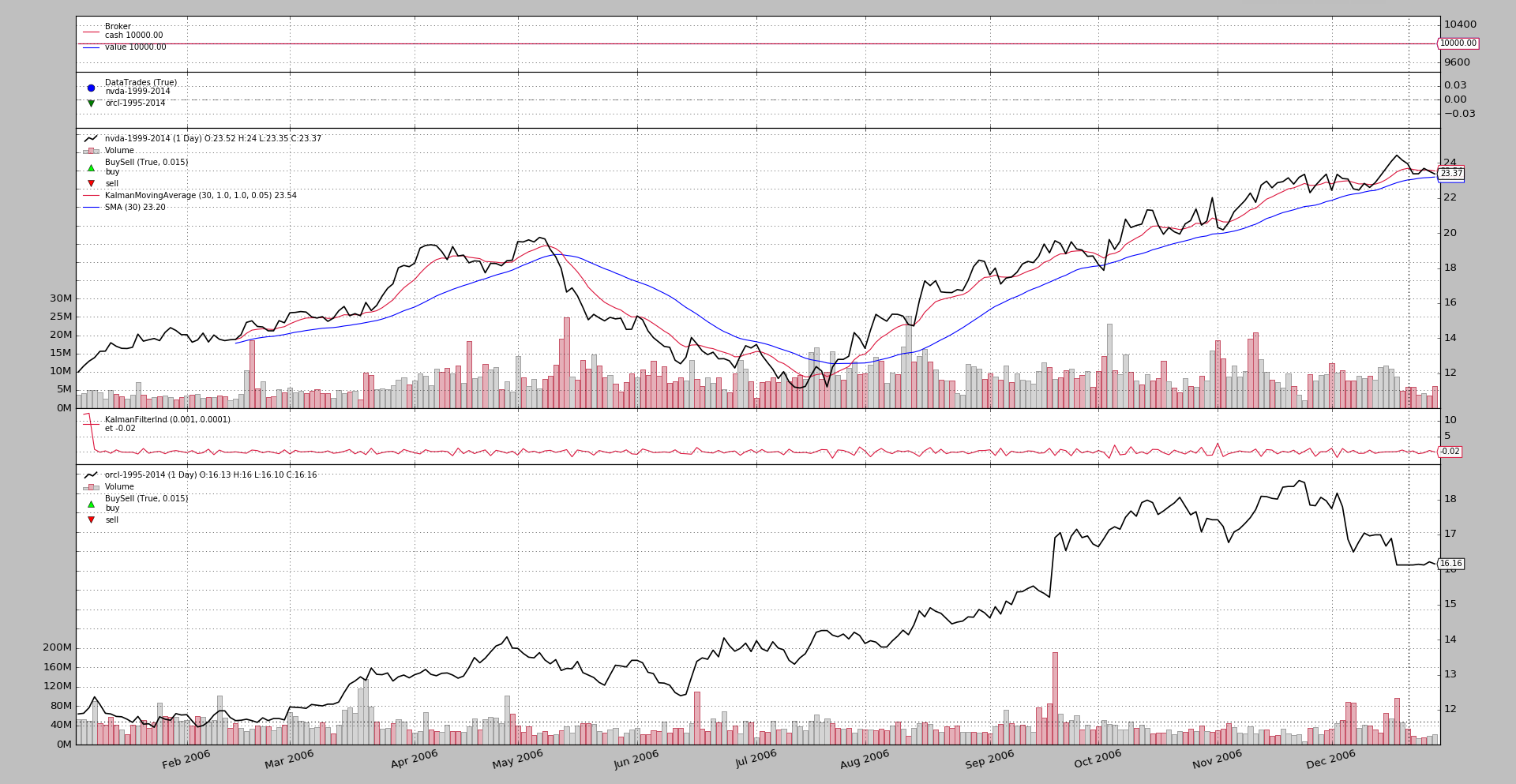

An execution of the sample:

$ ./kalman-things.py --plot

produces this chart

Sample Usage

$ ./kalman-things.py --help

usage: kalman-things.py [-h] [--data0 DATA0] [--data1 DATA1]

[--fromdate FROMDATE] [--todate TODATE]

[--cerebro kwargs] [--broker kwargs] [--sizer kwargs]

[--strat kwargs] [--plot [kwargs]]

Packages and Kalman

optional arguments:

-h, --help show this help message and exit

--data0 DATA0 Data to read in (default:

../../datas/nvda-1999-2014.txt)

--data1 DATA1 Data to read in (default:

../../datas/orcl-1995-2014.txt)

--fromdate FROMDATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default:

2006-01-01)

--todate TODATE Date[time] in YYYY-MM-DD[THH:MM:SS] format (default:

2007-01-01)

--cerebro kwargs kwargs in key=value format (default: runonce=False)

--broker kwargs kwargs in key=value format (default: )

--sizer kwargs kwargs in key=value format (default: )

--strat kwargs kwargs in key=value format (default: )

--plot [kwargs] kwargs in key=value format (default: )

Sample Code

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import datetime

import backtrader as bt

class KalmanMovingAverage(bt.indicators.MovingAverageBase):

packages = ('pykalman',)

frompackages = (('pykalman', [('KalmanFilter', 'KF')]),)

lines = ('kma',)

alias = ('KMA',)

params = (

('initial_state_covariance', 1.0),

('observation_covariance', 1.0),

('transition_covariance', 0.05),

)

def __init__(self):

self.addminperiod(self.p.period) # when to deliver values

self._dlast = self.data(-1) # get previous day value

def nextstart(self):

self._k1 = self._dlast[0]

self._c1 = self.p.initial_state_covariance

self._kf = pykalman.KalmanFilter(

transition_matrices=[1],

observation_matrices=[1],

observation_covariance=self.p.observation_covariance,

transition_covariance=self.p.transition_covariance,

initial_state_mean=self._k1,

initial_state_covariance=self._c1,

)

self.next()

def next(self):

k1, self._c1 = self._kf.filter_update(self._k1, self._c1, self.data[0])

self.lines.kma[0] = self._k1 = k1

class NumPy(object):

packages = (('numpy', 'np'),)

class KalmanFilterInd(bt.Indicator, NumPy):

_mindatas = 2 # needs at least 2 data feeds

packages = ('pandas',)

lines = ('et', 'sqrt_qt')

params = dict(

delta=1e-4,

vt=1e-3,

)

def __init__(self):

self.wt = self.p.delta / (1 - self.p.delta) * np.eye(2)

self.theta = np.zeros(2)

self.R = None

self.d1_prev = self.data1(-1) # data1 yesterday's price

def next(self):

F = np.asarray([self.data0[0], 1.0]).reshape((1, 2))

y = self.d1_prev[0]

if self.R is not None: # self.R starts as None, self.C set below

self.R = self.C + self.wt

else:

self.R = np.zeros((2, 2))

yhat = F.dot(self.theta)

et = y - yhat

# Q_t is the variance of the prediction of observations and hence

# \sqrt{Q_t} is the standard deviation of the predictions

Qt = F.dot(self.R).dot(F.T) + self.p.vt

sqrt_Qt = np.sqrt(Qt)

# The posterior value of the states \theta_t is distributed as a

# multivariate Gaussian with mean m_t and variance-covariance C_t

At = self.R.dot(F.T) / Qt

self.theta = self.theta + At.flatten() * et

self.C = self.R - At * F.dot(self.R)

# Fill the lines

self.lines.et[0] = et

self.lines.sqrt_qt[0] = sqrt_Qt

class KalmanSignals(bt.Indicator):

_mindatas = 2 # needs at least 2 data feeds

lines = ('long', 'short',)

def __init__(self):

kf = KalmanFilterInd()

et, sqrt_qt = kf.lines.et, kf.lines.sqrt_qt

self.lines.long = et < -1.0 * sqrt_qt

# longexit is et > -1.0 * sqrt_qt ... the opposite of long

self.lines.short = et > sqrt_qt

# shortexit is et < sqrt_qt ... the opposite of short

class St(bt.Strategy):

params = dict(

ksigs=False, # attempt trading

period=30,

)

def __init__(self):

if self.p.ksigs:

self.ksig = KalmanSignals()

KalmanFilter()

KalmanMovingAverage(period=self.p.period)

bt.ind.SMA(period=self.p.period)

if True:

kf = KalmanFilterInd()

kf.plotlines.sqrt_qt._plotskip = True

def next(self):

if not self.p.ksigs:

return

size = self.position.size

if not size:

if self.ksig.long:

self.buy()

elif self.ksig.short:

self.sell()

elif size > 0:

if not self.ksig.long:

self.close()

elif not self.ksig.short: # implicit size < 0

self.close()

def runstrat(args=None):

args = parse_args(args)

cerebro = bt.Cerebro()

# Data feed kwargs

kwargs = dict()

# Parse from/to-date

dtfmt, tmfmt = '%Y-%m-%d', 'T%H:%M:%S'

for a, d in ((getattr(args, x), x) for x in ['fromdate', 'todate']):

if a:

strpfmt = dtfmt + tmfmt * ('T' in a)

kwargs[d] = datetime.datetime.strptime(a, strpfmt)

# Data feed

data0 = bt.feeds.YahooFinanceCSVData(dataname=args.data0, **kwargs)

cerebro.adddata(data0)

data1 = bt.feeds.YahooFinanceCSVData(dataname=args.data1, **kwargs)

data1.plotmaster = data0

cerebro.adddata(data1)

# Broker

cerebro.broker = bt.brokers.BackBroker(**eval('dict(' + args.broker + ')'))

# Sizer

cerebro.addsizer(bt.sizers.FixedSize, **eval('dict(' + args.sizer + ')'))

# Strategy

cerebro.addstrategy(St, **eval('dict(' + args.strat + ')'))

# Execute

cerebro.run(**eval('dict(' + args.cerebro + ')'))

if args.plot: # Plot if requested to

cerebro.plot(**eval('dict(' + args.plot + ')'))

def parse_args(pargs=None):

parser = argparse.ArgumentParser(

formatter_class=argparse.ArgumentDefaultsHelpFormatter,

description=(

'Packages and Kalman'

)

)

parser.add_argument('--data0', default='../../datas/nvda-1999-2014.txt',

required=False, help='Data to read in')

parser.add_argument('--data1', default='../../datas/orcl-1995-2014.txt',

required=False, help='Data to read in')

# Defaults for dates

parser.add_argument('--fromdate', required=False, default='2006-01-01',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--todate', required=False, default='2007-01-01',

help='Date[time] in YYYY-MM-DD[THH:MM:SS] format')

parser.add_argument('--cerebro', required=False, default='runonce=False',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--broker', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--sizer', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--strat', required=False, default='',

metavar='kwargs', help='kwargs in key=value format')

parser.add_argument('--plot', required=False, default='',

nargs='?', const='{}',

metavar='kwargs', help='kwargs in key=value format')

return parser.parse_args(pargs)

if __name__ == '__main__':

runstrat()